Navigating Fixed Income Markets in 2025

Monthly Market Commentary

By Kensington Asset Management Team

At Kensington Asset Management, we’ve actively managed fixed income solutions for clients for over three decades. Throughout this journey, we’ve weathered all types of macroeconomic regimes from extreme market volatility events to periods of steady growth. These experiences have equipped us with a deep understanding of the opportunities and risks inherent in fixed income investing. We believe our time-tested, quantitative approach allows us to capture meaningful upside, while guarding against periods of decline and increased risk.

2024 presented a mixed bag for fixed income investors. While inflation began to cool, creating a path for the Federal Reserve to begin cutting rates, market participants grappled with lingering uncertainties surrounding the battle against inflation, the strength of the economy and labor markets. With rate cuts, changing correlations between asset classes, and a reshaping of the yield curve, understanding the current landscape is more critical than ever.

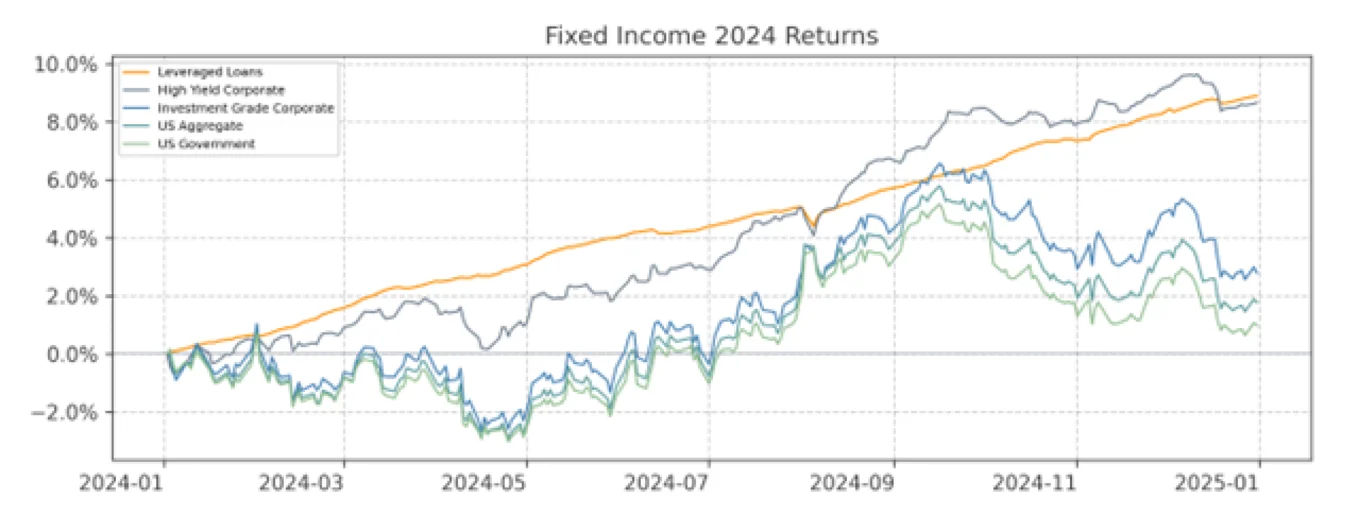

Lower Duration with Lower Credit Quality: A Winning Formula in 2024

As equity markets reached new all-time highs in 2024, areas of fixed income with lower relative credit quality, such as US Corporate High Yield Bonds, and Leveraged Loans, outshined, as these areas of the bond market traditionally exhibit a higher degree of correlation with the equity markets. As shown in the chart below, these asset classes exhibited higher returns with lower relative volatility. Our approach to fixed income in 2024was centered around this lower credit quality/lower duration approach. This allowed for meaningful yield to be harvested, while guarding against larger price erosion as rates climbed to close out the year. Conversely, areas of fixed income with greater sensitivity to interest rate changes underperformed throughout the year. This performance gap grew wider after yields began to rise again in the fourth quarter. While market participants were optimistic for bonds in 2024, with as many as six rate cuts priced in, hopes quickly faded as it became clear that “higher for longer” remained the prevailing theme during the first half of the year.

Current Conditions

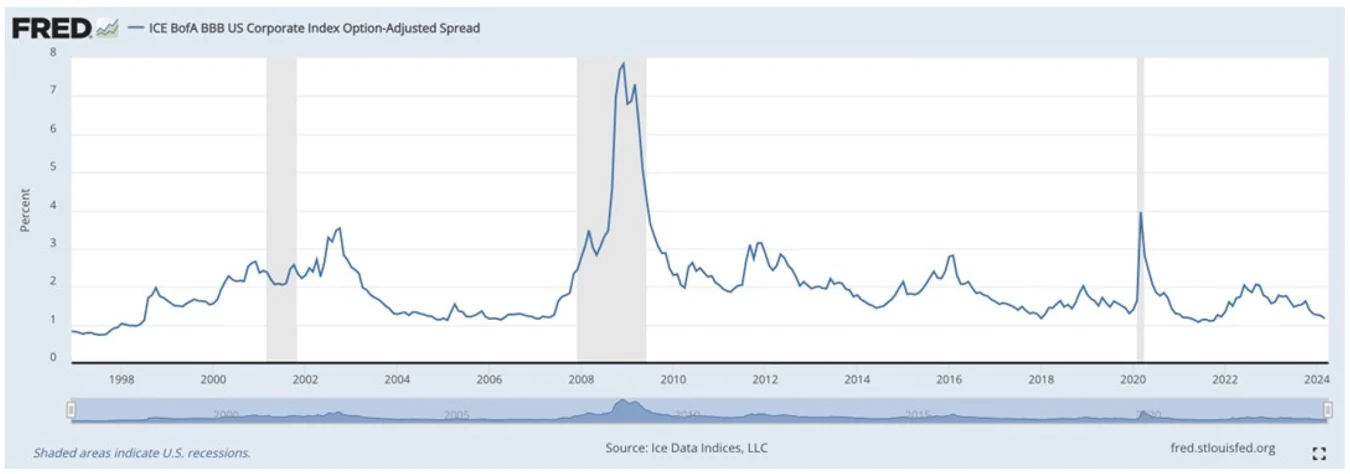

As we enter 2025, the fixed income landscape features tight credit spreads, a reshaping of the yield curve, and uncertainty surrounding the path of further rate cuts. While inflation has moderated, its trajectory from here remains uncertain, keeping the investment environment dynamic. Further, current spreads in the high yield market, a metric comparing the risk-free rate to high yield coupon rates, have reached the lowest recorded measurement since 2007, as shown below. While tight spreads indicate investor confidence in credit markets, these levels also signal reduced compensation for risk.

Also of particular note is the state of the yield curve. In a normalized yield curve, market participants demand a higher rate for longer dated Treasuries. However, from July 2022 to September 2024, the 2-Year Treasury rate exceeded the 10-Year Treasury. This yield curve “inversion,” lasting over two years, exceeded the previous record of 624 days, set in 1978. An inverted yield curve—historically, viewed as a reliable predictor of recessions—continues to weigh on investor sentiment.

Finally, as we wrap up 2024, future rate decisions by the Federal Reserve remain a central theme for investors. As of December 31, 2024, market participants are pricing in an 89% chance of no rate changes for the first Federal Reserve meeting of 2025 in January, and only a 54% chance of achieving a rate cut by the March meeting, according to CME Group’s Fed Watch tool. Continued strength in the US economy, paired with stalling progress on inflation reduction, could lead to a prolonged Fed “pause,” or perhaps even rate hikes.

Where We Could Be Going

Looking ahead, the historical aftermath of yield curve inversions can potentially provide valuable context. Typically, such inversions are followed by periods of economic slowdown or recession. Further, these periods of slowdown often begin after the “un-inversion” of the curve. As shown in the chart below, recessions, represented by gray shaded areas, typically follow after the curve normalizes. Such a slowdown could mean traditional areas of fixed income appreciate as rates fall.

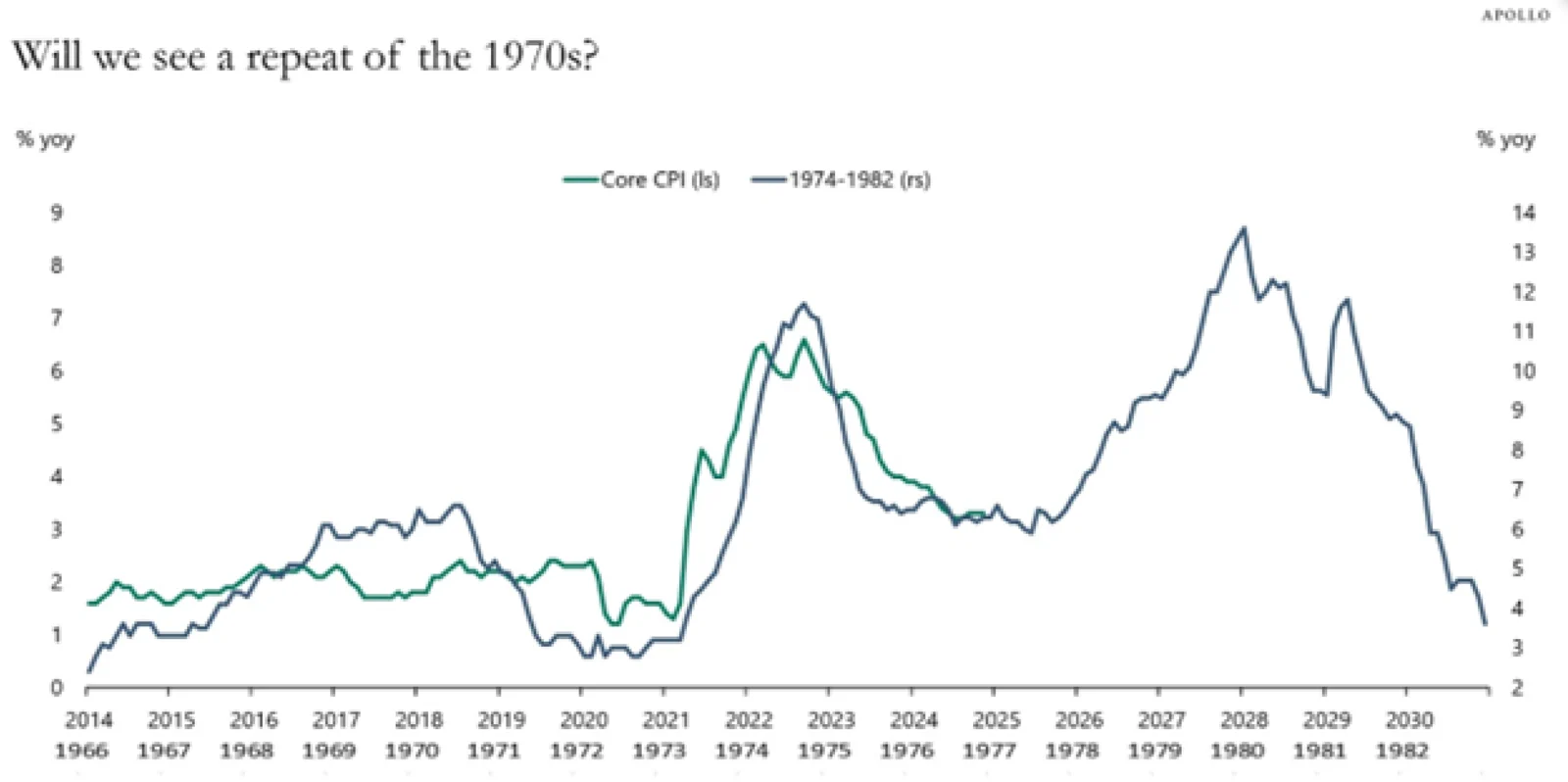

On the other hand, some economists believe inflation could be on the rise in the months and years ahead, harkening back to the inflation patterns of the 1970s. The following chart from Apollo illustrates the possible parallels between these eras:

While such analogs often fail to pan out, the threat of reinflation introduces significant implications for fixed income investors, including the need to prepare for heightened volatility and a rethinking of traditional strategies, as was the case in 2022.

We believe understanding these potential scenarios is key to navigating the road ahead. Whether we face reinflation, stagnation, or continued growth, we believe it is vital for investors to position themselves for resilience and adaptability.

Solutions for the Road Ahead

In an environment as complex as today’s, active management takes center stage. During dynamic market shifts, passive strategies often struggle to adapt to changing market conditions, making a compelling case for active solutions. We believe the following solutions should be considered when setting fixed income allocations for the year ahead:

Managed Income: Our Managed Income Strategy, which celebrates its 34th year in 2025, focuses on allocating to higher yielding segments of fixed income when conditions are favorable, while shifting to defensive sectors, such as cash and Treasuries, when market risk is elevated. In 2024, the Managed Income Strategy was fully invested for most of the year, leaning into the higher yielding/lower duration segments of fixed income described above. However, in a year such as 2022, when inflation and yields were rising, the Managed Income Strategy was in a “Risk-Off” stance for much of the year, as all segments of fixed income suffered meaningful drawdowns.

Active Advantage: Through a blending of model approaches and qualitative security selection, our Active Advantage Strategy adds equity exposure to our time-tested Managed Income process. This strategy should be considered for investors seeking a slightly riskier investment profile than Managed Income, but still value drawdown and downside participation. Active Advantage is engineered to provide access to both fixed income and equities in one actively managed solution. As is the case with Managed Income, Active Advantage can also move “Risk-Off” should conditions warrant.

Consider Kensington Asset Management as a Traditional Fixed Income Complement

The fixed income landscape in 2025 will likely continue to challenge investors, but with challenges come opportunities. At Kensington Asset Management, we stand ready to guide our investors through this ever-changing environment, leveraging decades of experience and a commitment to active, adaptive investing. As the markets evolve, we remain steadfast in our mission: delivering solutions that enable investors to achieve their financial goals while navigating uncertainty.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or are presentation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Managed Income Strategy

Risks specific to the Managed Income Strategy include Management Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Non-Diversification Risk, Turnover Risk, US Government Securities Risk, LIBOR Risk, Models and Data Risk.

Active Advantage Strategy

Risks specific to the Active Advantage Strategy include Management Risk, Equity Securities Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Limited History of Operations Risk, Non-Diversification Risk, Small and Mid-Capitalization Companies Risk, Turnover Risk, US Government Securities Risk, LIBOR Risk, Models and Data Risk.

Definitions

Federal Reserve Economic Data (“FRED”): Federal Reserve Economic Data (FRED) is a comprehensive database maintained by the Federal Reserve Bank of St. Louis, containing over 816,000 economic time series from various national and international sources. It provides users with tools to download, graph, and track economic data, aiding in economic research and analysis.

Normalized Yield Curve: A graphical representation where short-term debt instruments have lower yields than long-term debt instruments of the same credit quality. This upward-sloping curve suggests that investors expect higher returns for taking on the increased risk associated with longer-term investments.

Reinflation: The process of increasing the general price level of goods and services in an economy after a period of deflation or economic stagnation. It involves implementing monetary or fiscal policies to stimulate demand and drive prices back up.

Stagnation: A state where there is little or no growth, development, or movement in an economy, market, or other system. It can result in prolonged periods of economic inactivity, leading to issues such as high unemployment and low productivity.

Yield Curve Inversion (Inverted Yield Curve): When short-term interest rates become higher than long-term interest rates. This is unusual because typically, long-term interest rates are higher due to the increased risk over time. An inverted yield curve often signals investor concerns about the economy and is considered a possible indicator of an upcoming recession.

Yield Curve Uninversion (Uninverted Yield Curve): When an inverted yield curve returns to its normal upward slope, indicating potentially an improved economic outlook and investor confidence.

Tracking #KAM20250103A1

Related Perspectives

View All-

KENSINGTON SPOTLIGHT SERIES: THE DEFENDER STRATEGY

At Kensington Asset Management, we’ve actively managed fixed income solutions for clients for over three decades. Throughout this journey, we’ve weathered all types of macroeconomic regimes from extreme market volatility events to periods of steady growth.

-

White paper: Trend Following and Tail Risk

An introductory understanding of how trend following can manage tail risk.