Decoding the Fed’s Next Moves

Market Insights

Brian Weisenberger, CFA, Senior Market Strategist

Market Insights is a piece in which Kensington’s Portfolio Management team will share interesting and thought-provoking charts that we believe provide insight into markets and the current investment landscape.

CPI Report Offers Clues on the Fed’s Next Move – But What Comes After?

This week’s CPI report provided the final inflation reading ahead of the September Federal Open Market Committee (FOMC) meeting, where Chairman Powell and the Committee are expected to lower interest rates for the first time since the rate-hiking cycle began in March 2022. While inflation data plays a critical role in the Fed’s decision-making, other key economic signals, such as labor market dynamics and bond performance, are starting to hint at potential long-term shifts in the broader market. Let’s explore how these factors may shape investment strategies moving forward.

Cooling Inflation, But Core Prices Hold Firm

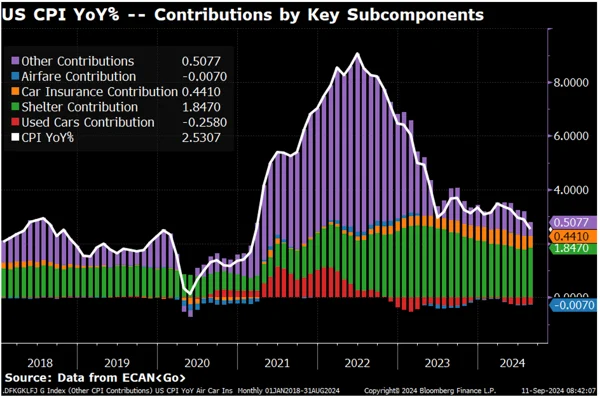

The headline CPI came in at 2.5% year-over-year (y/y), its lowest reading since February 2021, meeting market expectations (chart below). However, a slightly stronger-than-expected core CPI reading (0.3% month-over-month (m/m) vs. 0.2% m/m) triggered an initial market selloff, likely diminishing the probability of a more aggressive rate cut by the Fed.

This stronger core reading was driven by Shelter CPI, which increased by 5.2%, marking the 29th consecutive month with housing inflation above 5%. This streak of elevated shelter costs is the longest since the early 1980s. But it’s important to note that shelter inflation is a lagging indicator and may not reflect real-time conditions.

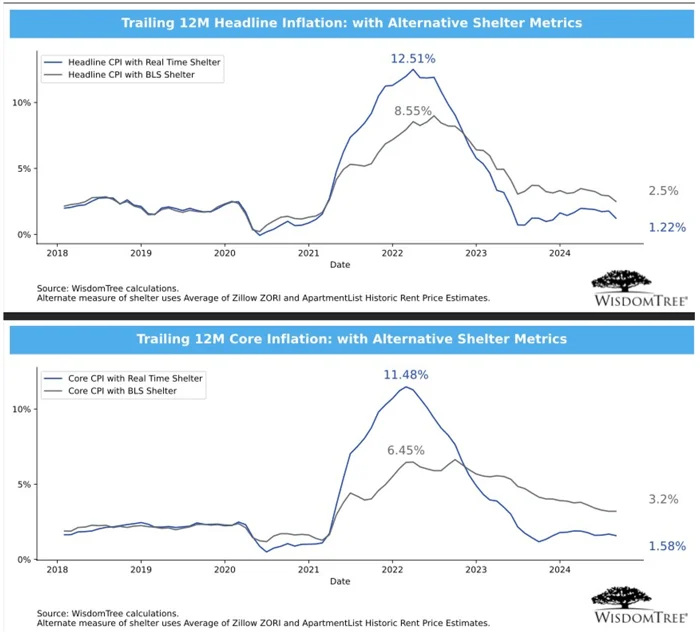

When we look at real-time shelter data, using metrics such as Zillow’s ZORI and ApartmentList’s Historical Rent Price Estimates, the picture changes. These measures suggest that both headline and core CPI would fall below the Fed’s 2% target—at 1.22% and 1.58%, respectively (chart below). This could signal that inflation concerns may soon give way to a different problem: inflation running too low.

The Shift from Inflation Concerns to Labor Market Weakness

As Bloomberg recently pointed out, “Persistently low inflation is as detrimental to the economy as elevated prices because it forces policymakers to keep borrowing costs too low for too long, reducing the Fed’s ability to combat economic downturns.”

Indeed, Fed Chair Jerome Powell acknowledged this challenge during the August Jackson Hole Symposium, noting that, “The cooling in labor market conditions is unmistakable.” (8/24/24) Persistent disinflation, coupled with a softening labor market, could limit the Federal Reserve’s ability to respond if recessionary pressures build. Although this scenario is still hypothetical and may not materialize for several months, it raises important questions about the future trajectory of US markets.

A Shift in Market Performance: Bonds Take the Lead

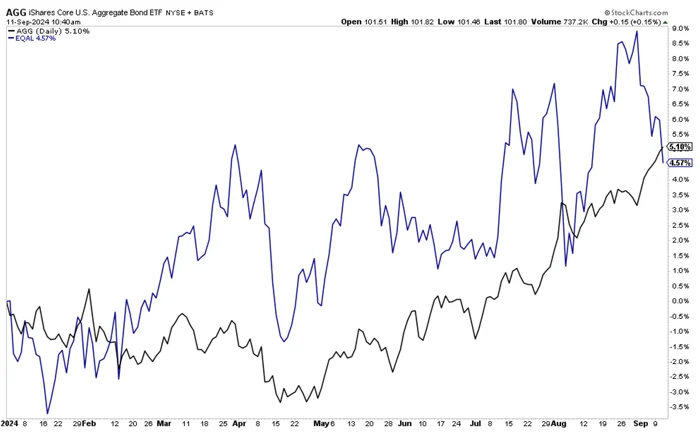

While inflation and labor concerns dominate the headlines, we’re already seeing notable shifts in market performance (chart below). For the first time in years, the Aggregate Bond Index has outperformed the “average US equity” year-to-date, signaling a potential change in market regime.

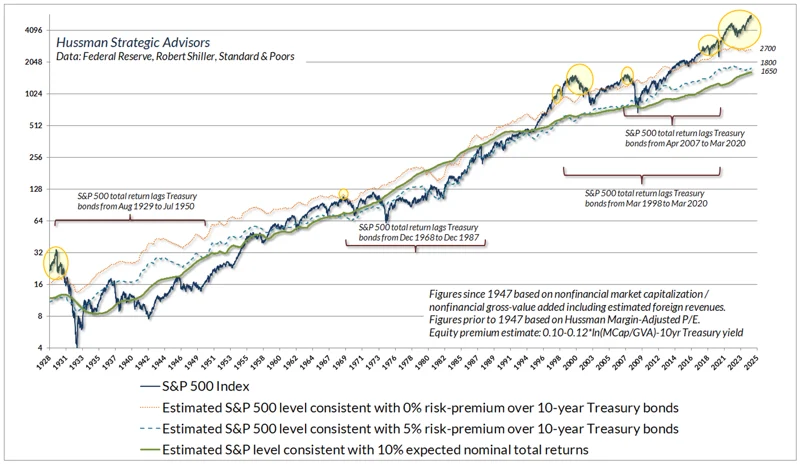

Although this outperformance may seem like an anomaly, historical precedent suggests bonds can outperform equities over extended periods. John Hussman highlights several periods—1927-1947, 1968-1985, and 2000-2013—when T-bills outperformed the S&P 500. The common factor during these periods? Extreme equity valuations at the outset, something that is consistent with today’s market based on his analysis.

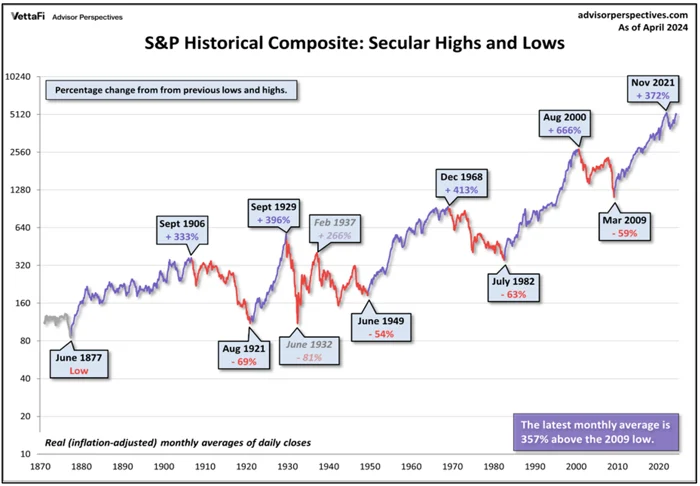

Secular Bear Markets and the Long-Term Outlook

Another shared characteristic of these periods is that they align with historical secular bear markets (chart below). These long-term periods of price declines, punctuated by occasional rallies, can last upwards of 20 years. While many investors today have never experienced a secular bear market—the last one concluded in March 2009—history shows that these periods can be prolonged and challenging.

We’re not suggesting the start of a new secular bear market just yet. However, as the economic narrative shifts from inflationary concerns to labor market issues, it’s worth broadening our perspective. Long-term market shifts may already be underway, and strategies that thrived during periods of inflation might struggle as we move into a new regime.

Navigating Uncertainty

Given the mounting uncertainty surrounding inflation, the labor market, and potential market shifts, a tactical approach to investing may be essential in the months—and possibly years—ahead. By being flexible and adaptive, investors can better navigate an evolving landscape where traditional strategies may no longer perform as expected.

As we head into the next phase of the market cycle, understanding these dynamics and remaining agile will be key to weathering potential changes in the economic environment.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Related Perspectives

View All-

KHPI’s Fiscal Year 2025 Review and the Power of Net-of-Tax Performance

KHPI’s Fiscal Year 2025 Review and the Power of Net-of-Tax Performance Monthly Market Commentary By Kensington Asset Management Team The following is for informational purposes only and not construed as tax advice. Please consult with a tax professional for your specific situation. For the modern fiduciary, performance is a multi-dimensional metric. While investment returns capture […]

-

KENSINGTON SPOTLIGHT SERIES: THE DEFENDER STRATEGY

At Kensington Asset Management, we’ve actively managed fixed income solutions for clients for over three decades. Throughout this journey, we’ve weathered all types of macroeconomic regimes from extreme market volatility events to periods of steady growth.