Is Inflation Here to Stay?

Monthly Market Commentary

By Bruce DeLaurentis

In last month’s commentary, we highlighted the historically elevated level of debit balances in margin accounts. Although this metric is not incorporated into the models we employ since it doesn’t meet our criteria for being a precise timing tool, it does suggest an extreme in bullish sentiment that should give investors a reason to temper upside expectations.

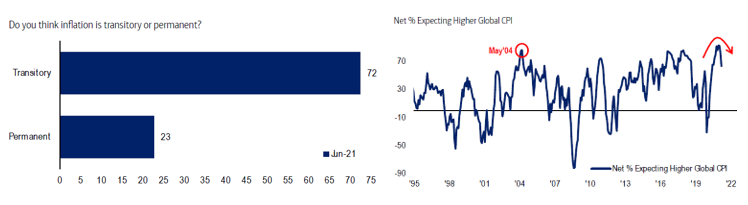

Another theme that warrants discussion is the emergence of inflationary pressures and its implications for monetary policy. The results of a recent survey of global fund managers by Bank of America is depicted below.

As indicated, 72% of professional money managers surveyed believe inflation is transitory while only 23% believe inflation is permanent. The expectation that inflation may be transitory is supported by the recent reversal in longer-term interest rates, having topped in March and fallen off since. The biggest threat to the sustainability of the bull trend would be a reversal in monetary policy to a more hawkish stance by the Fed to contain inflationary pressures. Rising rates would be particularly dangerous considering the current high level of margin debt.

Comments emanating from the recent Federal Reserve Open Market Committee suggest that there could be two rate hikes in 2023 if inflationary pressures do not abate. For now, the Fed does not see a need for immediate action and is holding policy steady. The markets have responded favorably with the NASDAQ making new highs and the S&P 500 Index threatening to follow suite.

It is important to bear in mind that rising inflationary pressures are indicative of improving economic growth. If the Fed does not take action to tighten monetary policy, the risk assets such as equities and lower quality debt that comprise Kensington’s portfolios should benefit.

The future is extremely difficult to predict, but managing risk is a less daunting endeavor. Kensington’s model driven process has consistently sought to protect its clients from painful losses during numerous market downturns, while seeking to capturing upside when market trends are favorable.

Best regards,

Bruce P. DeLaurentis

Kensington Asset Management, LLC.

Related Perspectives

View All-

Strategy Review – January 2026

Risk assets delivered mixed but generally positive results in November as investors weighed softer labor data, the ongoing government shutdown, and the prospect of another Federal Reserve rate cut in December.

-

Monthly Market Commentary – January 2026

Risk assets delivered mixed but generally positive results in November as investors weighed softer labor data, the ongoing government shutdown, and the prospect of another Federal Reserve rate cut in December.