Is This Time Different?

Monthly Market Commentary

By Kensington Asset Management Team

Geopolitics

This time is different. Sophisticated investors are reflexively skeptical whenever they hear this bromide, particularly so when used to make the case for investing in China. Over the past few years, bullish investors, lured by the combination of low equity valuations and the promise of meaningful government stimulus, have enthusiastically called turns in Chinese equities only to see multiple price rallies evaporate in the face of continued sluggish growth and increasing Party control over the economy. An increasingly hostile West and an intractable real estate crisis disillusioned many of those investors.

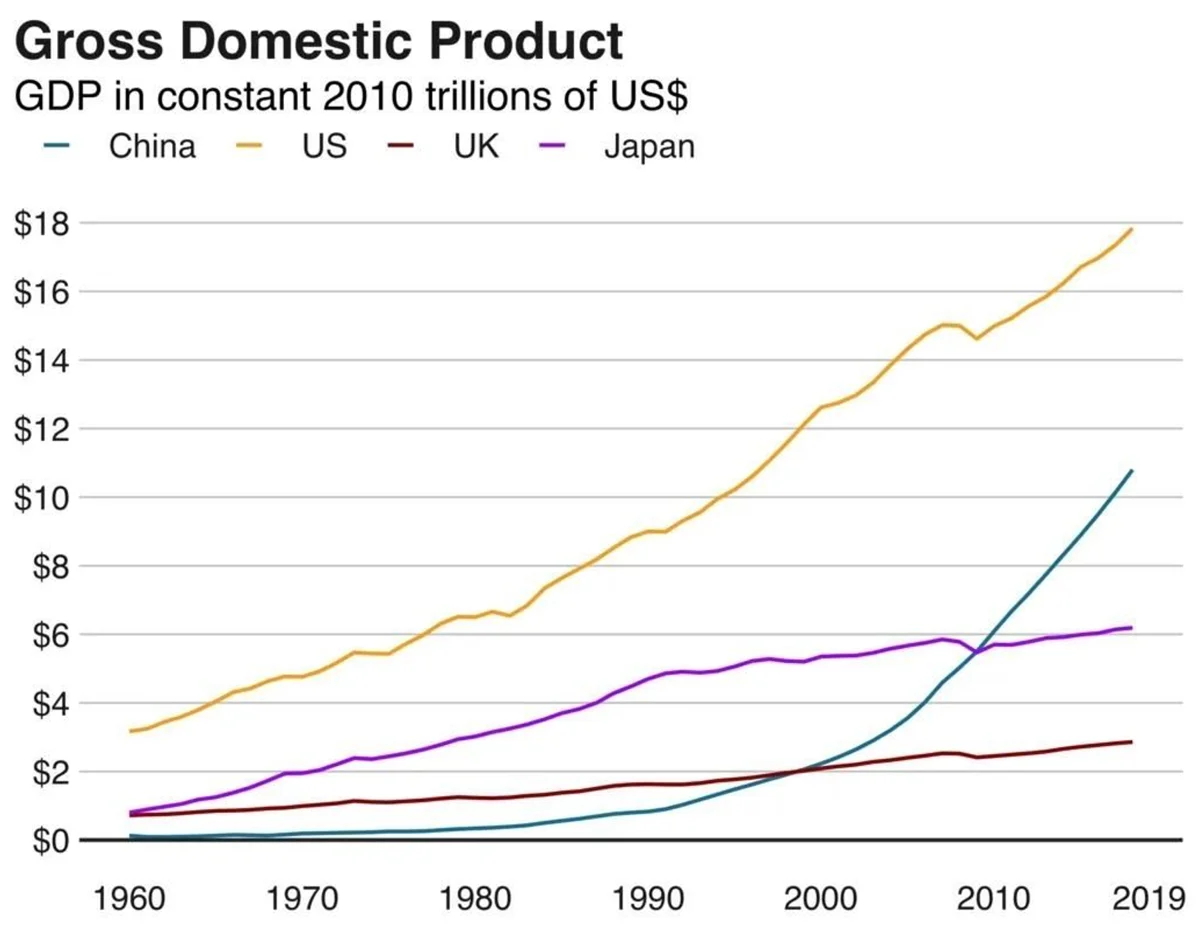

Perhaps a more nuanced appraisal and understanding of the country’s past economic policy is needed, however, to determine if China is indeed at a major turning point. As seen in the chart below, beginning with the country’s pivotal market reforms in 1978, followed by inclusion in the World Trade Organization (WTO) in 2003, the country experienced rapid and accelerating GDP growth.

It accomplished this feat mainly by means of their reliance on a mercantilist economic system, one that relies on the export of goods and services to drive national prosperity. Such a system places far greater emphasis on production and investment to drive growth and less emphasis on consumption.

A mercantilist approach is not atypical when nations are in the beginning stages of development and GDP is small relative to competing trading partners. The smaller, industrializing nation is able to produce goods at lower cost given lower wages and other comparative advantages and the larger trading partners reap the benefits of being able to purchase goods more cheaply. Both are better off as a whole.

Conflict arises, however, when the smaller nation grows significantly larger and their exports to trading partners effectively represent a greater share of the latter’s total domestic output. While both nations benefit, the larger trading partner’s domestic producers find themselves increasingly disadvantaged as production is moved overseas.

Such a shift in production can only go on for so long. Once the smaller mercantilist becomes a meaningful competitive threat, the larger trading partners will understandably react and start putting in place increasingly restrictive ways to reduce these imports, especially if the mercantilist does not open its own economy to trading partners’ goods.

Is there a long-term solution to resolving this situation? One school of thought asserts Beijing must set out to restructure its economic system in such a way that places greater emphasis on domestic consumption. As can be seen in the graph below, China saves far more than its major trading partners, and at least some portion of these excess savings might be – and should be – channeled into increased consumption by its own citizens. This would allow the country to continue growing while easing the stress it is causing by relying on foreign consumption to drive that growth.

The economic stimulus steps, the Chinese government recently announced, area slight step in that direction. But to be clear, closing the gap between domestic production and consumption will be a monumental and difficult task. Such a restructuring will take years and is only possible if President Xi and the Communist Party have the foresight and fortitude to embark on this essential transformation.

stock market

The S&P 500 Index was up 2.02% in the month of September, while the Nasdaq 100 gained 2.48% and the Russell 2000 was up fractionally, 0.56%. For the quarter, all three indices finished in the black, led by the Small Cap Russell advancing 8.90%, followed by the S&P 500, up 5.53% and the Nasdaq 100, gaining 1.92%. Year-to-date, the S&P 500 and Nasdaq 100 gained 20.81% and 19.22% respectively, while the Russell was up a more modest 10.01%.

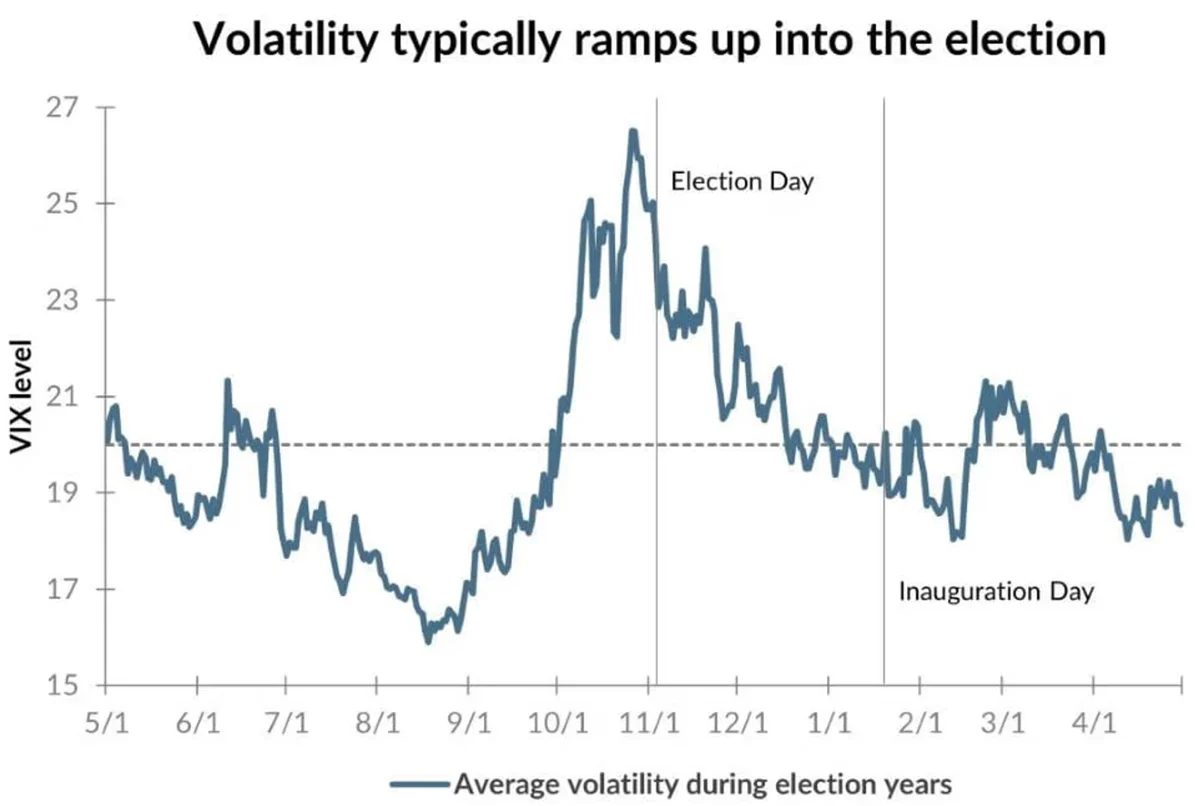

The strong performance put in by the indices in 2024 continues to closely track the historical playbook for election years. Though valuations remain challenging, easing inflation, surprisingly healthy economic growth, a Federal Reserve that appears to have stuck the (soft or no) landing, and the future promise of artificial intelligence continue to boost investor enthusiasm for equities.

Nonetheless, we should expect increased volatility in the months of October and November, as has been the case historically in the months preceding the election.

Data reflects the average CBOE Volatility Index (VIX) in full elections years since 1992.

As always, a bull market’s foundation rests on earnings and those continue to trend strongly upwards.

fixed income

The fixed income markets performed extraordinarily well in the third quarter on the back of surprisingly positive inflation figures. The US Treasury 30-year bond gained 8.07% in the quarter, the 10-year was up 5.75% and the Bloomberg US Corporate Investment Grade Index advanced 5.84%. Lower rated bonds as reflected by the Bloomberg US Corporate High Yield Index returned 5.28%.

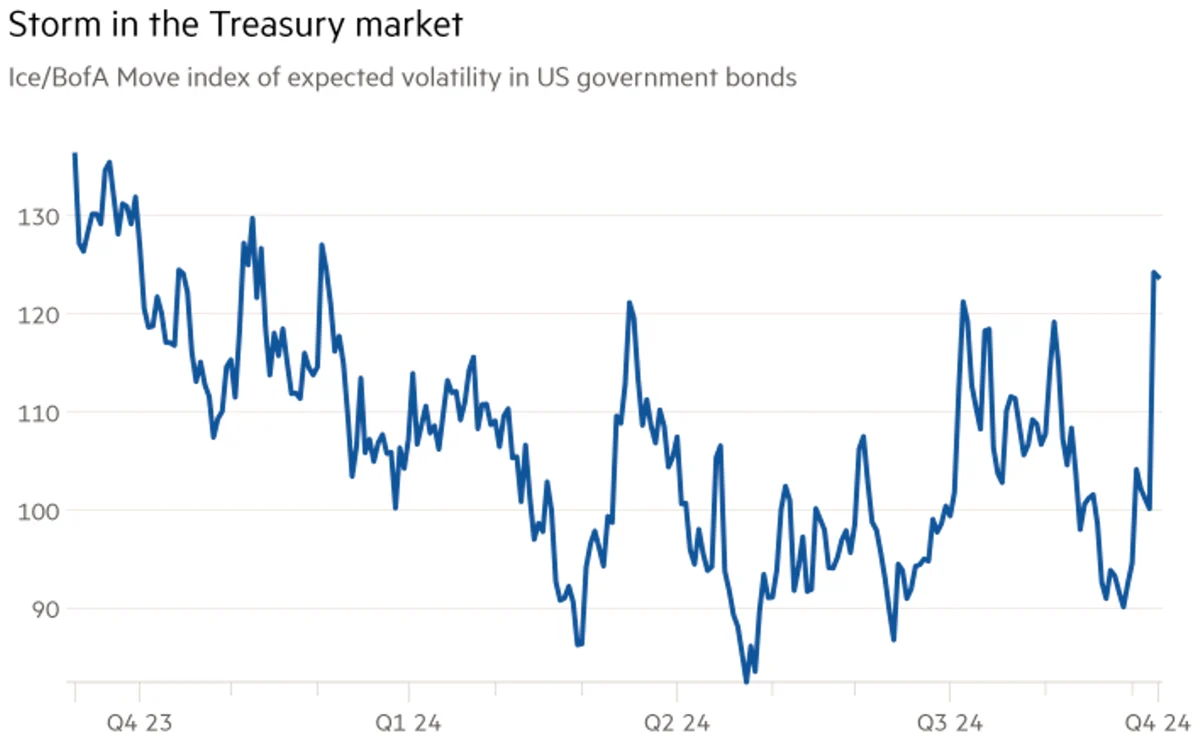

While the rate-driven performance was stellar, it reversed abruptly in the new month when the non-farm payroll numbers were released, showing a stunning increase of 254,000 jobs. The report also showed the economy added 72,000 more jobs in July and August than previously estimated. On top of the continuing decline in the 4-week average jobless claims, a stabilizing Job Openings and Labor Turnover (“JOLTS”) Survey and solid wage growth, consensus expectations for a rapid slowdown in growth are once again in question.

Not surprisingly, the entire yield curve shifted higher following the news, with the greatest impact seen at the long end. Price volatility ratcheted up as well with the ICE BofA Move index, a gauge of bond investors’ expectations of future volatility in the Treasury market, rising to its highest level since January at the time of this publication.

Federal Reserve and Monetary Policy

Chairman Powell has taken pains to tell the Street the Federal Reserve will be patient in implementing its pivot to easing, letting the data dictate speed and size. In the September FOMC meeting, members were supportive of the policy change, confident the downward trajectory in prices would continue, pointing to a whole host of factors: a further modest slowing in real GDP growth, well-anchored inflation expectations, waning pricing power, increases in productivity and a softening in world commodity prices. A number of participants noted that nominal wage growth was continuing to slow, with a few citing signs that it was set to decline further. The economy remains quite resilient however, and it is unclear if the Fed’s (and the Market’s) confidence in an economic slowdown scenario is well founded.

Managed Income Strategy – Manager Commentary

September brought market participants the much-anticipated initial rate cut from the Federal Reserve. On September 18, Fed Chair Jerome Powell announced a reduction in the federal funds rate of a half percentage point, or 50-basis points. In the months leading up to this announcement, expectations from market participants pointed toward a 25-basis point cut; however, weakening manufacturing and labor data played a large role in the decision to move forward with a larger cut to begin the cycle. Powell also set expectations for more rate cuts totaling another 50 bps points through the end of 2024.

During the month, all bond sectors benefited from the anticipated rate cut, with more duration-sensitive asset classes leading the way. US High Yield turned in its fifth consecutive month of positive returns. However, longer duration bonds pared back some of their gains for the month after the rate cut was announced, as some market participants “sold the news.”

The Managed Income Model remains Risk-On, and the current portfolio remains high yield centric, with satellite positions in floating rate and senior loan investments. We anticipate high yield to remain strong at this point, and do not anticipate any changes to the Portfolio composition in the short term.

Dynamic Growth Strategy – Manager Commentary

US stocks got off to a rocky start in September, with a second consecutive month of disappointing data from the labor markets. The S&P 500 index plunged over 4% in the first four trading sessions of the month. This was the worst performance for the S&P 500 in the first week of September since 1953. Following this sharp pullback, equities rallied for the remainder of the month, finishing positive for September. This was the first time the S&P 500 had produced a positive September since 2019.

For the week of September 2, the Dynamic Growth Model gave a Risk-On signal due to the continued uptrend established after the August 5 selloff. Because of seasonal factors, as well as elevated risks from manufacturing and labor data, the Portfolio Management Team positioned the Portfolio more defensively than usual, allocating tilt positions to low beta equities and large cap value, while underweighting the technology sector. With this more conservative positioning, the Strategy slightly outperformed the S&P 500 for the week and had better results than the usual growth-heavy allocation. However, due to this accelerated selloff, the Model moved the Strategy back to a Risk-Off position for the week of September 9, missing the S&P 500’s best week of the year. As volatility cooled once again, the Model moved the Strategy back into a Risk-On position for the week of September 30. The Portfolio currently consists of a mix of growth and core stocks.

For the second straight month, the Dynamic Growth Strategy suffered a classical “whipsaw” trade: bearing the brunt of the selloff while moving to the sideline before a sharp rebound. As we noted last month, such sequences are not unusual for a trend-following strategy. Above all else, our mantra is to protect against periods of outsized probability for loss. While such reversals do happen, we believe adherence to our long-term process is paramount to achieving Dynamic Growth’s investment objectives.

We believe risks still remain elevated for equity markets as we move deeper into the fourth quarter, as market participants continue to digest macroeconomic data. If future data points toward a continued slowing of the economy, or if inflation fails to continue falling, equities could be under pressure in the months ahead.

Active Advantage Strategy – Manager commentary

The Active Advantage Model remains positioned in a fully Risk-On state, with a balanced posture across fixed income and equities. The Portfolio began the month of September more conservatively positioned, with the majority of the fixed income portion of the Portfolio in higher credit quality holdings. This proved beneficial as markets sold off after Labor Day to begin the month.

As the month progressed, the Portfolio Management Team added some growth equity exposure, as well as additional high yield exposure. The Portfolio is well-diversified between equities and fixed income.

As noted above, we believe risks remain elevated for markets in general, as bond yields have risen after the rate cut announcement. Further pressure on fixed income could occur if inflation data begins to increase once again in Q4 2024. On the equity side, we remain positioned primarily in core equities to guard against volatility as the major indices reach all-time highs once again.

Defender Strategy – Manager commentary

September proved to be a challenging month across global equity markets, with heightened volatility driven by ongoing geopolitical tensions, central bank policy uncertainties, and slowing global growth. The US equity markets experienced a positive month of gains after early volatility despite concerns about inflationary pressures and interest rate positioning. Meanwhile, international markets faced headwinds from weaker-than-expected economic data from China and the Eurozone.

Amid this challenging backdrop, the Kensington Defender Strategy demonstrated its resilience, delivering a positive return for the month at the top of its category. The Fund’s slightly defensive posture and strategic allocation to lower-volatility sectors helped mitigate downside risks, exemplifying its role as a capital preservation vehicle during periods of market volatility as well as attempting to capture upside. Some of the strongest attributors to performance in the month were the US equity markets and gold.

Looking ahead, we remain cautiously optimistic. While economic uncertainty and market volatility are likely to persist, the Kensington Defender Strategy remains committed to its primary objective of preserving capital while providing moderate growth over the long term. We will continue to position the Strategy to navigate the current market environment, while seeking to deliver value to our investors through careful sector selection and risk management.

Hedged Premium Income Strategy – Manager Commentary

On September 5, 2024, Kensington rung the closing bell at the Cboe Global Markets trade floor to celebrate the launch of its first ETF based on the Hedged Premium Income Strategy. See Press Release here. It was a moment that captured the energy and dedication of everyone involved, marking a new chapter in Kensington’s growth and a shared achievement that everyone here was thrilled to be a part of.

With that said, the month of September kicked off with a bout of volatility, which is expected for the historically volatile month, falling over 4% in the first 4 trading days. For the Hedged Premium Income Strategy, the market was quickly approaching the hedging positions that are designed to provide a quarterly downside buffer against declines of 5-20%. This pullback turned out to be mild and short-lived, as the S&P 500 Index sharply rebounded to eventually make new all-time highs.

With this move higher, the Index moved into income generating positions (monthly call spreads), and ended up expiring near the top end of the spread range, which is the least desirable outcome for the Strategy as the returns for the period are limited to the net income that was generated. Once the market moves above the spread range, the Strategy benefits from unlimited appreciation potential since the strategy utilizes a “soft cap” (call spreads) as opposed to a “hard cap” (covered calls).

On September 20th, both the income-generating call spreads and downside buffers were reset to the new higher levels, resulting in both the floor and the cap to move higher. Due to the historically low volatility levels, the net option premium collected was near the high end of the range of our expectations. With the potential for more seasonal volatility on the horizon, the Strategy is well positioned to benefit from a flat, sharply lower or sharply higher markets.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular strategy such as the types of securities being substantially different.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Managed Income Strategy

Risks specific to the Managed Income Strategy include Management Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Non-Diversification Risk, Turnover Risk, U.S. Government Securities Risk, LIBOR Risk, Models and Data Risk.

Dynamic Growth Strategy

Risks specific to the Dynamic Growth Strategy include Management Risk, Equity Securities Risk, Market Risk, Underlying Funds Risk, Non- Diversification Risk, Small and Mid-Capitalization Companies Risk, Turnover Risk, U.S. Government Securities Risk, Models and Data Risk.

Active Advantage Strategy

Risks specific to the Active Advantage Strategy include Management Risk, Equity Securities Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Limited History of Operations Risk, Non-Diversification Risk, Small and Mid-Capitalization Companies Risk, Turnover Risk, U.S. Government Securities Risk, LIBOR Risk, Models and Data Risk.

Defender Strategy

Risks specific to the Defender Strategy are detailed in the prospectus and include general market risk, credit risk, interest rate risk, management risk, equity securities risk, fixed-income securities risk, high-yield bond risk, foreign investment risk, emerging markets risk, real estate and REITs risk, commodities risk, currency risk, subsidiary risk, market risk, underlying funds risk, derivatives risk, limited history of operations risk, turnover risk, models and data risk, momentum risk or risk of the portfolio not performing as expected.

Hedged Premium Income Strategy

The Strategy invests in options that derive their performance from the performance of the S&P 500 Index. Selling (writing) and buying options are speculative activities and entail greater than ordinary investment risks. The Strategy’s use of put options can lead to losses because of adverse movements in the price or value of the underlying asset, which may be magnified by certain features of the options. When selling a put option, the Strategy will receive a premium; however, this premium may not be enough to offset a loss incurred by the Strategy if the price of the underlying asset is below the strike price by an amount equal to or greater than the premium. Purchased put options may expire worthless and the Strategy would lose the premium it paid for the option. The Strategy may lose significantly more than the premiums it receives in highly volatile market conditions.

The Strategy will invest in short term put options which are financial derivatives that give buyers the right, but not the obligation, to sell (put) an underlying asset at an agreed-upon price and date. The Strategy’s use of options may reduce the Strategy’s ability to profit from increases in the value of the underlying asset. The Strategy could experience a loss or increased volatility if its derivatives do not perform as anticipated or are not correlated with the performance of their underlying asset or if the Strategy is unable to purchase or liquidate a position.

Definitions:

Bloomberg US Corporate Investment Grade Bond Index: An unmanaged index comprised of US investment grade fixed rate, taxable corporate bond market.

Bloomberg US Corporate High Yield Index: An unmanaged market value-weighted index that covers the universe of fixed-rate, non-investment grade debt in the US. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

Call Spread: An options trading strategy where the Strategy buys and sells call options on the same asset with different strike prices or expiration dates. The strategy helps manage risk and profit from small price changes.

Covered Call: An options strategy where a long asset position is held while a call option is sold. This generates income from the premiums received for selling the call option, but limits potential upside gains if the asset price rises above the strike price.

ICE BofA Move index: Measures US interest rate volatility based on options on Treasury securities. It reflects market expectations of future bond market volatility

Job Openings and Labor Turnover Survey (JOLTS): A program that provides information on labor demand and turnover.

NASDAQ 100 Index: A market index that comprises of the 100 largest, most actively traded companies listed on the Nasdaq stock exchange.

S&P 500: A capitalization weighted index of 500 stocks representing all major domestic industry groups. The S&P 500 TR Index assumes the reinvestment of dividends and capital gains.

Russell 2000 Index: A market index that consists of 2,000 small-cap US companies that are part of the larger Russell 3000 Index.

Related Perspectives

View All-

Strategy Review – May 2026

March was shaped by a sharp escalation in US-Iran tensions, a surge in energy prices, and renewed concern that inflation could stay stickier than expected. The Federal Reserve again held rates steady, while higher oil prices and rising yields pressured traditional risk assets.

-

Monthly Market Commentary – May 2026

US equities moved lower in March as the conflict involving Iran, the US, and Israel pushed energy prices sharply higher and added another layer of uncertainty to an already fragile market backdrop. After