Kensington Monthly Commentary – August 2025

Monthly Market Commentary

By Kensington Asset Management Team

EQUITY MARKETS

Equities extended their gains in August, supported by both broadening participation and improving fundamentals. The S&P 500 advanced 1.91%, the Nasdaq 100 gained 0.85%, and the small-cap Russell 2000 surged an impressive 7.00%. The rally’s breadth is particularly encouraging, as earnings momentum is no longer confined to mega-cap names. According to Leuthold’s latest Green Book, “Year-Over-Year earnings growth appears to be expanding beyond the mega-cap space for the first time in several years. Forward-looking measures also seem much more upbeat. The S&P 400’s (Mid Cap) next twelve months (NTM) EPS estimate finally eclipsed its old high (May 2022), and expectations for S&P 600 (Small Cap) NTM EPS have risen 6% in just three months.”

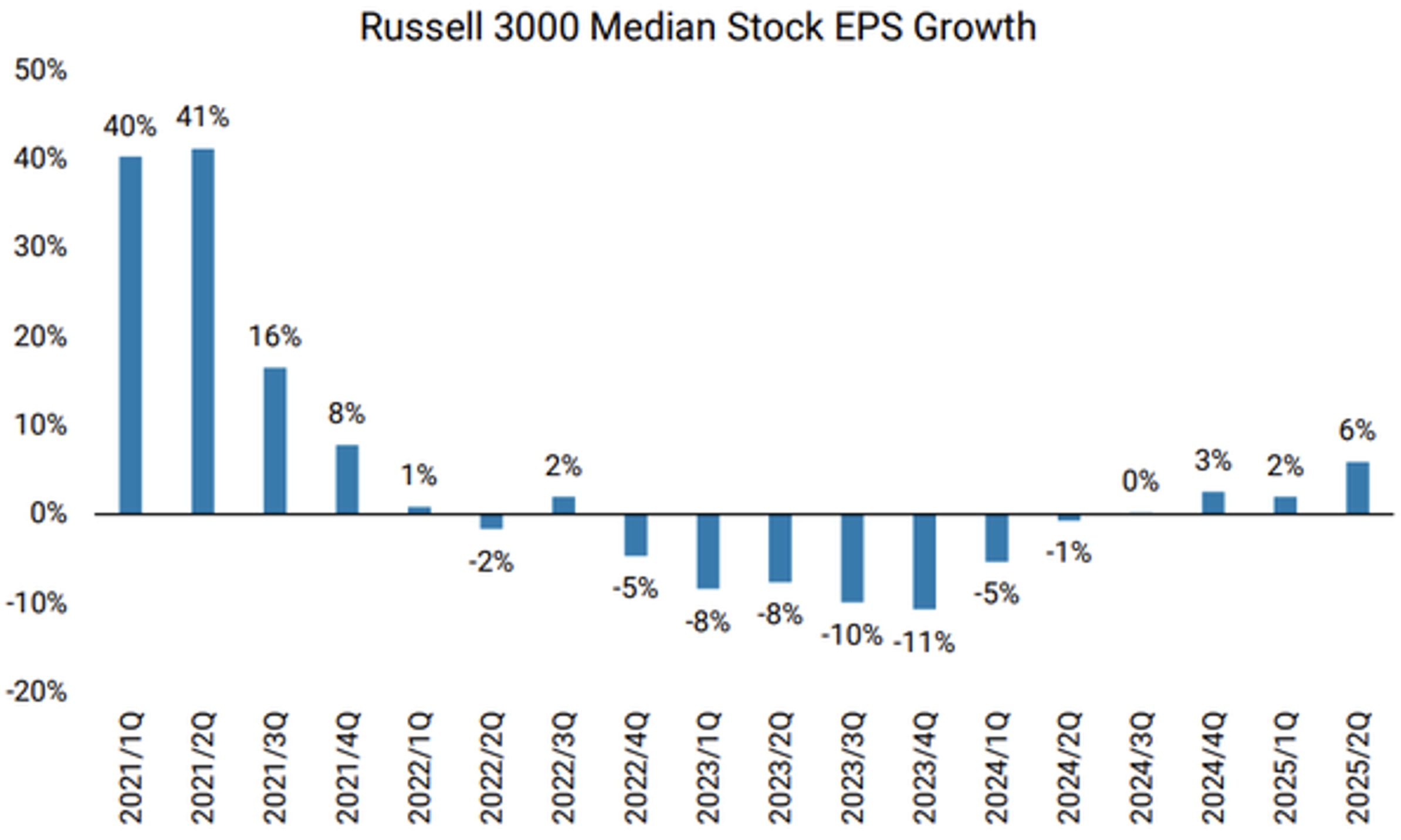

Source: Compustat, Morgan Stanley Research

Exhibit 1 underscores this trend: EPS growth for the median stock in the Russell 3000, negative for much of the last three years, has turned positive.

The recent decline in bond yields has also been a key driver of equity broadening, providing support for long-duration sectors such as small-cap, REITs, and biotech. Policy developments are further enhancing this backdrop, with new federal legislation allowing businesses to deduct the full cost of eligible assets in the year they are placed in service. This accelerates deductions, reduces taxable income, and improves cash flow for smaller firms.

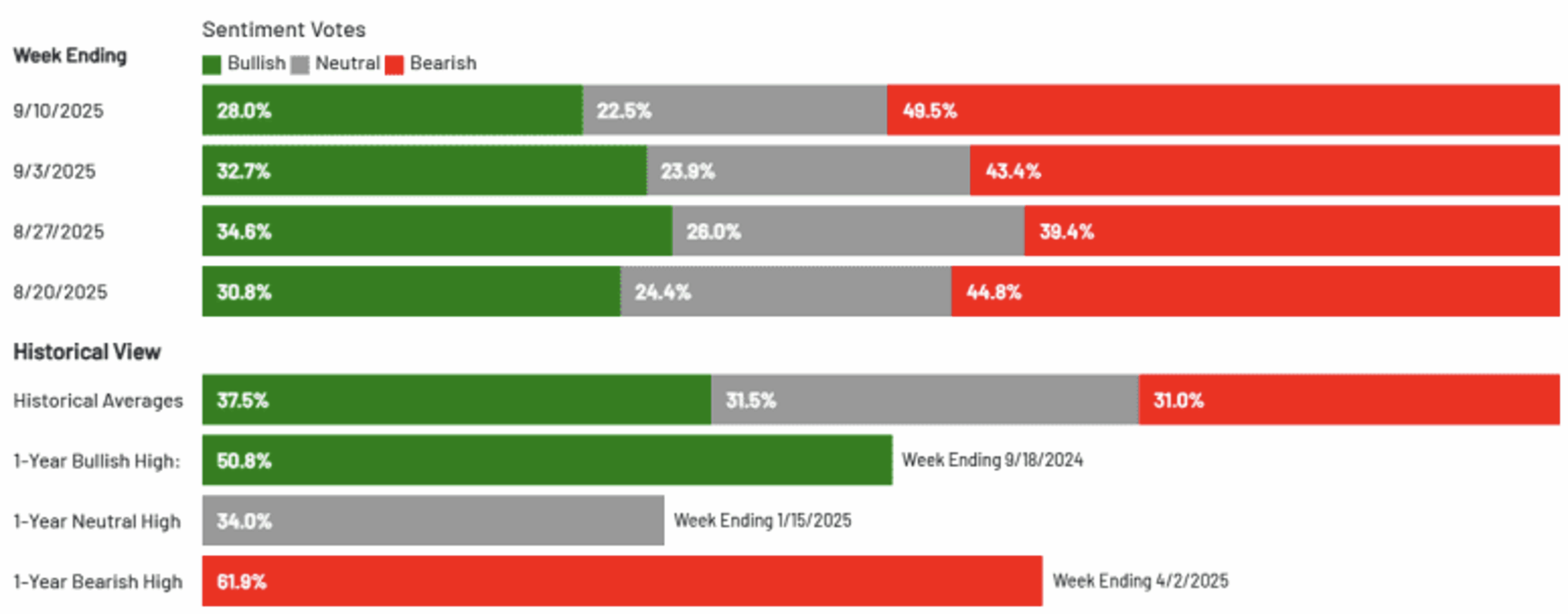

Despite these positives, sentiment remains restrained. American Association of Individual Investors (AAII) surveys show investor sentiment muted compared to historical averages, while CNN’s Fear and Greed Index remains in neutral territory. While speculative excesses are visible in pockets of the market, overall sentiment is still well within normal ranges.

Source: American Association of Individual Investors (AAII) as of 9/10/2025

Fixed Income

Bond markets delivered solid gains in August, aided by weaker labor market data. The 10-year Treasury rose 1.58%, Bloomberg US Corporate Investment Grade Index gained 1.01%, Bloomberg US Mortgage Backed Securities Index climbed 1.61%, and Bloomberg US Corporate High Yield Index advanced 1.25%. The outlier was the long end of the curve, with 30-year Treasuries slipping -0.09%.

Labor data drove much of the rally. Non-Farm Payrolls showed just 22,000 jobs added in July, a steep drop from June’s 79,000 gain. June was revised to a loss of 13,000 jobs, marking the first monthly job loss since 2020. May’s figures were also revised sharply lower, from 144,000 to just 19,000, resulting in a cumulative downward adjustment of 258,000 jobs over May and June. More significantly, the Bureau of Labor Statistics’ annual benchmark revision reduced job totals for the year ending March 2025 by 911,000, the largest such revision in history. These developments highlight the profound impact of recent immigration policy shifts on labor force dynamics.

Citadel Securities notes that with a three-month average payroll gain of only 29,000, one would normally expect a sharper rise in unemployment. Instead, the breakeven level of payroll growth appears to have shifted closer to 50,000, reflecting reduced net migration under current policies. With labor force growth now negative, potential GDP growth has slowed from 2.5% to just 0.6% in the past year.

Despite these long-term headwinds, near-term economic momentum remains resilient. Consensus GDP growth estimates for 2026 are being revised higher, supported by easier financial conditions, robust PMI data, strong new orders, fiscal stimulus, and an FOMC poised to cut rates.

Federal Reserve Policy OUtLOOK

All eyes are on the Federal Reserve, which is widely expected to lower rates at its September meeting. The key question for investors is not whether the Fed cuts, but how dovish the outlook will be for additional easing. Policymakers remain caught between their dual mandates: maintaining price stability near 2% inflation while promoting maximum employment.

Today’s environment complicates this balancing act. The economy is bifurcated, high-income households continue to thrive, while middle- and lower-income consumers remain under strain. As Wells Fargo CEO Charles Scharf recently noted, “There is this big dichotomy between higher-income and lower-income consumers, which continues and is a real issue… The low end is spending the money they have. Their balances are below pre-pandemic levels. They are living on the edge.”

This divergence underscores how dependent the economy has become on affluent households. The wealthiest 10% of Americans now control 87% of US equities and account for a record 50% of consumer spending. As the Fed begins its easing cycle with markets at all-time highs, it risks fueling asset bubbles. History suggests we are not there yet, but the conditions are potentially forming.

LONGER-TERM CONSIDERATIONS

Looking further out, a stagnating labor force raises the stakes for productivity gains. Advances in artificial intelligence and automation will be critical to offsetting slower population growth. Without them, the risk of wage-driven inflation, squeezed profit margins, and liquidity pressures from an aging population could weigh heavily on future economic performance.

Disclosures:

Investing involves risk, including possible loss of principal. Past performance does not guarantee future results. No strategy, including diversification, ensures a profit or prevents loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Please refer to Important Disclosures | Glossary

KAM20250912

Related Perspectives

View All-

Monthly Market Commentary – February 2026

Risk assets delivered mixed but generally positive results in November as investors weighed softer labor data, the ongoing government shutdown, and the prospect of another Federal Reserve rate cut in December.

-

Strategy Review – February 2026

Risk assets delivered mixed but generally positive results in November as investors weighed softer labor data, the ongoing government shutdown, and the prospect of another Federal Reserve rate cut in December.