Kensington Monthly Commentary – October 2025

Monthly Market Commentary

By Kensington Asset Management Team

Stock Market

The stock market continued its advance in October, with the major cap-weighted indices all posting positive returns. The S&P 500 gained 2.27%, the Nasdaq 100 was up 4.77%, and the Russell 2000 added 1.76%. Foreign markets moved higher as well, with the EuroStoxx 50 up 2.39%, the MSCI EAFE Index gaining 3.41%, and MSCI Emerging Markets Index up 4.61%.

Under the surface, however, market breadth was weaker. The S&P 500 Equal-Weight Index was actually down for the month, returning -1.04%. Even so, it still looks too early to call a meaningful top, and our models remain in a Risk-On posture.

Earnings reports for the third quarter have been far better than anticipated. According to FactSet, the S&P 500 earnings growth rate for the third quarter, which was estimated to be 7.3% at the beginning of the quarter, has risen to approximately 12%. This marks the fourth straight quarter in which the index has delivered double-digit year-over-year earnings growth.

Four sectors have done most of the heavy lifting: Information Technology, Utilities, Financials, and Materials. Technology, Utilities, and Materials are being propelled by the AI capital-expenditure boom along with advantageous changes in tax policy. Financials, meanwhile, are benefiting from wider net interest margins as funding costs move lower.

The strong earnings backdrop has not gone unnoticed. The forward 12-month P/E ratio of 23.1 (as of October 29) was the highest in more than five years and not far below the market’s peak P/E ratio of the past 30 years of 24.4. Those elevated P/E ratios are being driven higher largely by the technology sector, as illustrated in the chart below.

Source: Topdown Charts, LSEG | TMT – 12 month Trailing

Looking ahead to 2026, the Street expects earnings growth to remain robust, with double-digit year-over-year increases anticipated in each of the four quarters.

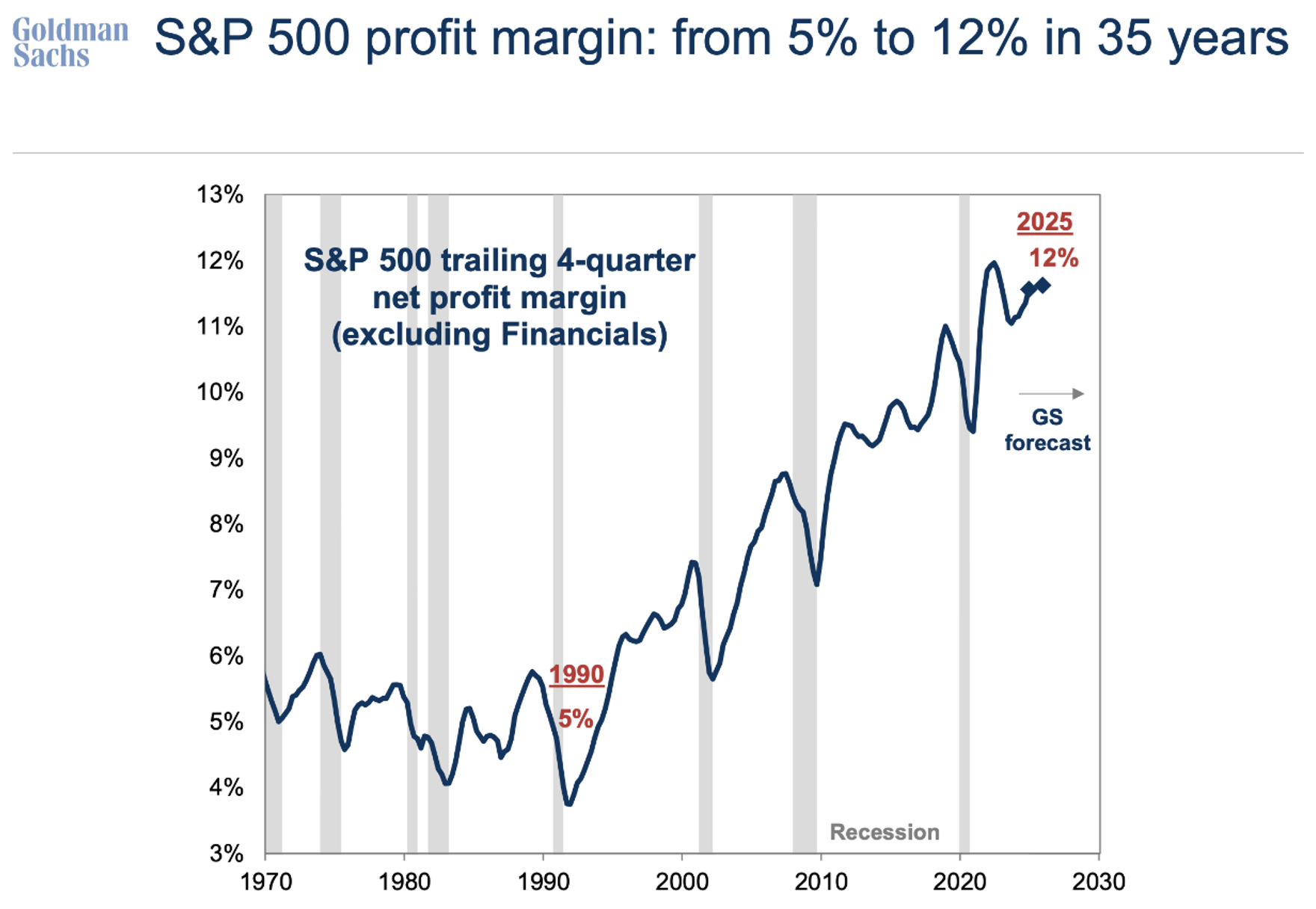

Breaking it down further, analysts are projecting S&P 500 revenue growth of 6.6% in 2026, a notable step up from this year’s estimated growth of 4.3%. At the same time, net profit margins are expected to reach record levels, extending the impressive long-term upward trend shown in the chart below. This combination of faster top-line growth and record margins leaves the market heavily reliant on continued strong execution to justify current valuations.

Source: FactSet, Goldman Sachs Global Investment Research

FIXED INCOME

Bond markets posted modest gains in October. The benchmark 10-year Treasury returned 0.77%, the Bloomberg Corporate Investment Grade Index rose 0.38%, the Bloomberg Mortgage-Backed Securities Index gained 0.86%, and the Bloomberg High Yield Index was essentially flat, up 0.16%. The 30-year Treasury led the way, returning 1.36% for the month.

Overall, fixed income has delivered solid results this year, supported by lower-than-expected inflation and a pronounced decline in price volatility since early April. The drop in volatility matters not only for risk and return, but also for overall market liquidity. Since financial markets are heavily reliant on leverage, the amount of collateral required depends on both the value and the perceived riskiness of the underlying assets.

As fixed income volatility has subsided, lenders have been more willing to extend credit, effectively increasing investors’ purchasing power. That easier access to financing has, in turn, helped support higher bond prices across sectors.

Federal Reserve and Monetary Policy

On October 29th, Chairman Powell noted that another quarter-point cut in December is “not a foregone conclusion” and emphasized that policy is “not on a preset course.” He highlighted “strongly differing views” within the committee on both the current stance of policy and the appropriate pace of further easing.

One of the more dovish voices, Governor Stephen Miran, has argued that the Fed may be overestimating inflation and underestimating softness in the labor market, leaving policy too restrictive. His key point on inflation is that housing, which makes up more than 30% of the CPI basket, is still being measured using lagged estimates of Owners’ Equivalent Rent, even as more timely rent data have cooled. In his view, this lag means reported inflation is running hotter than underlying reality, giving the Fed room to cut more aggressively without risking a renewed inflation surge. (November 3, 2025)

For now, Miran’s outlook represents a minority view, and the committee as a whole remains data-dependent rather than pre-committed to a faster easing path. The larger takeaway for investors is that policy uncertainty remains high, and shifts in the inflation data – particularly in shelter – could have an outsized influence on rate expectations and asset prices into year-end.

Disclosures:

Investing involves risk, including possible loss of principal. Past performance does not guarantee future results. No strategy, including diversification, ensures a profit or prevents loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Please refer to Important Disclosures | Glossary

KAM20251114A

Related Perspectives

View All-

Strategy Review – January 2026

Risk assets delivered mixed but generally positive results in November as investors weighed softer labor data, the ongoing government shutdown, and the prospect of another Federal Reserve rate cut in December.

-

Monthly Market Commentary – January 2026

Risk assets delivered mixed but generally positive results in November as investors weighed softer labor data, the ongoing government shutdown, and the prospect of another Federal Reserve rate cut in December.