KHPI’s Fiscal Year 2025 Review and the Power of Net-of-Tax Performance

Monthly Market Commentary

By Kensington Asset Management Team

The following is for informational purposes only and not construed as tax advice. Please consult with a tax professional for your specific situation.

For the modern fiduciary, performance is a multi-dimensional metric. While investment returns capture headlines, the sophisticated advisor understands that true performance is often measured by what their clients take home. For investors in taxable accounts, the “tax drag” of some traditional income strategies — the taxes paid each year on dividends, interest, and realized gains– can erode the compounding clients seek.

The Hidden Cost of Traditional High-Yield Strategies

Traditional higher-yielding strategies, including high-yield credit, certain Equity Linked Notes (ELNs), and standard covered-call option funds, often generate distributions classified as ordinary income. For investors in taxable accounts, these distributions can add to their potential year-end tax liability and impact overall returns.

Traditional Higher-Yielding Strategies create two potentially distinct disadvantages:

- Part of each distribution is lost to taxes due to tax liability created as ordinary income.

- When distributions are taxed as ordinary income, less cash is available to reinvest, reducing long‑term compounding.

How KHPI aims to reduce tax drag?

The Hedged Premium Income ETF (KHPI) helps reduce year-to-year tax drag by altering the character of its distributions. The approach is built on two-pillars:

- Maintains a long-term position in an ETF tracking the S&P 500 so most equity gains accrue as unrealized gains, generally not taxed until you sell.

- Use a call-spread strategy to generate option-premium income and a put-spread strategy to help hedge downside risk. This premium is realized on a regular schedule (monthly or quarterly) and helps fund the distribution.

How do these components help reduce tax drag?

KHPI’s lower current‑year tax drag comes from a timing mismatch. The core S&P 500 ETF tends to build unrealized gains (no current tax), while the options overlay may realize gains and losses during the year. In a rising market, the overlay often realizes losses while the equity position appreciates. That mix allows part of the cash paid out to be classified as Return of Capital (ROC) rather than ordinary income—so less is taxed in the current year and more stays invested to compound.

Fiscal Year 2025 Performance Spotlight

In FY2025, KHPI delivered a positive return while keeping distributions tax-efficient for investors in taxable accounts.

As of 12/31/2025

| 1 YEAR (Annualized) | Since Inception – 9/3/24 (Annualized) | |

| NAV total return | 11.14% | 11.69% |

| Market Price total return | 11.30% | 11.58% |

Performance data quoted represents past performance and does not guarantee future results. Investment return and principal value will fluctuate; shares may be worth more or less than their original cost when sold. Current performance may be lower or higher than the performance data quoted. For most‑recent month‑end performance, visit https://www.kensingtonassetmanagement.com/solutions/etfs-khpi/ or call (866) 303‑8623. Returns assume reinvestment of distributions and are shown net of fees.

Distributions & yield (FY2025)[1]

| Total 2025 Distribution | $2.28 per share |

| Distribution Rate[2] | 9.00% |

| 30-Day SEC Yield[3] | 0.21% |

[1] Distribution amounts and tax character are determined after year‑end and reported on Form 1099‑DIV. Managed distributions may include net investment income, realized gains, and/or return of capital.

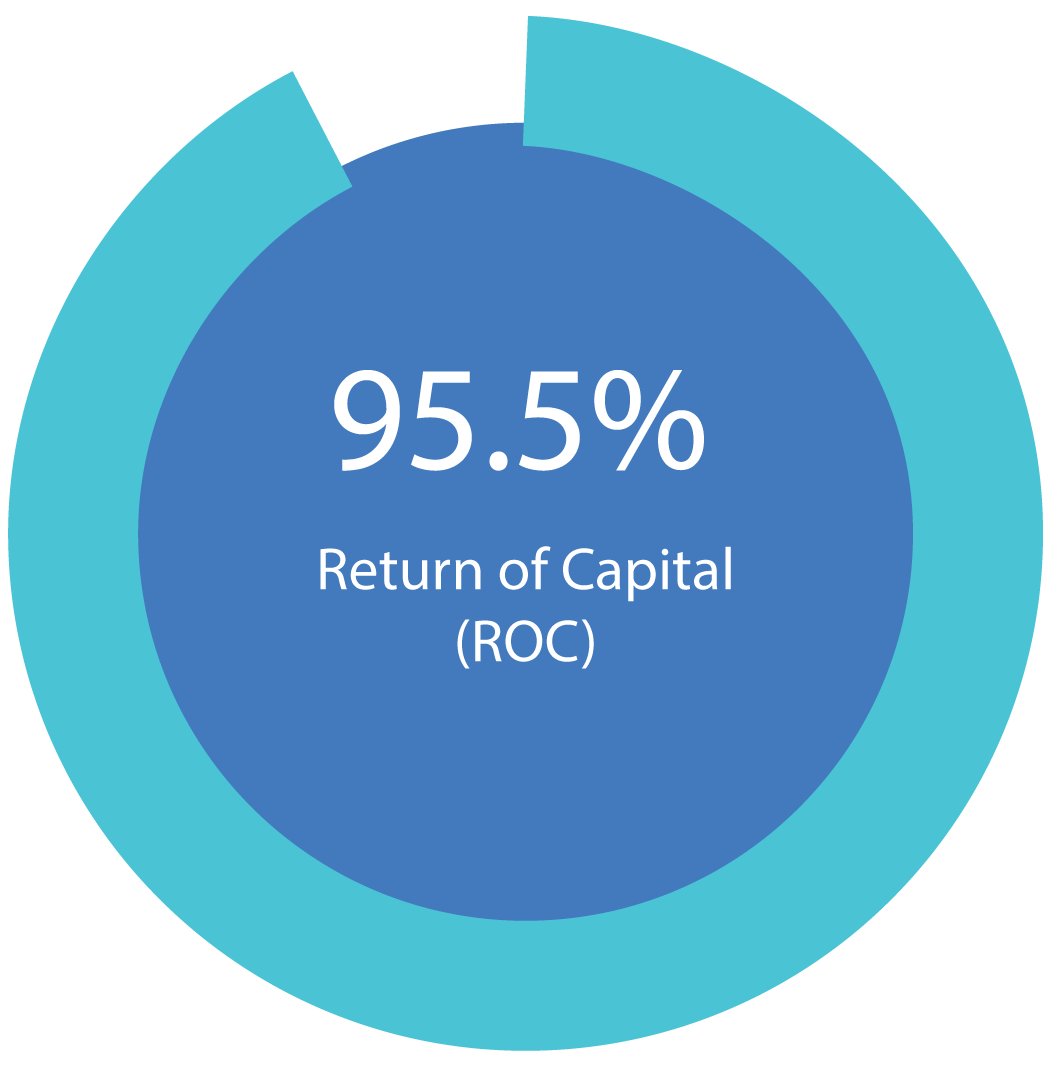

[2] KHPI’s distribution policy allocates a set 9% per annum of the Fund’s net asset value to shareholders, payable on a monthly basis. As of the year ended December 31, 2025, approximately 5% of the Fund’s distributions were considered net investment income and the remaining approximate 95% of the distributions were considered return of capital.

2025 Tax Characterization Breakdown (final 1099-ddiv)[4]

| Distribution Type | % of FY2025 Total | Tax Treatment |

| Return of Capital (ROC) | 95.5% | Not taxable when paid It reduces cost basis and defers taxes until shares are sold (if basis ever hits zero, further ROC is taxed as capital gains in that year). |

| Qualified Dividend Income (QDI) | 4.5% | Taxed as long-term capital gains rates if holding-period requirements are met[5] |

| Ordinary Income | 0.0% | Taxed as ordinary income rates[5] |

What ROC means?

ROC is tax deferral, not tax elimination. A ROC is not taxed when paid; it reduces cost basis and defers tax until sold. If basis falls to zero, any further ROC is taxed as capital gain in that year. Reinvested ROC still reduces basis.

Why investors may care?

- Lower current‑year tax drag: Less of each dollar goes to taxes in the year paid.

- More to compound: Keeping more capital invested can support long‑term growth (tax is due later, typically at sale).

- Potential step‑up at death: Many taxable assets receive a step‑up (or step‑down) in basis for heirs, which can eliminate deferred gains.

[3] The 30-Day SEC Yield represents net investment income, which excludes option income, earned by the ETF over the 30-Day period, expressed as an annual percentage rate based on such ETF’s share price at the end of the 30-Day period. Distributions are not guaranteed. [4] Final tax character is determined after year end on Form 1099 DIV (e.g., Box 3 ROC, Box 1 ordinary/QDI, Box 2a capital gain). Mid year notices are estimates and can be reclassified. [5] May also be subject to the 3.8% Net Investment Income Tax (NIIT) for higher income investors.

KHPI seeks to deliver steady, managed distributions and current income with the potential for capital appreciation. KHPI’s structure can result in ROC and QDI distributions, which may lower current-year taxes and leave more invested to compound.

As we look toward the remainder of 2026 and beyond, we remain focused on outcomes that matter most to investors.

Investors should consider the investment objectives, risks, charges and expenses of the Kensington Hedged Premium Income ETF (KHPI) before investing. KHPI’s prospectus and summary prospectus contain this and other information about KHPI may be obtained by calling 1(866) 303-8623 / visiting our website, which should be read carefully. There is no guarantee KHPI will achieve its investment objectives. Please read carefully. There is no guarantee any investment strategy will generate a profit or prevent a loss. Index performance does not represent KHPI’s performance. It is not possible to invest directly in an index. KHPI is managed by Liquid Strategies, LLC (LS) through a sub-advisory agreement with Kensington Asset Management, LLC (KAM). KAM is the adviser to the KHPI, distributed by Quasar Distributors, LLC. KAM and LS are not affiliated with Quasar.

Risk Factors: KHPI invests in options that derive their performance from the performance of the S&P 500 Index. Selling (writing) and buying options are speculative activities and entail greater than ordinary investment risks. KHPI use of put options can lead to losses because of adverse movements in the price or value of the underlying asset, which may be magnified by certain features of the options. When selling a put option, KHPI will receive a premium; however, this premium may not be enough to offset a loss incurred by KHPI if the price of the underlying asset is below the strike price by an amount equal to or greater than the premium. Purchased put options may expire worthless and KHPI would lose the premium it paid for the option. KHPI may lose significantly more than the premiums it receives in highly volatile market conditions. KHPI will invest in short term put options which are financial derivatives that give buyers the right, but not the obligation, to sell (put) an underlying asset at an agreed-upon price and date. KHPI’s use of options may reduce KHPI’s ability to profit from increases in the value of the underlying asset. KHPI could experience a loss or increased volatility if its derivatives do not perform as anticipated or are not correlated with the performance of their underlying asset or if KHPI is unable to purchase or liquidate a position. KHPI was recently organized and has no operating history. As a result, investors have a limited track record on which to base their investment decision. Investments involve risk including the possible loss of principal. Investing in ETFs involves risk, including loss of principal. Risks specific to the KHPI are detailed in the prospectus and include Management Risk, Equity Risk, ETF Risks, Tax Risk, Market Risk, Underlying Funds Risk, Derivative Risk (Futures Contract, Swap Agreement, Options), Short Sale Risk, Leverage Risk, Limited History of Operations Risk, Non-Diversification Risk, and Turnover Risk. For a summary of these risks, please visit: KHPI Risks.

Tax treatment varies by investor and may change. Final distribution character (ordinary income, capital gains, and/or return of capital) is determined after year‑end and reported on Form 1099‑DIV. For guidance specific to your situation, consult a tax professional.

Due to its investment strategy, the KHPI’s distributions are expected to exceed its taxable income and capital gains realized during a taxable year. Consequently, all or a portion of the distributions made in the same taxable year may be recharacterized as a return of capital to shareholders. A return of capital distribution will generally not be taxable, to the extent of each shareholder’s basis in KHPI’s shares but will reduce each shareholder’s cost basis in KHPI and result in a higher reported capital gain or lower reported capital loss when those shares on which the distribution was received are sold. If the return of capital distribution exceeds a shareholder’s cost basis, the excess amount will be capital gain, assuming you held your shares as a capital asset, and will be long-term or short-term capital gain depending on how long you have held your KHPI shares.

For more information about terms used in this article, please visit our Glossary at https://www.kensingtonassetmanagement.com/glossary/.

Related Perspectives

View All-

KENSINGTON SPOTLIGHT SERIES: THE DEFENDER STRATEGY

At Kensington Asset Management, we’ve actively managed fixed income solutions for clients for over three decades. Throughout this journey, we’ve weathered all types of macroeconomic regimes from extreme market volatility events to periods of steady growth.

-

White paper: Trend Following and Tail Risk

An introductory understanding of how trend following can manage tail risk.