March 2025: TARIFFS, TUMULT, AND A SHIFT IN SENTIMENT

Monthly Market Commentary

By Kensington Asset Management Team

Stock Market: A Correction

Takes Hold

A market correction took hold in March with equity indices falling across the board. The S&P 500 dropped -5.75%, the Nasdaq 100 -7.69%, and the Russell 2000 -6.99%. Foreign markets fared better, with the EuroStoxx 50 down -3.94% and the MSCI EAFE down -2.77%.

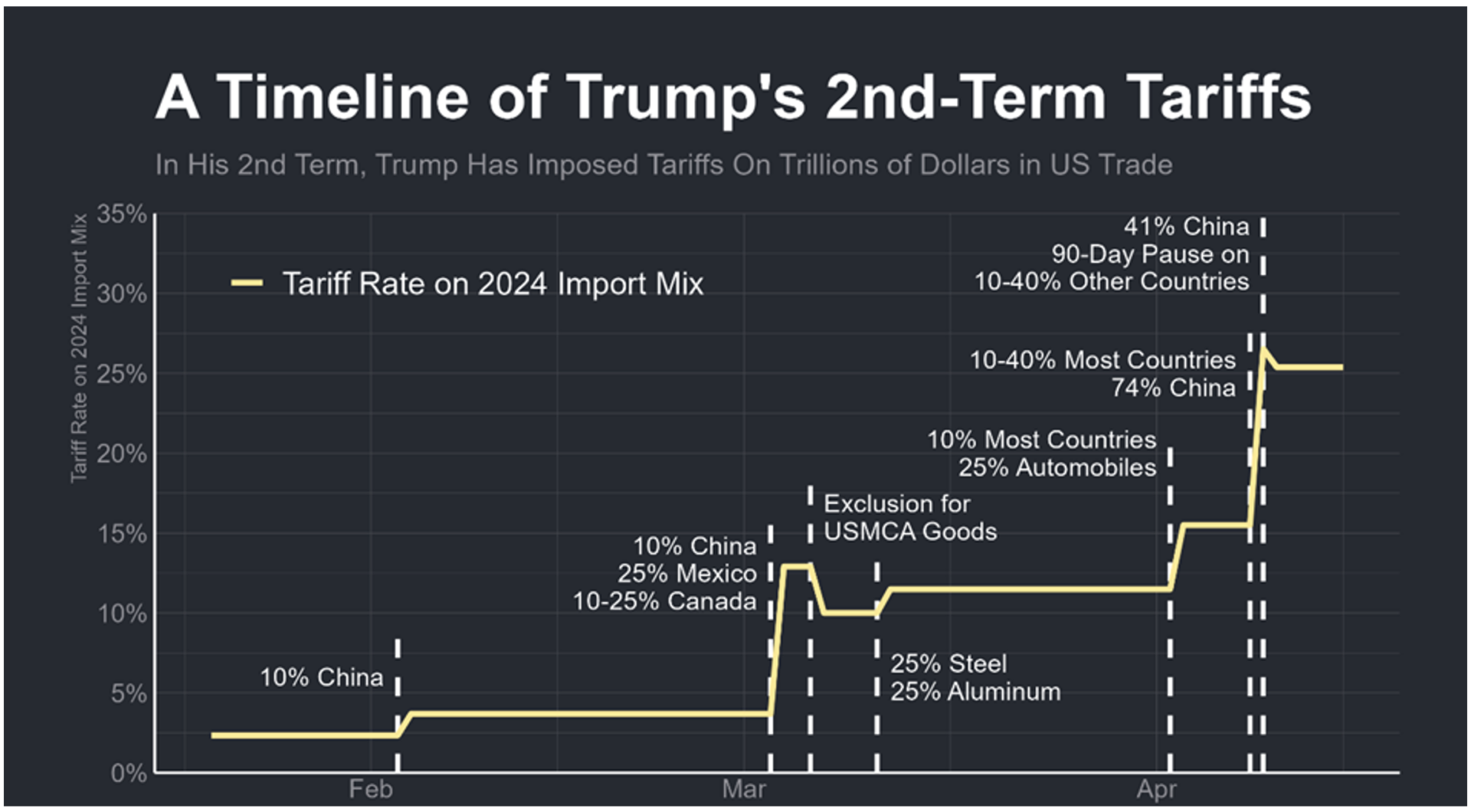

Investors were rattled by the Trump Administration’s ambitious effort to reset trade policy, including threats to raise trade levies to levels unseen since 1910. Economist Joey Politano estimates the effective US tariff rate is now 25%, roughly 10 times higher than before Trump took office.

Source: Apricitas Economics as of April 12, 2025

BROAD-BASED CONCERNS

Market participants and business leaders expressed concern not just over the scale of the tariffs, but also their execution:

- The punitive approach taken prior to the start of any negotiations

- Its indiscriminate application to ally and adversary nations alike

- The potential for reciprocal tariffs

- Potential impact on global growth and overall market stability

- Remote possibility of a global trade war similar to what took place in the 1930s under the Smoot-Hawley Act leading to the Great Depression

The Administration’s limited clarity has amplified volatility. Conflicting messages and poorly explained policy mechanisms have fueled confusion, leaving both Wall Street and Main Street on edge. Businesses are increasingly pausing investment decisions, waiting for more direction.

SHOCK AND PAUSE DIPLOMACY

The Administration’s strategy appears to be one of “shock and awe,” paired with urgent calls for trade negotiations. A recently announced 90-day pause in new tariffs offers a window to establish a framework with affected trade partners. However, expectations were muted. Overhauling global trade structures built over decades is a long-term process, one unlikely to align with the White House’s accelerated timeline.

This mismatch has forced global investors to reassess US exposure, contributing to the recent selloff and a potential rebalancing of long-held portfolio weightings.

FIXED INCOME: VOLATILITY RETURNS

The bond market offered mixed results in March. Short-term Treasuries posted modest gains, the 10-year was relatively flat, and the 30-year fell -1.38%. Bloomberg US Mortgage-Backed Securities Index was mostly unchanged, while US Corporate Investment-Grade Bond Index slipped -0.29% and US Corporate High Yield Index declined -1.02%.

TREASURIES AND THE GLOBAL WEB OF RISK

Bond markets saw a meaningful uptick in volatility toward the end of the month as investors attempted to digest multiple potential outcomes from a tariff policy that may mark the end of the post-WW II international economic order.

Given global interest rates key off the US Treasuries, major disruption in the latter has an outsized impact on economic activity around the world. In addition, Treasuries serve as the principal collateral securing a daisy chain of highly levered transactions totaling in the trillions of dollars. When that collateral value is impaired due to a large and unexpected jump in yields, the unwinding of such trades can result in huge losses that flow through the entire financial system, threatening to bring it to a halt. If businesses are unable to refinance loans at reasonable and planned for cost, the end result can be outright defaults, threatening the onset of a severe recession.

UNCERTAINTY BREEDS SELLING

Much of this risk is hidden. Uncertainty in markets is magnified by the fact most market participants lack the ability to see how other participants are positioned, compounded by the fact many of those participants are highly levered. When fear spreads, the impulse is to sell first. Risk managers, facing opaque exposures, often preemptively liquidate positions or call-in margin. It’s not difficult to see how these incentives can result in a negative price spiral (selling begetting more selling) – which is what financial authorities should want to avoid at all cost.

This environment is further destabilized by geopolitics:

- Treasury holders abroad may act in ways misaligned with US interests

- Some nations may sell Treasuries to pressure Washington

- Higher tariffs risk higher inflation, adding upward pressure on yields

The dollar’s recent decline is one symptom of lost global confidence. A weaker dollar boosts import prices, feeding inflation and complicating the Fed’s job.

MONETARY POLICY: A DELICATE BALANCING

Fed Chair Jerome Powell has remained steady, reiterating that monetary policy will be guided by data. While President Trump has called for rate cuts, Powell has resisted, pointing to strong economic data and warning of the inflationary effects of tariffs.

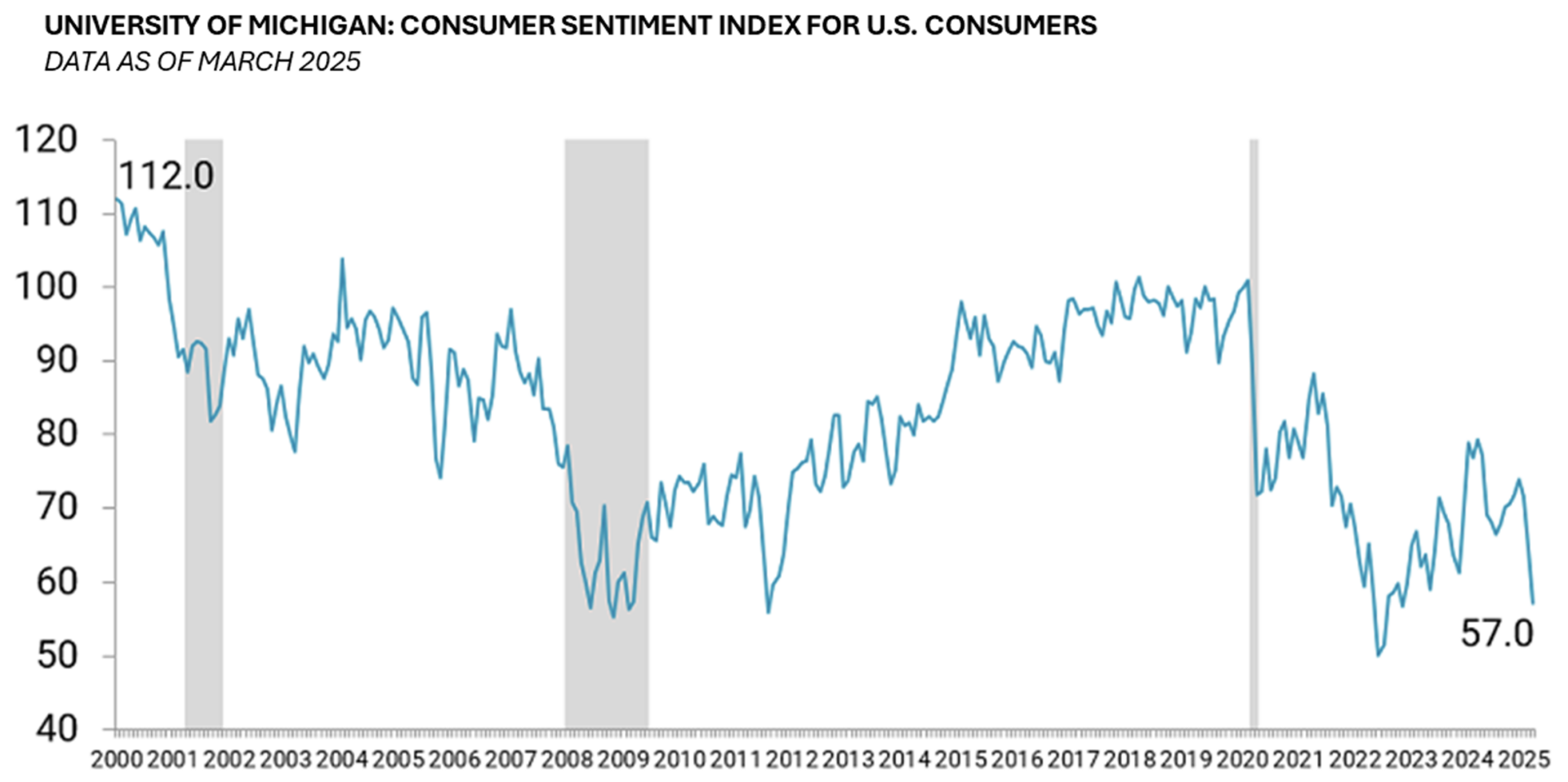

But the economy is clearly in transition. Consumer sentiment, according to the University of Michigan, has dropped to the second-lowest level on record. Inflation expectations have surged to multi-decade highs. Even among Independents and Republicans, confidence has waned. Business confidence is down sharply as executives delay capital expenditures until policy clarity improves.

Source: Callahan Associates as of March 2025

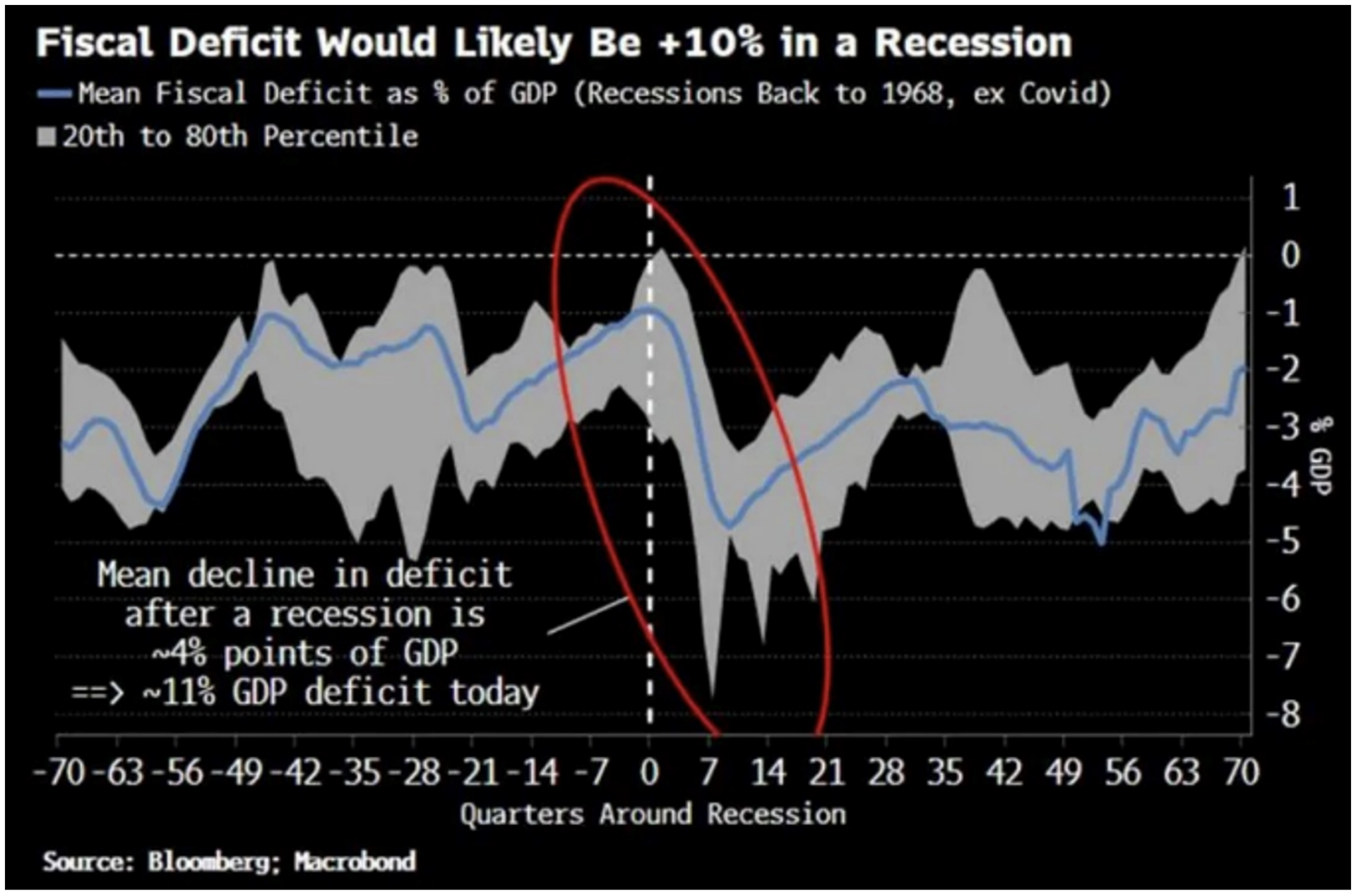

While all this suggests the Fed will look to ease monetary policy soon rather than later, they are constrained by the fact a recession would increase the size of the fiscal deficit, placing upward pressure on both inflation and interest rates once the economy recovers.

CONCLUSION: CAUTION AHEAD

March marked a turning point. Markets are adjusting to a new regime of policy unpredictability, higher inflation risk, and geopolitical tension. Tariff headlines and Fed independence are now central concerns for investors.

For now, the prudent approach is to stay defensive. Risk premiums are rising, volatility is back, and clarity from Washington remains elusive. Patience and vigilance will be essential in the months ahead.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular strategy such as the types of securities being substantially different.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Definitions:

Bloomberg US Corporate Investment Grade Index: An unmanaged index that covers the publicly issued US corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered.

Bloomberg US Corporate High Yield Index: An unmanaged market value-weighted index that covers the universe of fixed-rate, non-investment grade debt in the US. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

Bloomberg US Mortgage-Backed Securities (MBS) Index:An unmanaged index that tracks fixed-rate agency mortgage-backed pass-through securities guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The index is constructed by grouping individual TBA-deliverable MBS pools into aggregates or generics based on program, coupon, and vintage.

Euro Stoxx 50 Index: A market capitalization-weighted stock index that represents the 50 largest blue-chip European companies operating within the eurozone nations

MSCI EAFE Index:An international equities market index that consists of large and mid-cap stocks across developed markets in Europe, Australasia, and Far East Asia. Excludes US and Canadian equities.

NASDAQ 100 Index: A market index that comprises of the 100 largest, most actively traded companies listed on the Nasdaq stock exchange.

Russell 2000 Index: A market index that consists of 2,000 small-cap US companies that are part of the larger Russell 3000 Index.

S&P 500: A capitalization weighted index of 500 stocks representing all major domestic industry groups. The S&P 500 TR Index assumes the reinvestment of dividends and capital gains.

KAM20250414

Related Perspectives

View All-

Strategy Review – June 2026

March was shaped by a sharp escalation in US-Iran tensions, a surge in energy prices, and renewed concern that inflation could stay stickier than expected. The Federal Reserve again held rates steady, while higher oil prices and rising yields pressured traditional risk assets.

-

Monthly Market Commentary – June 2026

June’s central tension was that positive US economic data coincided with weakness in certain large-cap equities.