Navigating Uncertainty Amid Market Opportunities

Market Insights

By Brian Weisenberger, CFA, Senior Market Strategist

Market Insights is a piece in which Kensington’s Portfolio Management team will share interesting and thought-provoking charts that we believe provide insight into markets and the current investment landscape.

Q3 Earnings Season

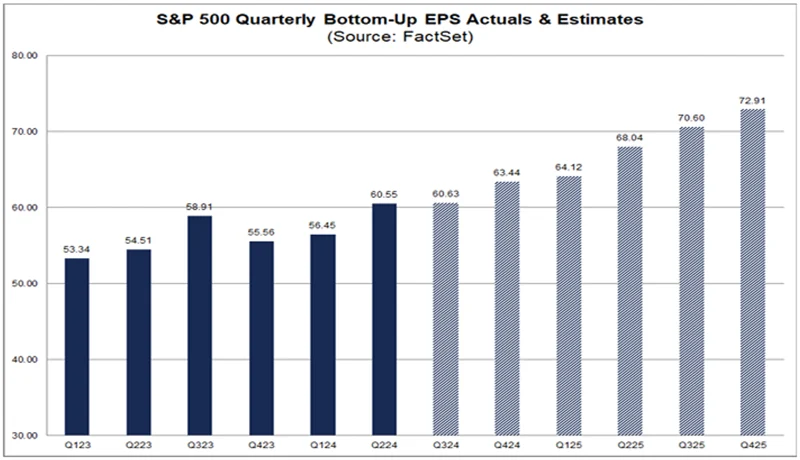

Q3 earnings season kicks off this week with the S&P 500 expected to deliver a solid 4.2% year-over-year growth rate (chart below). While estimates have come down significantly from an anticipated 7.8% growth rate on June 30, a 4.2% growth rate would mark the 5th consecutive quarter of positive growth for the index and help ease any short-term concerns about a slowing economy.

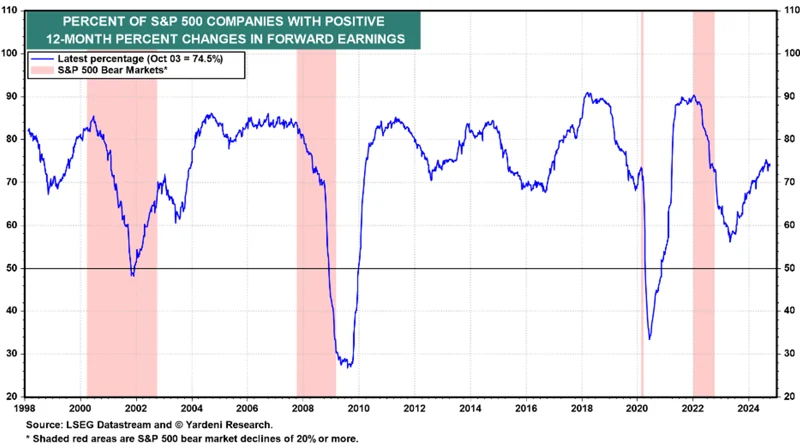

Even more encouraging than the headline number is the expanding breadth of companies within the index contributing to the gains (chart below). Nearly 75% of S&P 500 companies are anticipated to announce a positive change in forward earnings, a stark improvement from 2023, when fewer than 60% of companies reported such growth, as the Information Technology sector primarily propped up markets during much of the year.

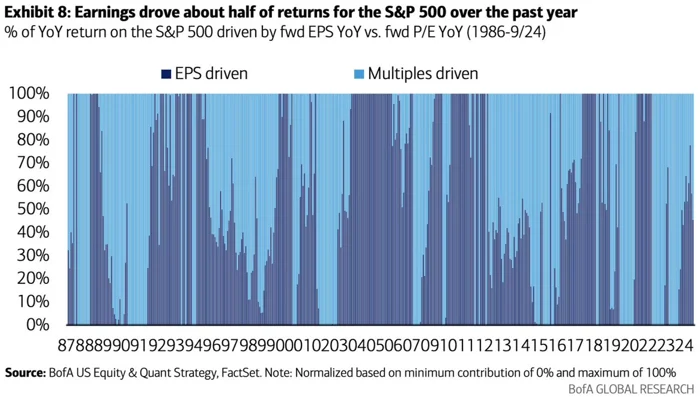

Quarterly earnings always play a crucial role in stock market returns, but they may take on even more significance in the months ahead. While 2023 market returns were largely driven by multiple expansion, earnings have accounted for 45% of the S&P 500’s 12-month returns as of September (chart below).

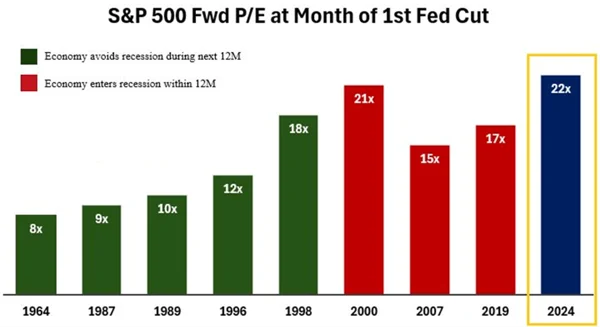

For markets to continue their upward trajectory, that trend will likely need to persist and could be critical in avoiding a recession. As illustrated in the chart below, the S&P 500 Forward P/E at the time of the September rate cut was 22x, the highest multiple seen during an initial rate cut since at least 1964. Although this is a relatively small sample size with only eight previous instances, higher starting multiples have shown some correlation with a recession (highlighted by the red bars). If earnings deliver as expected in the third quarter, it could provide a buffer for market multiples, allowing them to remain steady or even contract without triggering significant drawdowns.

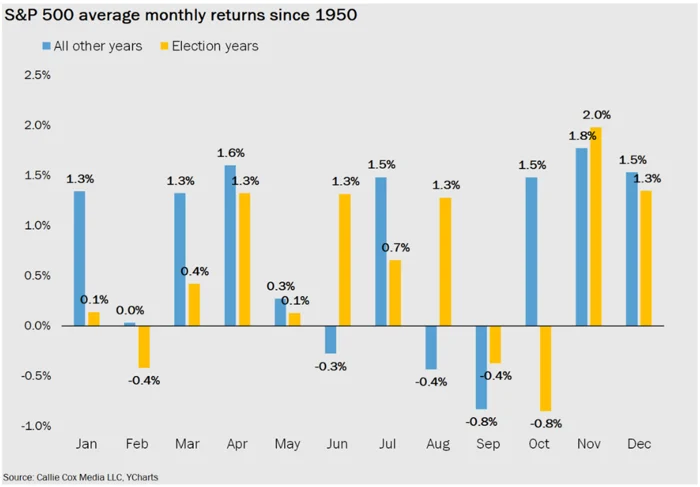

That said, the market is not immune to corrections, especially as we navigate a historically challenging time for equities. While it’s often noted that September is the weakest month for equities, in election years, it’s October that typically lags the most—a significant divergence from non-election years, where October has historically performed well (chart below).

It’s not just historical precedent signaling potential short-term weakness; volatility markets are also flashing warnings. Earlier this week, the CBOE Volatility Index (VIX) surpassed 22, a level that has coincided with S&P 500 losses over the past 18 months (chart below).

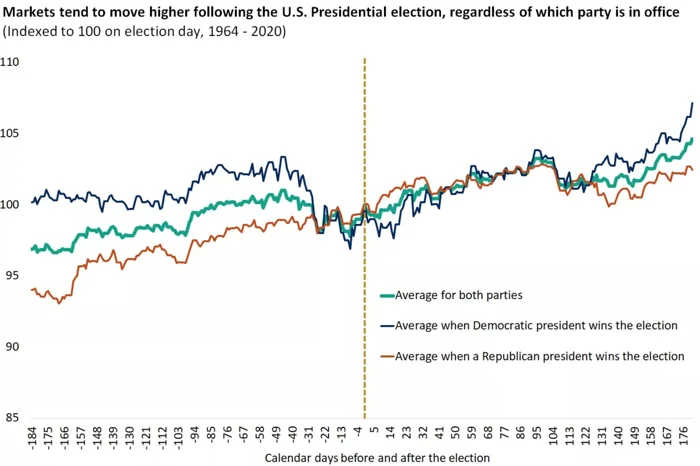

However, viewed from another angle, these instances have also historically presented excellent opportunities to “buy the dip” as volatility later dissipated. History supports this idea as well. As the election year return chart indicates, while October has been weak in election years, November has historically been the best-performing month for the index—election year or not. What’s perhaps most encouraging for election watchers is that, historically, markets tend to rise after the election, regardless of which party wins (chart below).

While there are potential headwinds as we head deeper into earnings season, particularly with the historical volatility surrounding October in election years, the outlook for the broader market remains cautiously optimistic. With earnings growth playing an increasingly pivotal role and strong forward earnings guidance expected from a majority of S&P 500 companies, there is potential for resilience in the face of economic uncertainty. Coupled with the historical trend of market gains in post-election Novembers, investors may find strategic opportunities in the midst of near-term volatility. Staying focused on earnings and macro trends will be key as markets navigate this crucial period.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Related Perspectives

View All-

KHPI’s Fiscal Year 2025 Review and the Power of Net-of-Tax Performance

KHPI’s Fiscal Year 2025 Review and the Power of Net-of-Tax Performance Monthly Market Commentary By Kensington Asset Management Team The following is for informational purposes only and not construed as tax advice. Please consult with a tax professional for your specific situation. For the modern fiduciary, performance is a multi-dimensional metric. While investment returns capture […]

-

KENSINGTON SPOTLIGHT SERIES: THE DEFENDER STRATEGY

At Kensington Asset Management, we’ve actively managed fixed income solutions for clients for over three decades. Throughout this journey, we’ve weathered all types of macroeconomic regimes from extreme market volatility events to periods of steady growth.