The Global Bull

Monthly Market Commentary

By Kensington Asset Management Team

Geopolitics

As we pointed out in our February Commentary, three billion people are expected to head to the electoral polls across several economies over the next two years. The impact on financial markets can be wide ranging, as was evident earlier this month when election results in India were revealed. In a surprise upset, Prime Minister Modi’s BJP party lost its majority in parliament, forcing Modi to work with a National Democratic Party coalition to govern the country. Fearful that Modi’s economic development plan might face increased opposition, investors saw the BSE Sensex Index down as much as 8% before fully recovering in the following days.

Another election surprise occurred in Mexico, where President Obrador was replaced by Claudia Scheinbaum of the ruling Moreno Party, who won by a substantial majority (over 30% margin). Both the Mexican stock market and peso have fallen, with the Mexican Bolsa index down nearly 10% on concerns the new administration will move to put in place market-unfriendly policies.

Turning to Europe, France’s Emmanuel Macron recently called for a surprise snap election, in an effort to test voters’ appetite for the far-right policies of Marine Le Pen or, less likely, those of an amalgamation of far-left parties. For investors, the specter of populists gaining power, whether from the right or left, is cause for concern and the uncertainty around the two-round ballot that concludes on July 7th has sent the CAC Index plummeting, down close to 9% since its peak in mid-May.

stock market

May saw a sharp rebound in equities, reversing the losses seen in April and then some. The S&P 500 Index gained 4.8%, the Nasdaq 100 Index jumped 6.28%, while the small-cap Russell 2000 Index was up 4.87%. Foreign stocks trailed their U.S. counterparts, with the MSCI EAFE gaining 2.46% and the MSCI Emerging Markets up slightly, 0.48%. Proxies for financial conditions (US Dollar, WTI crude oil prices and bond yields) all eased over the course of the month, supportive of higher stock prices.

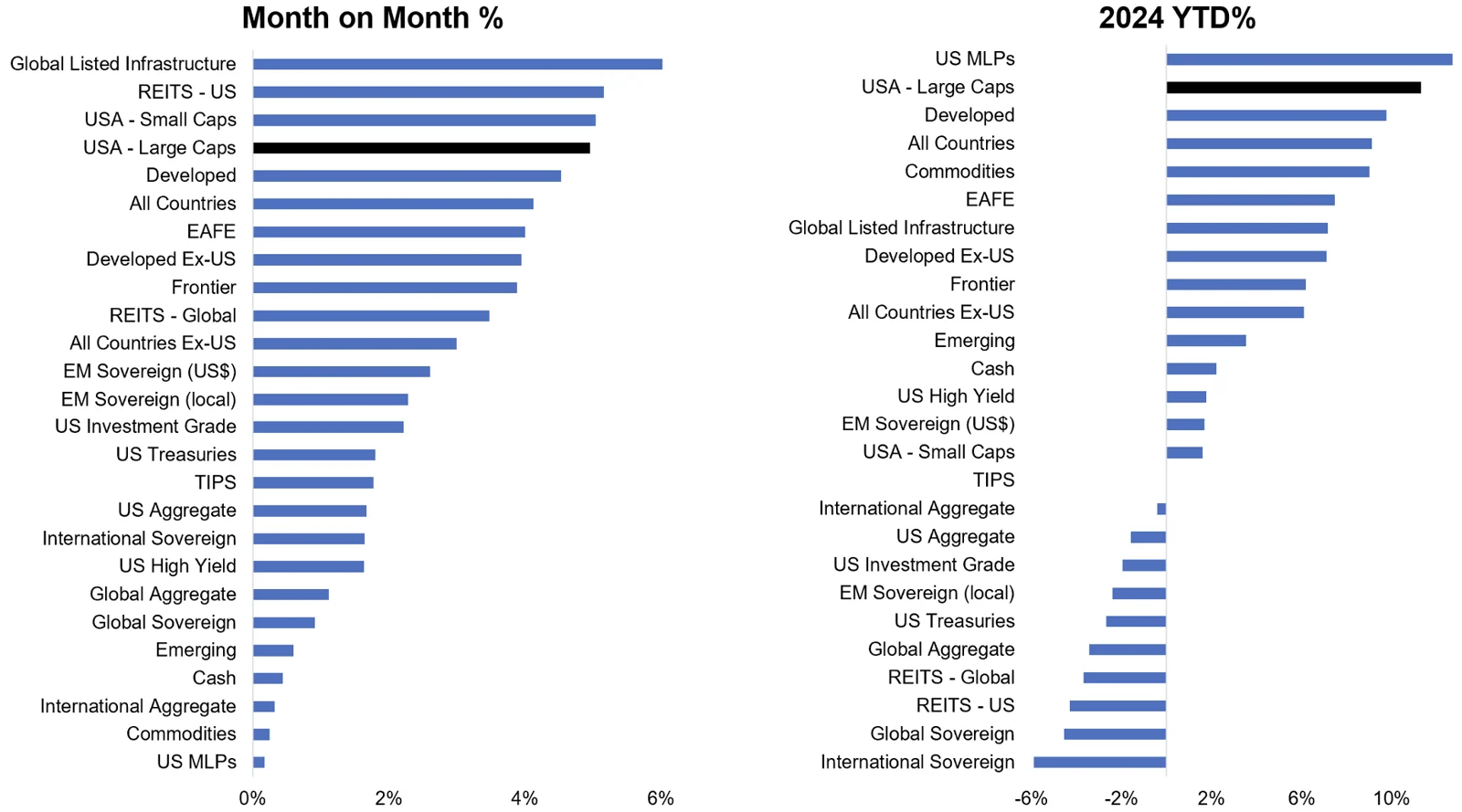

The chart below portrays the performance of global asset class returns in May and Year-to-Date.

A few takeaways: the bull market in stocks in 2024 – while certainly led by the U.S. – has been global in nature. Commodities, despite the relatively flat performance in oil prices this year, have generated close to double digit returns through the end of May, nearly matching the performance of stocks. This is somewhat surprising as commodities and financial assets have been negatively correlated to one another historically.

Also surprising is the very positive performance of stocks compared to the YTD negative returns seen in the global fixed income complex and REIT surrogates. Financial theory posits an increase in interest rates should translate into lower stock valuations as future earnings are discounted at a higher rate. While this is generally true, this year is proving to be an exception. A major reason may be bonds are still exiting a period of historically low rates, in some cases negative rates, where even small increases in nominal yields translate into a significant drop in prices.

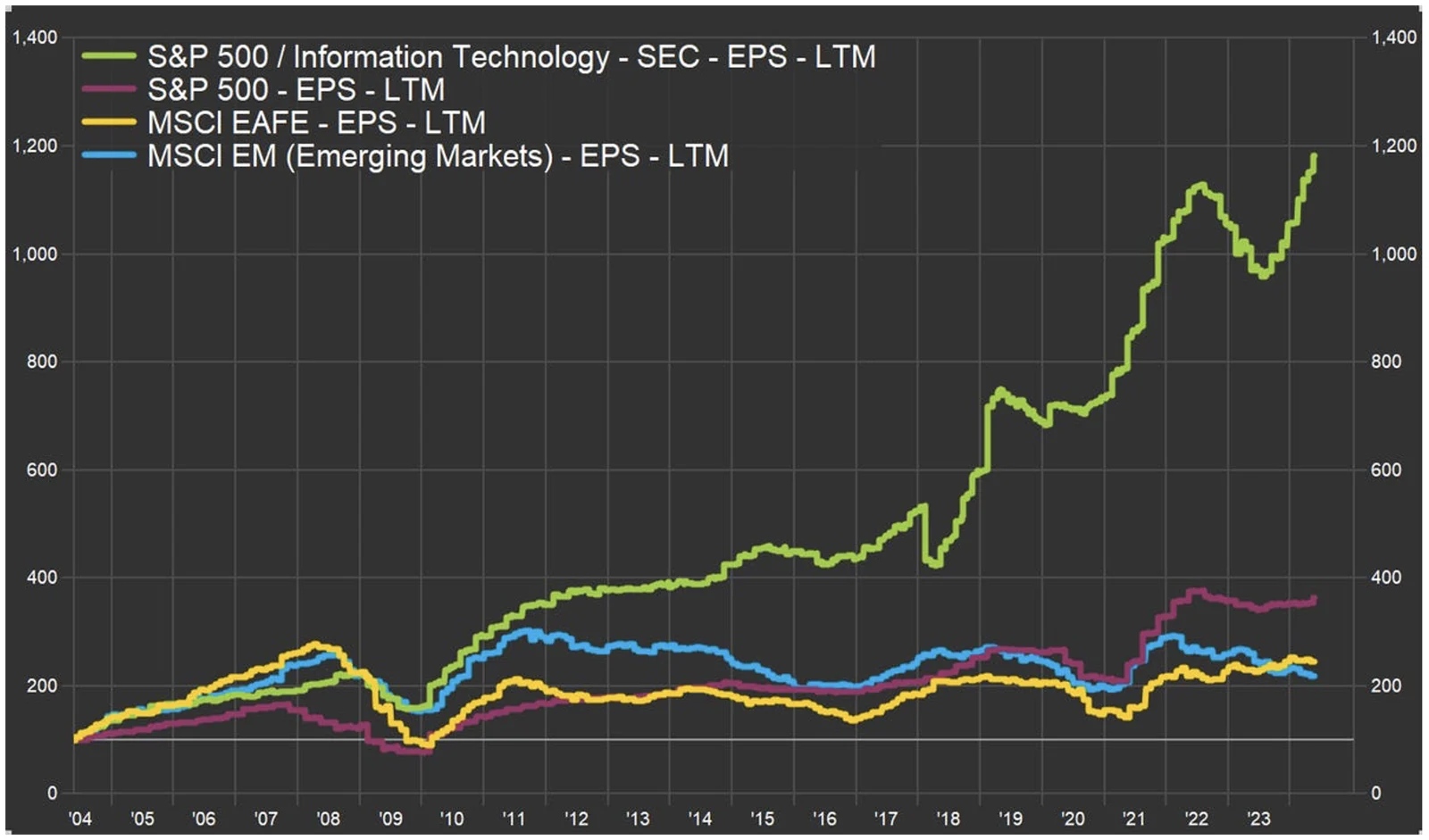

Another not surprising reason is the rise of AI and the accompanying hardware and software build out that have sent technology stocks skyrocketing. While many have suggested investor enthusiasm for the sector is bordering on mania, it’s important to note earnings of the IT sector have far outperformed those of broader indices here and abroad.

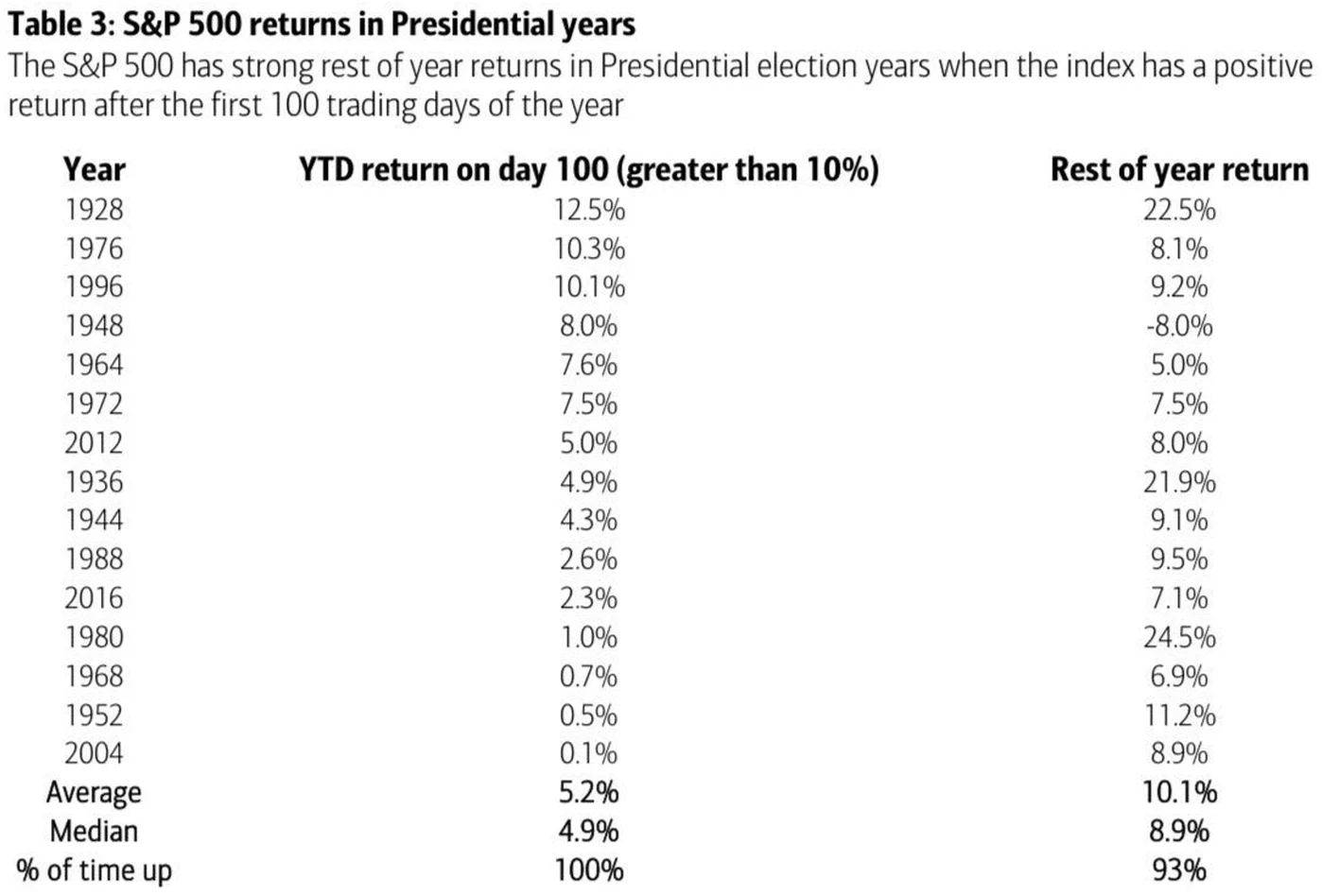

We have commented on the historically bullish performance of stocks in election years and 2024 is certainly following that playbook. Looking forward and taking into consideration the positive performance of stocks to date, the outlook for the remainder of the year – if history is our guide – is extremely bullish.

That said, we would be remiss if we didn’t point out the market advance is narrowing and weakness has set in across most sectors with the exception of technology and communications, and even there, the progress is concentrated in a few names. The Dow Jones Transportation Average has recently traded at a new low in 2024, an important development according to Dow Theory proponents as it signals a non-confirmation of the broader market uptrend. Further, indices abroad have weakened, with France being the most noticeable. The much anticipated broadening in stock participation, seen as the spur for further market gains going forward, may have to wait until Q2 2024 earnings reports are released.

fixed income

While the overall performance of bond markets in 2024 has been less than stellar, May was a positive month for the asset class. Duration sensitive securities benefitted the most, with the 30-Year U.S. Treasury gaining 2.83%, Bloomberg U.S. Corporate Investment Grade Bond Index up 1.87% and the 10-Year U.S. Treasury nearly the same (1.88%), and Bloomberg U.S. mortgage back securities advancing 2%. Bloomberg U.S. Corporate High-Yield bonds lagged but were still positive, up 1.1%.

Investors took heart from the relatively benign economic reports over the course of the month and in particular, budding evidence of weakness in the labor market. Although the non-farm payroll report showed job growth of 272,000 in May, far above what was forecast, the household employment survey (which is based on a smaller sampling) showed a significant decline. The Unemployment Rate has ticked up noticeably and now is clearly above its 12-month moving average and approaching their 36-month moving average. In the meantime, the National Federation of Independent Businesses survey of small business hiring plans has plummeted to levels not seen since the global pandemic. The Job Openings and Labor Turnover Survey (“JOLTS”) also shows job openings shrinking and workers less inclined to change jobs, both signs of decreasing confidence.

This is not to paint a gloomy picture of imminent recession. The economy continues to expand and the Atlanta Fed’s GDPNow forecast currently points to real growth of 3.1% in the second quarter (admittedly, the model’s results can bounce around quite a bit). Wage growth is healthy and as Chairman Powell pointed out, the pace of real final sales to private domestic purchasers – which eliminates the effect of changes in inventory, government spending and net exports – while moderating, grew at a solid pace, up 2.8% in the first quarter.

Federal Reserve and Monetary Policy

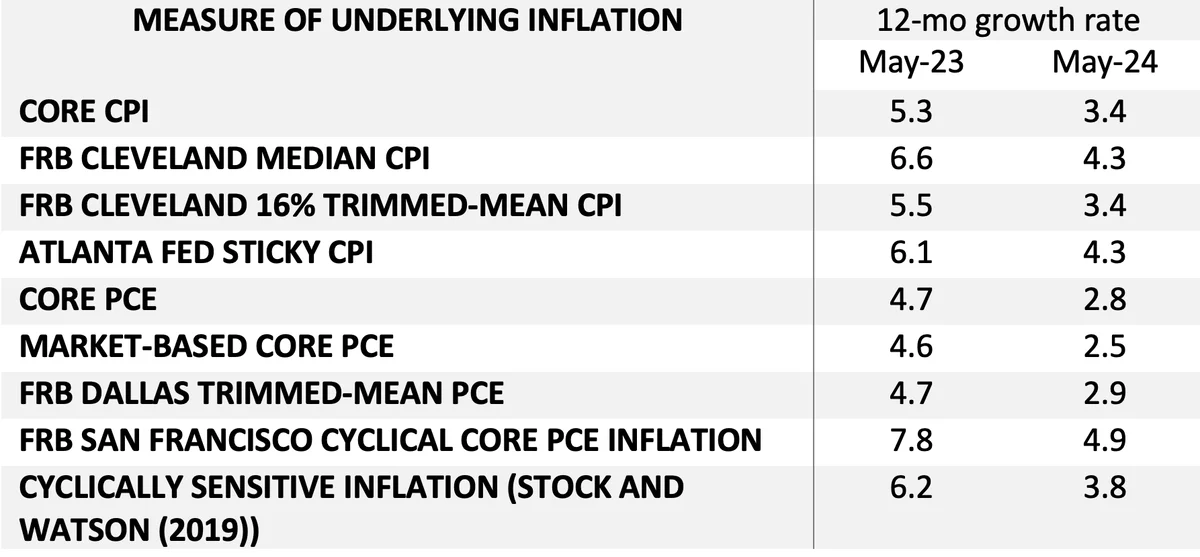

Chairman Powell’s game plan of holding rates steady while rolling back the speed of its balance sheet reduction is bearing fruit with inflation steadily falling and economic growth slowing but still in positive territory. The latest Atlanta Fed Underlying Inflation Dashboard shows the substantial progress the Fed has made in bringing inflation down nearer to its 2% long-term goal.

The Federal Reserve (“Fed”) has been aided by substantial growth in the labor supply over the past couple of years, even with an increasing number of baby boomers retiring. This has had the salutary effect of moderating wage growth coming out of the pandemic while boosting overall economic growth. The FOMC will want to see further progress on the wage front, as average hourly earnings month-over-month rose 0.4% in May and the employment cost index showed an increase of 1.2% in Q1 2024.

The Federal Reserve’s policy approach does hold one glaring contradiction centered around financial conditions. Chairman Powell in his recent press conferences has taken pains to reiterate the Fed’s monetary policy continues to be restrictive, implying aggregate demand will slow, eventually leading to cooling prices. The objective reality is financial conditions, as measured by the Chicago Fed National Financial Conditions Index and other comparable surveys, have been loose for years and it is the latter that most observers would agree drive markets. The San Francisco Fed explained the distinction in its Economic Letter of March 4, 2024 entitled Monetary Policy and Financial Conditions: “But focusing only on the short-term policy rate does not account for the broader financial conditions. After all, the effects of monetary policy on the economy also depend on long-term interest rates, corporate bond yields and lending rates, stock prices, exchange rates, and other asset prices. These factors, and not the policy rate alone, help determine financial market effects on economic activity.”

Extending this one step further because broader financial conditions have been so benevolent over time, it has produced a substantial wealth effect in the upper class who as a result, have continued to spend briskly even in the face of higher interest rates. The impact on those in the lower economic strata who have much less in investable savings has been quite the opposite and poses a quandary for the Fed on how best to slow the economy without unfairly burdening those less able to bear a restrictive rate policy.

Managed Income strategy – Manager Commentary

In early May, the Managed Income model moved back to a Risk-On posture, ending a three-week defensive period that began in mid-April. The signal change was attributed to a new uptrend established in U.S. High Yield, along with stabilization across equity market indicators and decreased market volatility.

Credit spreads remain near cycle lows, and in our view, the high yield sector is much more “expensive” than it was in November 2023 when the prior trade began. For this reason, the portfolio management team elected to increase its allocation to senior loan/floating rate to supplement the core high yield positions. Since the trade began in early May, these positions have outperformed the high yield sector. In the short term, we intend to continue relying on this segment of the portfolio to mitigate pricing volatility of the portfolio, while still providing a meaningful current yield.

Dynamic Growth strategy – Manager Commentary

Despite equity markets advancing in May, the Dynamic Growth model remained positioned in a Risk-Off posture for the entirety of the month, with the portfolio positioned entirely in cash equivalents. The exit trade was triggered based on rising volatility during the last week of April after six months of Dynamic Growth being fully invested.

During the first three weeks of May, the model was overweighting “countertrend” over “trend”; that is to say, assessing that the market was potentially overbought and due for a pullback to provide the opportunity to reenter. However, markets continued to inch upward. In the short term, we would expect to be buyers upon a sizable decline in equities as we enter a period of relatively stable seasonality for growth stocks. Conversely, should markets continue to surge ahead, we would expect the Dynamic Growth model to generate a Risk-On signal on continued strength. For now, however, the price action in equity markets has flattened out, suggesting a “wait and see” approach.

Active Advantage strategy – Manager commentary

In early May, the Active Advantage model moved into a fully Risk-On posture, with a balanced portfolio across fixed income and equities. For the fixed income component of the portfolio, floating rate/senior loan is the largest position. As noted above, we believe this segment of bonds provides a compelling risk/reward profile at this point in the cycle, providing some support and lower correlation to the equity portion of the portfolio with less correlation to equities than the high yield sector.

For the equity portion of the portfolio, Active Advantage holds a large core equity position, with smaller satellite positions in growth and high dividend equities. We will continue to monitor the markets, as well as the Active Advantage model outputs, to determine if any action is needed in the short term. For now, we believe the portfolio is well positioned in a balanced posture to provide current yield from the fixed income sector, while not taking on excess equity exposure.

Defender strategy – Manager Commentary

May proved to be a volatile month for global markets, characterized by mixed economic data, geopolitical tensions, and ongoing concerns over inflation and interest rate policies. The S&P 500 experienced fluctuations amid earnings reports, while international markets saw varied performances influenced by regional economic indicators and geopolitical developments.

The Defender Strategy navigated these turbulent waters with resilience. The strategy, known for its focus on defense, demonstrated stability during periods of market uncertainty. Asset class exposure to the Nasdaq and S&P 500 continued to show robust performance and remained resilient despite inflationary pressures, supported by strong consumer demand. However, geopolitical events, including tensions in Eastern Europe and shifts in global trade policies, influenced market sentiment throughout May and caused some volatility in the international exposures. Overall, the diversified asset positioning within the Defender Strategy helped shield investors from the full impact of these developments, highlighting the fund’s risk management capabilities.

Looking ahead, market participants anticipate continued volatility amid economic data releases and central bank communications. The Defender Strategy is positioned to benefit from its defensive and diversified stance, although market dynamics could shift based on evolving economic indicators and geopolitical developments.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular strategy such as the types of securities being substantially different.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Managed Income Strategy

Risks specific to the Managed Income Strategy include Management Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Non-Diversification Risk, Turnover Risk, U.S. Government Securities Risk, LIBOR Risk, Models and Data Risk.

Dynamic Growth Strategy

Risks specific to the Dynamic Growth Strategy include Management Risk, Equity Securities Risk, Market Risk, Underlying Funds Risk, Non- Diversification Risk, Small and Mid-Capitalization Companies Risk, Turnover Risk, U.S. Government Securities Risk, Models and Data Risk.

Active Advantage Strategy

Risks specific to the Active Advantage Strategy include Management Risk, Equity Securities Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Limited History of Operations Risk, Non-Diversification Risk, Small and Mid-Capitalization Companies Risk, Turnover Risk, U.S. Government Securities Risk, LIBOR Risk, Models and Data Risk.

Defender Strategy

Risks specific to the Defender Strategy are detailed in the prospectus and include general market risk, credit risk, interest rate risk, management risk, equity securities risk, fixed-income securities risk, high-yield bond risk, foreign investment risk, emerging markets risk, real estate and REITs risk, commodities risk, currency risk, subsidiary risk, market risk, underlying funds risk, derivatives risk, limited history of operations risk, turnover risk, models and data risk, momentum risk or risk of the portfolio not performing as expected.

Definition:

Bloomberg US Mortgage-Backed Securities (MBS): An unmanaged index that tracks fixed-rate agency mortgage-backed pass-through securities guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The index is constructed by grouping individual TBA-deliverable MBS pools into aggregates or generics based on program, coupon, and vintage.

Bloomberg US Aggregate Bond Index: An unmanaged index comprised of US Investment grade fixed rate bond market securities, including government agency, corporate and mortgage-backed securities. Investors cannot invest directly in an index. It is also known as US Aggregate Bond Index.

Bloomberg US Corporate Investment Grade Bond Index: An unmanaged index comprised of US investment grade fixed rate, taxable corporate bond market.

MSCI EAFE Index: An international equities market index that consists of large and mid-cap stocks across developed markets in Europe, Australasia, and Far East Asia. Excludes US and Canadian stocks.

MSCI Emerging Markets Index: An international equities market index that consists of large and mid-cap stocks across 24 emerging market countries that include but not limited to Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, South Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and United Arab Emirates.

NASDAQ 100: A market index that comprises of the 100 largest, most actively traded companies listed on the Nasdaq stock exchange.

S&P 500: A capitalization weighted index of 500 stocks representing all major domestic industry groups. The S&P 500 TR Index assumes the reinvestment of dividends and capital gains.

Russell 2000 Index: A market index that consists of 2,000 small-cap US companies that are part of the larger Russell 3000 Index.

Related Perspectives

View All-

Strategy Review – May 2025

February saw heightened volatility as investors reassessed the economic impact of newly imposed trade tariffs. While the market had initially assumed tariffs were a bargaining tactic, the confirmation of their implementation triggered a swift correction.

-

Kensington Monthly Commentary – May 2025

The stock market endured one of its most volatile months in years. The S&P 500 fell 21.35% from its February 19 peak of 6,147.43 before bottoming on April 7 at 4,835.04, shortly before the Administration announced a 90-day pause on new tariffs (excluding China). Markets quickly rebounded on the news, with the S&P 500 soaring 9.52% on April 9, its largest single-day gain since October 2008. The Nasdaq Composite jumped 12.16% the same day, marking its biggest one-day percentage gain since January 3, 2001, and the second-largest on record.