Kensington Monthly Commentary – May 2025

Monthly Market Commentary

By Kensington Asset Management Team

Stock Market

The stock market continued its robust rebound in May, fueled by positive developments in trade policy and legislative actions. The announcement of a 90-day pause in the US-China trade standoff and the House passage of a stimulative tax bill significantly boosted investor sentiment. The S&P 500 rose 6.15% (though the S&P 500 Equal Weighted lagged by 200 basis points), the Nasdaq 100 Index surged 9.04%, the Russell 2000 Index gained 5.20%, and the MSCI EAFE Index increased by 4.66%.

Investors welcomed the White House’s softened trade stance, particularly the substantial tariff reductions agreed with China, lowering US tariffs from 145% to 30%, and Chinese tariffs from 125% to 10%. Officials from both nations reached a framework deal in principle, awaiting final approval by President Trump and President Xi. Additionally, the White House postponed imposing a 50% tariff on EU countries from June 1st to July 8th, signaling ongoing negotiations and progress on complex trade issues like autos, digital taxes, and Value-Add Tax treatments.

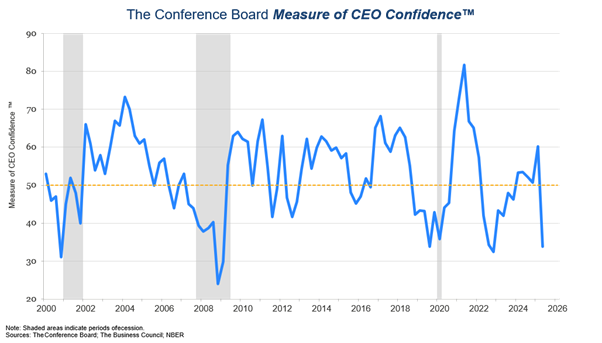

Aside from reduced trade tensions, robust economic news also supported the market rally. Despite strong first quarter corporate earnings growth of 13.3% among S&P 500 companies, forecasts for Q2 have moderated significantly, now projected at just 4.9%. Reflecting cautiousness, many CEOs avoided providing forward guidance. The Conference Board’s CEO Confidence Measure revealed a dramatic decline, plunging into pessimistic territory with over half of CEOs anticipating worsening economic conditions over the next six months.

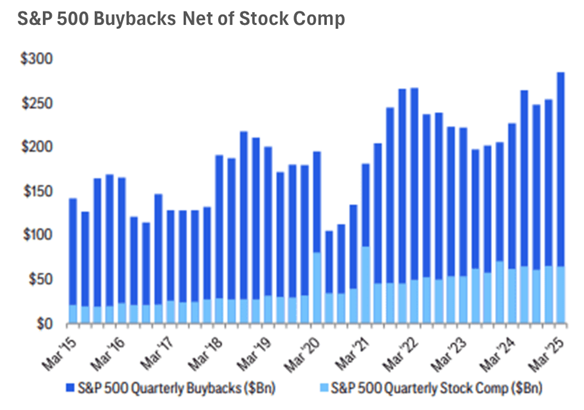

Nonetheless, investors largely shrugged off this pessimism, focusing instead on positive policy developments. With longer term capital decisions deferred, corporations directed significant cash flows into stock buybacks, achieving historic levels. Citi projects total share repurchases may approach $1 trillion in 2025, with April’s buybacks reaching the highest monthly total since 1984.

Source: Citigroup as of April 30, 2025

Fixed Income

Stronger than expected economic conditions posed headwinds for bond markets. The 30 year and 10 year Treasury bonds declined by -3.10% and -1.36%, respectively, while the Bloomberg US Mortgage Backed Securities Index fell -0.91%. the Bloomberg US Corporate Investment Grade Index remained essentially flat, whereas the Bloomberg US Corporate High Yield Bond Index outperformed, rising 1.68%.

Bond markets contended with two significant uncertainties: ongoing tariff negotiations and long term fiscal deficits. With Republicans aiming for legislative approval by July, continued large scale government spending is anticipated, pressuring rates alongside inevitable price increases from tariffs.

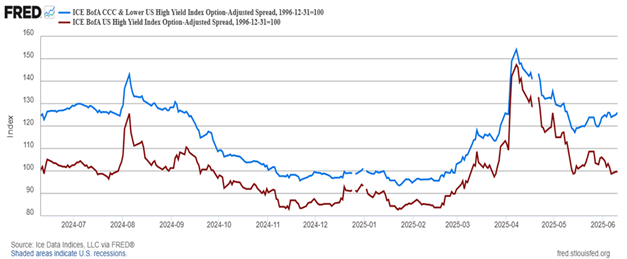

Corporate bond issuance rebounded, with May’s $209 billion marking an 85% increase over April. As proceeds frequently fund stock buybacks, issuance health remains a critical market indicator. However, caution is warranted regarding spreads on CCC[1] rated debt, which have begun widening relative to the broader high yield category, signaling potential future stress.

Liquidity considerations are also vital, notably the US Treasury’s cash balance management. Following tariff related disturbances in April, the Treasury allowed its balance to drop significantly, temporarily boosting market liquidity. However, projections indicate a sharp cash balance rebuild to around $850 billion by the end of June. This adjustment coincides with substantial corporate bond maturities anticipated later this year, the so-called corporate debt wall, raising refinancing pressures and highlighting liquidity as a key watchpoint.

Federal Reserve and Monetary Policy

The Federal Reserve has consistently rejected easing monetary policy, a stance supported by recent economic resilience. The Atlanta Fed GDPNow estimate indicates Q2 GDP growth to be around 3.8%. Inflation remains moderate, meeting or undershooting consensus forecasts.

Despite geopolitical uncertainties, consumer spending has remained stable, supported by robust personal income growth. April’s personal income rose 0.8%, following similar strong gains in prior months, bolstered by wage increases, stable employment, and strong transfer payments. Personal spending, though modest, has stayed resilient, rising 0.2% in April and 0.7% in March.

However, economic soft spots are emerging. Initial and continuing unemployment claims have increased slightly, and the Institute for Supply Management Services PMI recorded its first contraction in nearly a year, with new orders plunging to a three year low and input prices reaching multi year highs. Consumer debt repayment struggles are also rising.

Economic forecasts remain particularly uncertain pending outcomes of tariff negotiations and fiscal policies. JPMorgan CEO Jamie Dimon characterized the current environment succinctly, suggesting tariffs might moderate the economy’s trajectory without triggering significant downturns: “The tariffs are just hitting. It may just make the soft landing a little bit softer without making the ship go down.”

Overall, while markets remain buoyant due to policy developments and resilient economic indicators, uncertainties from tariff negotiations, fiscal policy implications, and rising credit stress warrant close monitoring in the months ahead.

[1]CCC credit rating from S&P 500 Global and Fitch indicates a borrower is highly vulnerable to default, though still meeting financial obligations. It reflects very high credit risk and is considered non-investment grade or junk statuse focus remains on monitoring inflation developments and economic resilience in the face of shifting trade dynamics.

Disclosures:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular strategy such as the types of securities being substantially different.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Definitions:

Bloomberg US Corporate Investment Grade Index: An unmanaged index that covers the publicly issued US corporate and specified foreign debentures and secured notes that meet the specified maturity, liquidity, and quality requirements. To qualify, bonds must be SEC-registered.

Bloomberg US Corporate High Yield Index: An unmanaged market value-weighted index that covers the universe of fixed-rate, non-investment grade debt in the US. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

Bloomberg US Mortgage-Backed Securities (MBS) Index: An unmanaged index that tracks fixed-rate agency mortgage-backed pass-through securities guaranteed by Ginnie Mae (GNMA), Fannie Ma

NASDAQ 100 Index: A market index that comprises of the 100 largest, most actively traded companies listed on the Nasdaq stock exchange.

Russell 2000 Index: A market index that consists of 2,000 small-cap US companies that are part of the larger Russell 3000 Index.

S&P 500: A capitalization weighted index of 500 stocks representing all major domestic industry groups. The S&P 500 TR Index assumes the reinvestment of dividends and capital gains.

S&P 500 Equal Weight Index: Equal weight to each of the 500 companies in the S&P 500, ensuring that each company has the same impact on the index’s performance, regardless of its market capitalization

KAM20250611A

Related Perspectives

View All-

Strategy Review – May 2026

March was shaped by a sharp escalation in US-Iran tensions, a surge in energy prices, and renewed concern that inflation could stay stickier than expected. The Federal Reserve again held rates steady, while higher oil prices and rising yields pressured traditional risk assets.

-

Monthly Market Commentary – May 2026

US equities moved lower in March as the conflict involving Iran, the US, and Israel pushed energy prices sharply higher and added another layer of uncertainty to an already fragile market backdrop. After