2024 In Review

Monthly Market Commentary

By Kensington Asset Management Team

Geopolitics:

The year 2025 is notable for being a perfect square year, meaning it is the product of a squared integer, in this case, 45. It is also the year of the Wood Snake according to the Chinese Zodiac. The Snake is associated with intuition, strategic thinking, intellect, intensity and transformation, like that of the phoenix rising from the ashes. The new international order that seems to be unfolding may warrant global leaders who can call upon these resources. We are a couple weeks into the new calendar year, and already the leader of one major country, Canada’s Justin Trudeau, has stepped down, President-elect Trump is threatening the takeover of Greenland and the Panama Canal, and the recent events in the Middle East suggest a profound change in its geopolitical landscape. All are indicative of a world in flux where national interest and self-reliance will be the watchwords in the coming year.

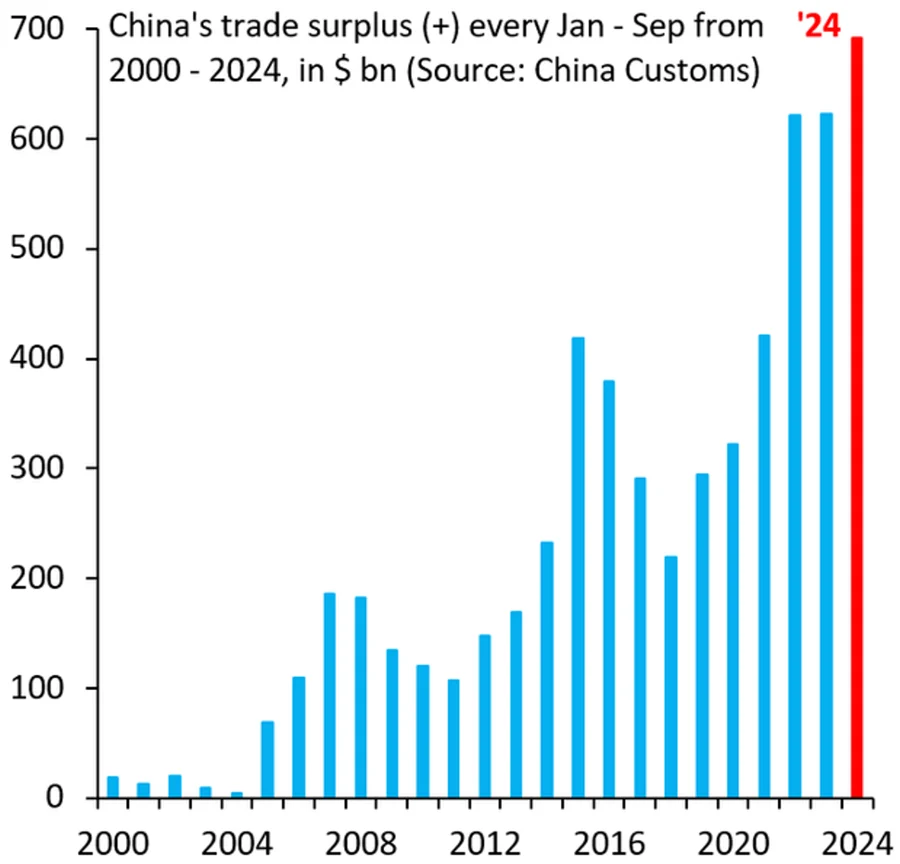

In terms of geopolitical risk, how the US and China manage their bilateral relationship continues to take center stage. The two countries will have to find a way to work together to roll back the huge trade surplus China has enjoyed for several years. China’s role as the “manufacturer of the world” has benefitted both to a point, but a major reset is needed.

Peacefully rebalancing trade between the two countries won’t be easy and is, to a great degree, a problem of China’s own making. It has been clear for years that the country’s excessive malinvestment in real estate would eventually bring unwanted consequences and require painful adjustment. Instead, authorities chose to delay the necessary painful steps to write off debt and rebalance the economy. Now at a time when the rest of the developed world no longer wants to increase their consumption of exports from China, the country faces a debt deflation and a domestic populace hesitant to spend. It remains to be seen whether President Xi and the Political Bureau will take the bold fiscal action required to stimulate the economy and reignite animal spirits there. There have been several sputtering attempts to do so but the country’s debt markets are loudly announcing they’re insufficient. China will have to look within for more of the answers to its economic problems.

Stock Market:

2024 marked the second consecutive year of 20%+ returns for the S&P 500, with the Index appreciating 23.31%. The stellar performance was driven by the so-called “Magnificent 7” stocks, which rocketed 65.22% higher in the year. By contrast, the S&P 500 Equal-Weighted Index lost -6.44% in December, and gained a relatively paltry 10.9% for the year. The Magnificent 7’s performance was reflected in the outperformance of the Nasdaq 100 Index as well, which was up 24.88%. The Russell 2000 Small Cap Index advanced 10.02% in 2024, in line with foreign indices where the MSCI EAFE Index was up 11.28% and the MSCI Emerging Markets Index a positive 13.12%. Given the disparity in performance among sectors and capitalization, it’s little wonder fund managers not focused on large-cap growth, and in particular tech and telecom, greatly trailed the indices most well-known to the public.

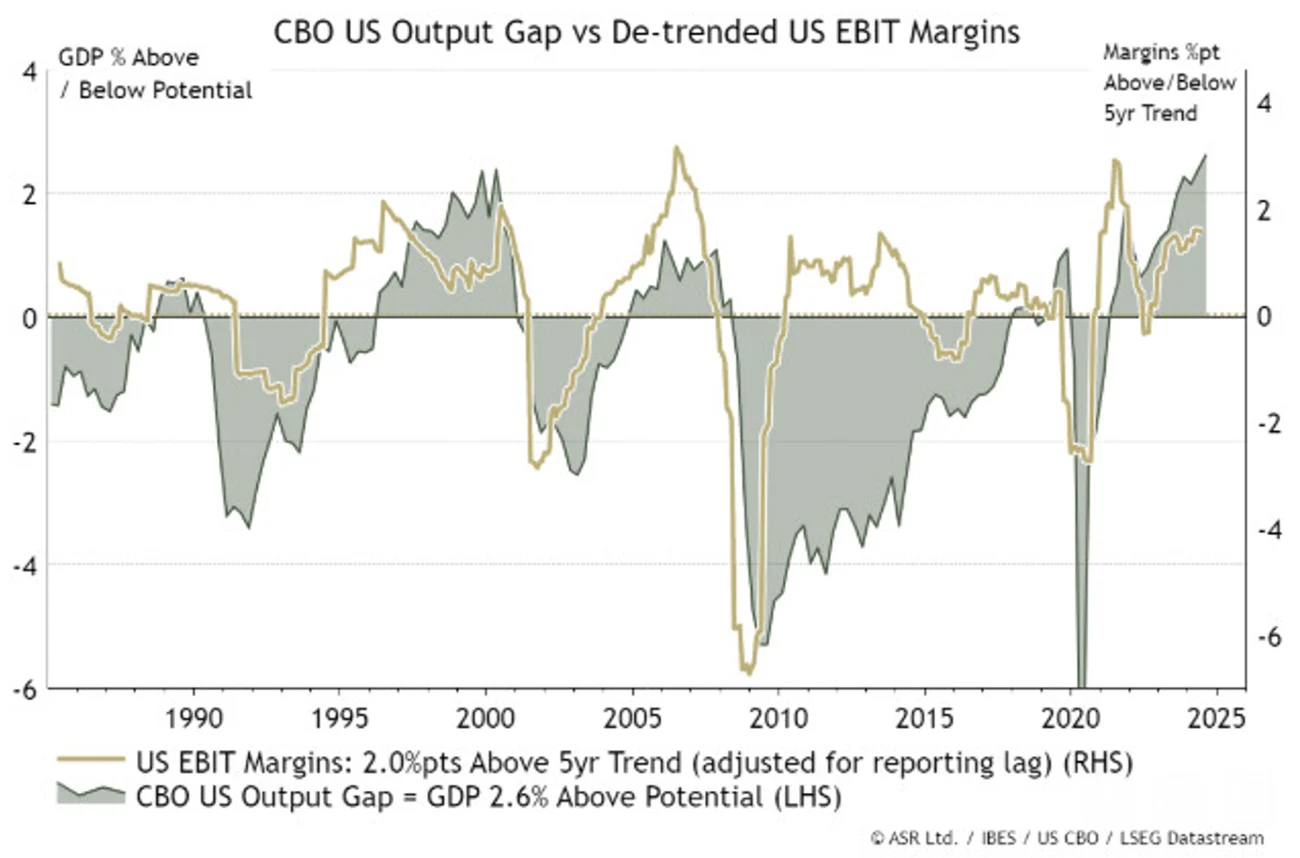

It’s glaringly obvious, by a cursory review of those same indices’ valuations, how elevated investor expectations are for 2025. FactSet’s highly regarded market analyst, John Butters, recently wrote that the market anticipates a year-over-year increase of 14.8% in the S&P 500, driven by a 5% increase in sales. Investors will want to take note that this growth rate far exceeds the trailing 10-year average (annual) growth rate of 8.0% (2014 – 2023). The earnings forecast assumes an estimated net profit margin of 13.0%, itself also meaningfully above the 10-year average (annual) net profit margin of 10.8%. In fact, if achieved, margins would be the highest since FactSet began tracking the metric in 2008.

A Financial Times article took a closer look at profit margins and pointed out that, not surprisingly, they are extremely sensitive to the overall strength of the economy (see below).

Given the new administration is expected to maintain a pro-stimulus economic policy, one might feel comfortable betting margins will be maintained and even increase, as earnings estimates imply. However, the combination of tariffs, deportation of illegal immigrants currently working and adding to GDP, plus the possibility of substantial cutbacks in public sector employees suggest a high degree of uncertainty around such a wager.

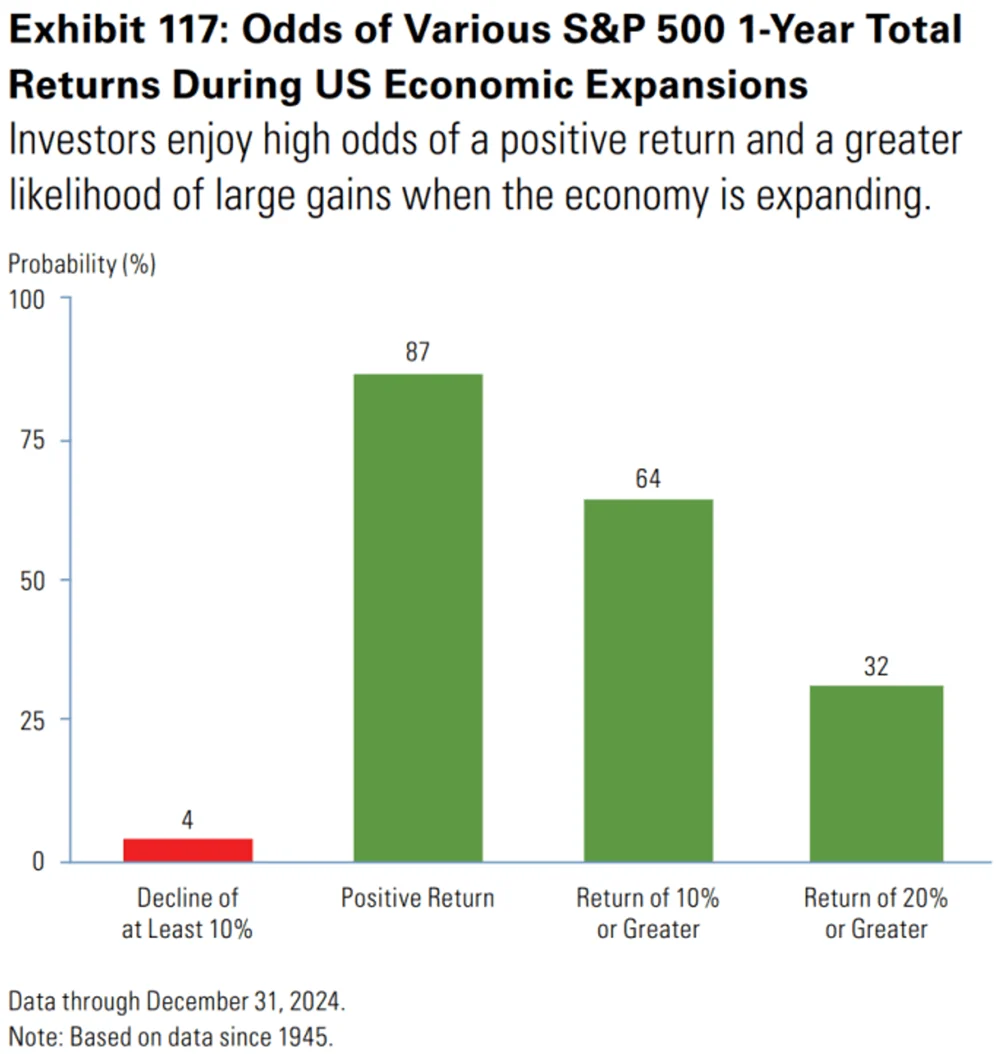

One final note – Goldman Sachs’ investment strategy group points out the US stock market, measured by the S&P 500, tends to deliver gains during economic expansions (see graph). With more fiscal stimulus to come and a populist President in office, a recession appears unlikely barring both a cyclical slowdown (not yet evident) and an external shock (although several of Trump’s proposals may well qualify – it remains to be seen).

Fixed Income:

Bonds finished another mediocre year, with the exception of lower quality credit, as longer-term rates moved measurably higher. The benchmark S&P US Treasury Bond Current 10Y Index fell -1.67%, the more duration sensitive S&P US 30Y Treasury Index lost an eye-opening -8.13%, while the S&P US Current 2Y Treasury Note Index appreciated 3.84%. The curve’s bear steepening over the course of the year rewarded managers for staying short their duration benchmarks. Shifting to credit, the Bloomberg US Corporate High Yield Index once again led the pack in 2024, gaining 8.19% while Bloomberg US Investment Grade Bonds Index advanced 2.13% and Bloomberg US MBS Index 1.20%.

Credit spreads remained extremely well behaved in 2024, narrowing to their smallest in many years. This has been a function of a few factors: one, the US economy continues to exhibit strength, many corporate issuers have long since termed out their debt such that new supply is meeting overwhelming demand, and fiscal spending has been a positive support of private sector demand while simultaneously exerting upward pressure on Treasury yields.

This backdrop suggests any future corrections across asset classes may be driven not by problems in a weakening credit environment – as is customarily the case – but more by upset in sovereign debt markets such as what occurred in the U.K. during Prime Minister Truss’ short-lived reign. A bear market in stocks may well start in Treasuries before translating into a slowdown in the private sector and credit markets. Low grade credit may not play its traditional role as an early warning signal.

One can easily imagine the sheer magnitude of Treasury issuance in the months and years ahead will require the Fed to soak up excess supply, effectively forcing it to embark on yield curve control. Under such a scenario, interest rates will be set at a level that allows corporate America to refinance the large amount of debt coming due, while placing less emphasis on overall inflation levels. The result may not be a debt-driven deflationary contraction but rather an economy growing in nominal terms with sluggish growth if not outright decline in real terms, such as occurred in the 1970s. Such a stagflationary environment has historically been a negative one for financial assets.

Federal Reserve and Monetary Policy:

The FOMC dropped the Fed Funds rate by 25 basis points at its December meeting with Powell, adopting a more cautious tone in regards to further rate decreases in 2025. Investors were caught a bit flat-footed by the Fed’s more conservative outlook and financial markets sold off in response.

The Fed finds itself subject to criticism from both sides of the interest rate argument. Those who believe the economy is weaker than economic reports indicate urge Powell not to waver in the Fed’s plan to lower rates. Meanwhile, rate hawks point to sticky inflation, still buoyant labor markets and quite loose financial conditions as reasons to reject further easing.

For now, the market’s verdict is that the Fed was overly dovish, too optimistic in expecting inflation to soon reach its 2% target. In response, the bond market has largely reversed what the Fed set out to do in September, with the 10-Year Treasury yield having shot up by more than 100 basis points. The Fed next meets in late January and will have a plethora of data to contend with: by then members will likely have a greater sense of the new Administration’s economic program. In addition, recent employment reports have indicated the recent softening in labor markets has slowed, while at the same time progress in inflation has stalled. Perhaps more alarmingly, consumers’ outlook for inflation over the next five years jumped to 3.3% this month, the highest since June 2008. Mix in the short and long-term economic impact of perhaps the most expensive fire in US history, and it can be expected the Fed will proceed even more cautiously than normal.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular strategy such as the types of securities being substantially different.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Definitions:

Bloomberg US Corporate Investment Grade Bond Index: An unmanaged index comprised of US investment grade fixed rate, taxable corporate bond market.

Bloomberg US Corporate High Yield Index: An unmanaged market value-weighted index that covers the universe of fixed-rate, non-investment grade debt in the US. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

Bloomberg US Mortgage-Backed Securities (MBS) Index: An unmanaged index that tracks fixed-rate agency mortgage-backed pass-through securities guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The index is constructed by grouping individual TBA-deliverable MBS pools into aggregates or generics based on program, coupon, and vintage.

MSCI EAFE Index: An international equities market index that consists of large and mid-cap stocks across developed markets in Europe, Australasia, and Far East Asia. Excludes US and Canadian equities.

MSCI Emerging Markets Index: An international equities market index that consists of large and mid-cap stocks across 24 emerging market countries that include but not limited to Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, South Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and United Arab Emirates.

NASDAQ 100 Index: A market index that comprises of the one hundred largest, most actively traded companies listed on the Nasdaq stock exchange.

Russell 2000 Small Cap Index: A market index that consists of 2,000 small-cap US companies that are part of the larger Russell 3000 Index.

S&P 500: A capitalization weighted index of 500 stocks representing all major domestic industry groups. The S&P 500 TR Index assumes the reinvestment of dividends and capital gains.

S&P 500 Equal Weight Index: Equal weight to each of the 500 companies in the S&P 500, ensuring that each company has the same impact on the index’s performance, regardless of its market capitalization

S&P US 30Y Treasury Index: Tracks the performance of US Treasury bonds with maturities of 30 years. It reflects the long-term interest rate environment and is used by investors to gauge the performance of long-term government debt.

S&P US Treasury Bond Current 10Y Index: The S&P US Treasury Bond Current 10-Year Index is a one-security index comprising the most recently issued 10-year US Treasury note or bond.

S&P US Treasury Bond Current 2Y Index: A one-security index that tracks the most recently issued 2-year US Treasury note or bond1. This index provides a benchmark for the performance of short-term US government debt

Related Perspectives

View All-

Monthly Market Commentary – April 2026

US equities moved lower in March as the conflict involving Iran, the US, and Israel pushed energy prices sharply higher and added another layer of uncertainty to an already fragile market backdrop. After

-

Strategy Review – April 2026

March was shaped by a sharp escalation in US-Iran tensions, a surge in energy prices, and renewed concern that inflation could stay stickier than expected. The Federal Reserve again held rates steady, while higher oil prices and rising yields pressured traditional risk assets.