A Breadth of Fresh Air

Market Insights

Brian Weisenberger, CFA, Senior Market Strategist

Market Insights is a piece in which Kensington’s Portfolio Management team will share interesting and thought-provoking charts that we believe provide insight into markets and the current investment landscape.

Improving Breadth as Q2 Earnings Approach

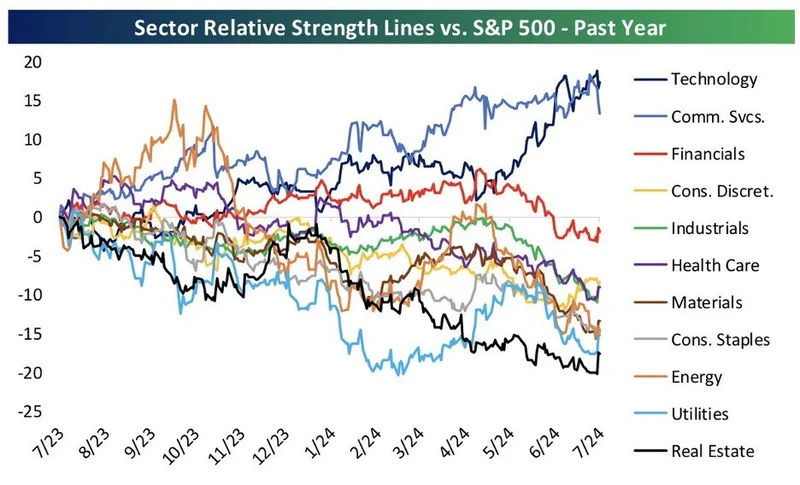

The first half of 2024 for U.S. equity markets, particularly large caps, has been defined by advancing indices with very limited breadth. Of the 11 sectors that make up the S&P 500, only two have outperformed the index over the past year (chart below): Technology and Communication Services (which is technology-heavy). While markets have benefitted from these sectors’ strong performance, it has also created significant concentration, leaving markets vulnerable should tech underperform.

Small Caps on the Rise

However, with last week’s better-than-expected CPI inflation report, a potential shift has taken place as the more interest rate-sensitive small-cap sector has started to take off. Last week, the small-cap index, the Russell 2000, advanced by 6%, outperforming the S&P 500 for the week by the largest such margin since April 2020. Encouragingly, the trend has continued into this week, with the index rising an astounding 10.3% in five trading days (through July 15th), compared to just 1.08% for the S&P 500 over the same period (chart below).

A Breadth of Fresh Air

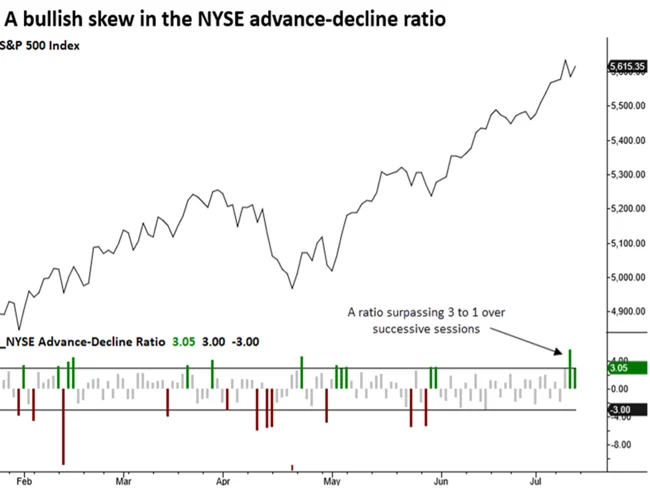

The shift is not just confined to small caps. In the first half of 2024, the S&P 500 had been buoyed by the performance of a small number of stocks. In fact, the top 10 biggest stocks in the S&P 500 contributed to 77% of the index’s total return through June. However, the recent surge in small caps has also coincided with a rotation within the S&P 500. For only the 26th time since 1936, advancing issues on the NYSE outpaced declining issues by a ratio of 3 to 1 over successive trading sessions last week (chart below), expanding breadth within the S&P 500 to its strongest reading since April.

Q2 Earnings on Deck

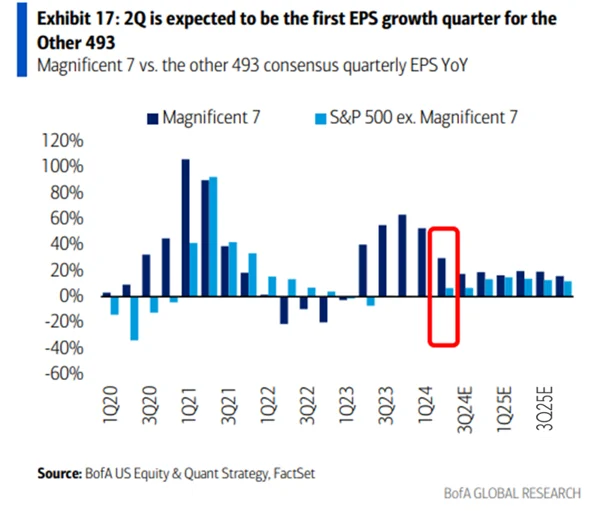

While all of this is potentially a positive indicator for market strength going forward, this recent push has been predicated on optimism for Fed rate cuts in September (a long way away) and will likely need to be supported by improved Q2 earnings if it is to continue. Outside of the Magnificent 7, S&P 500 earnings have been flat to down for the past five quarters, justifying their underperformance over the past two years. Q2 is expected to mark the first growth quarter for the “Other 493” since Q4 2022 (chart below).

This improvement would come at a good time as earnings expectations for AI stocks, which have carried the market for a year and a half, are expected to decline going forward (chart below). A rise in earnings for non-AI-related companies is a best-case scenario for the bull market to continue.

Even with a significant rise in earnings for the “Other 493,” the bar is set fairly high for this earnings season. The S&P 500 is currently projected to show 8.8% year-over-year growth in EPS for Q2 (chart below), a meaningful rise from previous quarters, and even if accurate, it may not be enough to support further growth.

According to DataTrek Research, “The magic number for Q2 earnings season is a 6.6% earnings beat versus expectations. Given that U.S. large caps are near record highs, this is the bare minimum necessary to keep equity valuations at current levels.” While this number is certainly achievable (the average earnings surprise beat since 2019 is 8.6%) (chart below), given the higher earnings expectations this quarter, it is certainly not a given.

Conclusion

As we look ahead, it’s clear that while the recent market performance is encouraging, the upcoming Q2 earnings will be a critical determinant of how the second half of 2024 unfolds for U.S. equities. The improving (but still limited) breadth of market participation, driven by a few key sectors, underscores the necessity of robust earnings across a wider array of companies to sustain momentum. Given the current landscape of higher valuations, it is essential for investors to remain nimble and vigilant in order to capitalize on opportunities while managing risks effectively.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Related Perspectives

View All-

KHPI’s Fiscal Year 2025 Review and the Power of Net-of-Tax Performance

KHPI’s Fiscal Year 2025 Review and the Power of Net-of-Tax Performance Monthly Market Commentary By Kensington Asset Management Team The following is for informational purposes only and not construed as tax advice. Please consult with a tax professional for your specific situation. For the modern fiduciary, performance is a multi-dimensional metric. While investment returns capture […]

-

KENSINGTON SPOTLIGHT SERIES: THE DEFENDER STRATEGY

At Kensington Asset Management, we’ve actively managed fixed income solutions for clients for over three decades. Throughout this journey, we’ve weathered all types of macroeconomic regimes from extreme market volatility events to periods of steady growth.