Adapting to Rate Cuts

Market Insights

Brian Weisenberger, CFA, Senior Market Strategist

Market Insights is a piece in which Kensington’s Portfolio Management team will share interesting and thought-provoking charts that we believe provide insight into markets and the current investment landscape.

Rate Cuts Incoming

Last week at the Jackson Hole Economic Symposium, Federal Reserve Chairman Powell seemingly confirmed a September rate cut, indicating, “The time has come for policy to adjust.” Notably, his focus was not on improving inflationary data. Instead, he highlighted, “The cooling in labor market conditions is unmistakable,” marking a shift in the Fed’s primary focus within their dual mandate of “pursuing the economic goals of maximum employment and price stability.” For the past two and a half years, the Fed has been on a mission to tame inflation (price stability), but it is now turning its attention to the labor market (maximum employment).

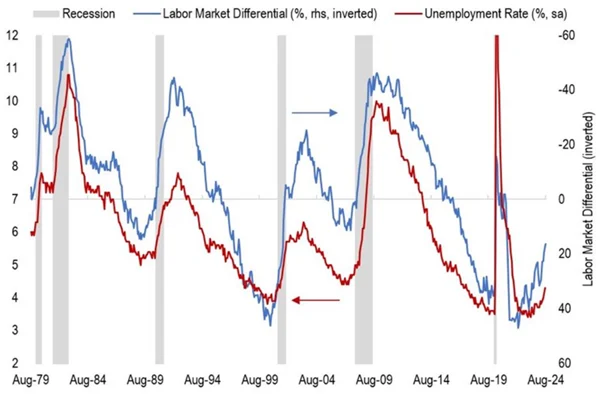

Earlier this week the Conference Board released their August US Consumer Confidence Report, which showed the Labor Market Differential—the difference between respondents citing jobs as “hard to get” versus “plentiful”—saw another sharp rise (chart below). This measure has historically been a leading indicator for the unemployment rate…and recession.

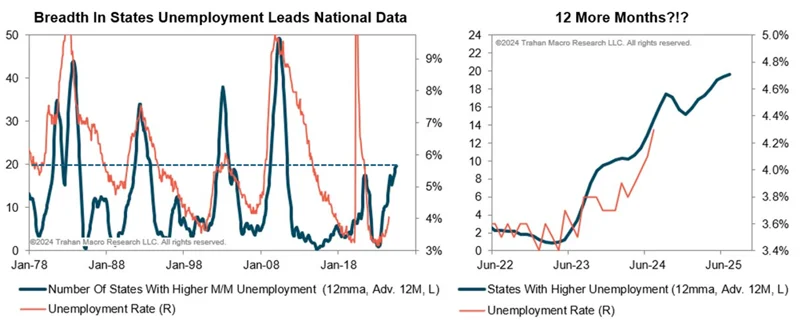

It’s important to note that even a relatively low unemployment rate does not necessarily safeguard against a recession. Since the late 1940s, half of historical recessions occurred when the unemployment rate was at or below the current level (4.3%), and in 8 of the last 12 recessions, it was at or below 5% (chart below).

Rate Cut Impact on Equities

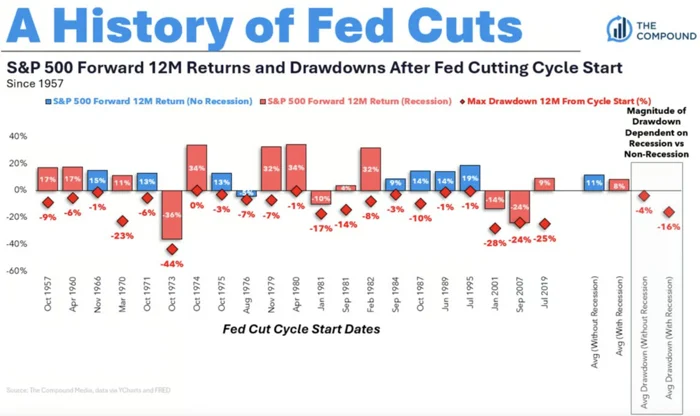

With a new rate cut cycle seemingly beginning in a few weeks, investors must now evaluate how to position their portfolios in response. If history is any guide, equity markets are likely to benefit from cuts. Since 1957, the 12-month forward return from the first rate cut for the S&P 500 has shown the index up 82% of the time (18 out of 22 instances), regardless of a recession (chart below). While returns are better if a recession is avoided (average return: 11%), they remain positive on average even if a recession occurs (average return: 8%). What a recession does impact is the predictability of equity returns. Historically, each of the negative 12-month forward returns occurred when a recession hit, with the average drawdown quadrupling from -4% in the absence of a recession to -16% during a recession. The maximum drawdown was -10% (1987) without a recession compared to -44% during a recession (1973).

Rate Cut Impact on Fixed Income

The impact on fixed income in a rate-cut environment might seem straightforward on the surface. The connection between interest rates and bond prices suggests that bonds should appreciate, with longer-duration bonds benefiting the most. However, it may not be that simple.

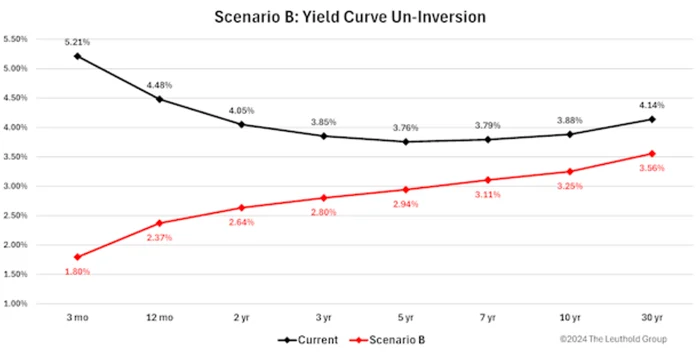

As Scott Opsal, Director of Research at The Leuthold Group, recently pointed out in a “Of Special Interest” report, “The simple approach of targeting longer durations is complicated by today’s inverted curve, meaning that lower rates will almost surely not manifest themselves through a parallel downward shift in the curve, but will be accompanied by an un-inversion that will return rates to an upward sloping shape. This twist in the curve’s slope will require investors to target the appropriate spot on the curve to optimize the interest rate effect on bond prices.”

Using a simple example (chart below), we could see the long end of the curve only moderately shift down, while shorter-duration issuances, which are historically more influenced by Fed rate policy, experience a more significant drop as the curve un-inverts.

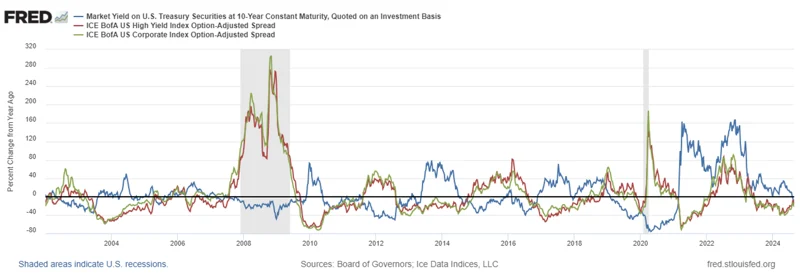

Mr. Opsal further notes that for corporate bonds, both investment-grade and high-yield, the interaction between interest rate moves and credit spreads (the difference in yield between corporates and Treasuries) is of significant importance. The relationship between the 10-year Treasury yield and corporate spreads (chart below) has demonstrated a significant inverse relationship, where higher rates have tended to result in lower spreads and vice versa. We have certainly seen spreads tighten during the rate-hiking cycle of these past two-plus years. If this relationship holds true, widening spreads could insulate or offset potential gains in corporate issuances.

Conclusion

While a forthcoming rate cut may offer some support to both equity and fixed income markets, the outcomes are far from certain. The variability in how stocks and bonds might respond—especially given the complexities of an inverted yield curve and shifting economic conditions—underscores the importance of remaining agile in your investment strategy. As the market navigates these uncertain waters, a nimble approach will be key to capitalizing on opportunities and mitigating risks.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Related Perspectives

View All-

KHPI’s Fiscal Year 2025 Review and the Power of Net-of-Tax Performance

KHPI’s Fiscal Year 2025 Review and the Power of Net-of-Tax Performance Monthly Market Commentary By Kensington Asset Management Team The following is for informational purposes only and not construed as tax advice. Please consult with a tax professional for your specific situation. For the modern fiduciary, performance is a multi-dimensional metric. While investment returns capture […]

-

KENSINGTON SPOTLIGHT SERIES: THE DEFENDER STRATEGY

At Kensington Asset Management, we’ve actively managed fixed income solutions for clients for over three decades. Throughout this journey, we’ve weathered all types of macroeconomic regimes from extreme market volatility events to periods of steady growth.