Margin Madness

Monthly Market Commentary

By Bruce DeLaurentis

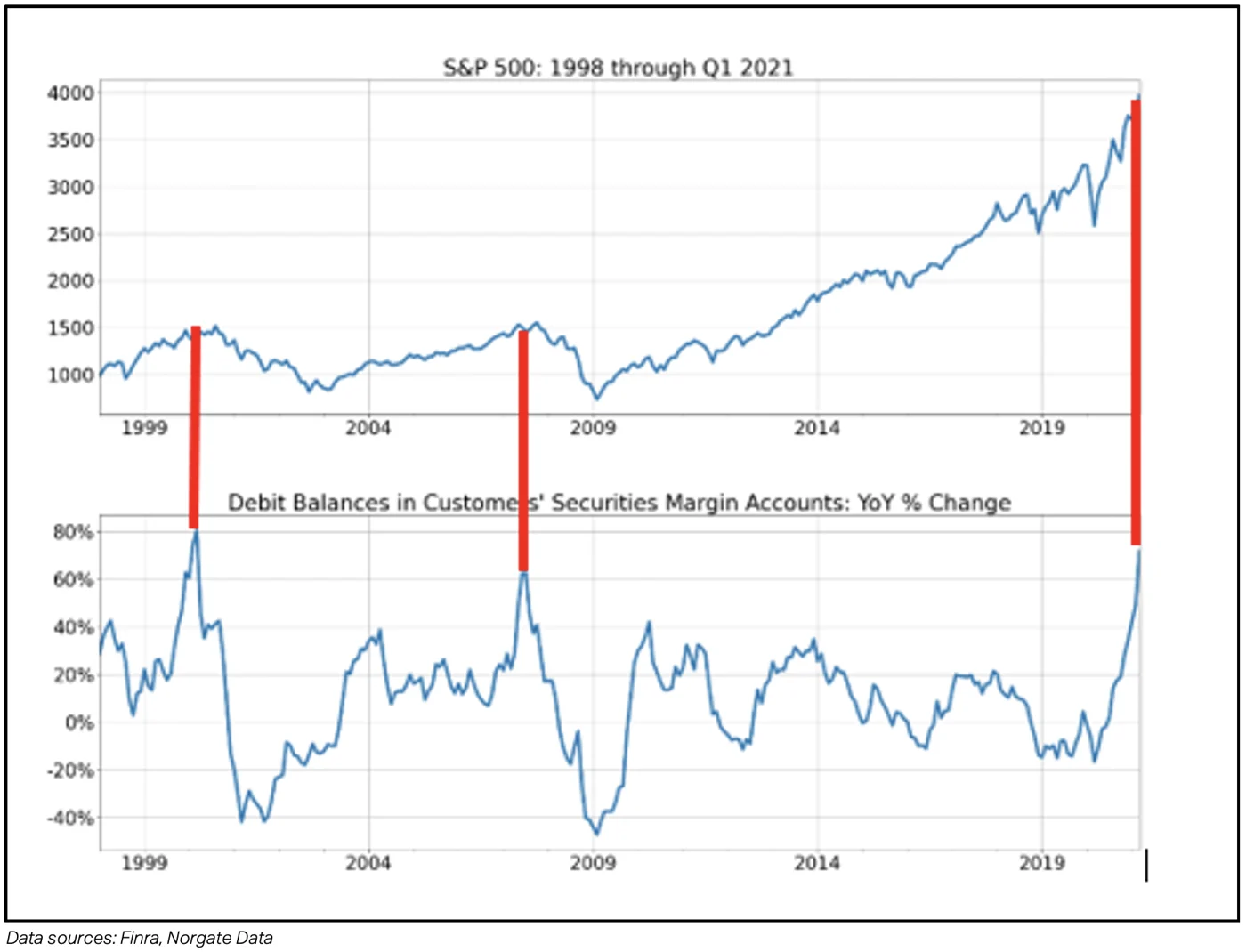

In last month’s commentary, we highlighted the seasonal adage, “Sell in May and go away.” Adding to our concern this month is a bearish signal from an important measure of investor sentiment: the recent surge in the growth of margin debit balances. Debit balances are the total amount of money owed by the customer to a broker or other lender for funds borrowed to purchase securities. Broad investor willingness to borrow money to buy securities is a sure sign of over optimism and a warning markets may be setting up for a correction.

Historically, an extreme (60%+) year-over-year change in margin debt is a rare occurrence, as illustrated by the chart below. Notice the red lines connecting the points in time when the year-over-year increase exceeded the 60% threshold. The prior two incidences preceded the last two major bear markets. The most current reading suggests it may again be time for a more defensive stance going forward.

The concern that investor sentiment may be reaching a bullish extreme is also supported by other anecdotal evidence: the growing trend of retail fondness for so-called “meme” stocks, cryptocurrencies, call options and other higher-risk offerings. Together with more fundamental reasons for caution in the form of rising interest rates and the possibility of major tax increases ahead suggests the need for a more tactical investment approach such as Kensington’s model-driven process, which has always sought to mitigate losses during significant market downturns.

Best regards,

Bruce P. DeLaurentis

Kensington Asset Management, LLC.

Related Perspectives

View All-

Monthly Market Commentary – July 2026

June’s central tension was that positive US economic data coincided with weakness in certain large-cap equities.

-

Strategy Review – June 2026

March was shaped by a sharp escalation in US-Iran tensions, a surge in energy prices, and renewed concern that inflation could stay stickier than expected. The Federal Reserve again held rates steady, while higher oil prices and rising yields pressured traditional risk assets.