Margin Madness

Monthly Market Commentary

By Bruce DeLaurentis

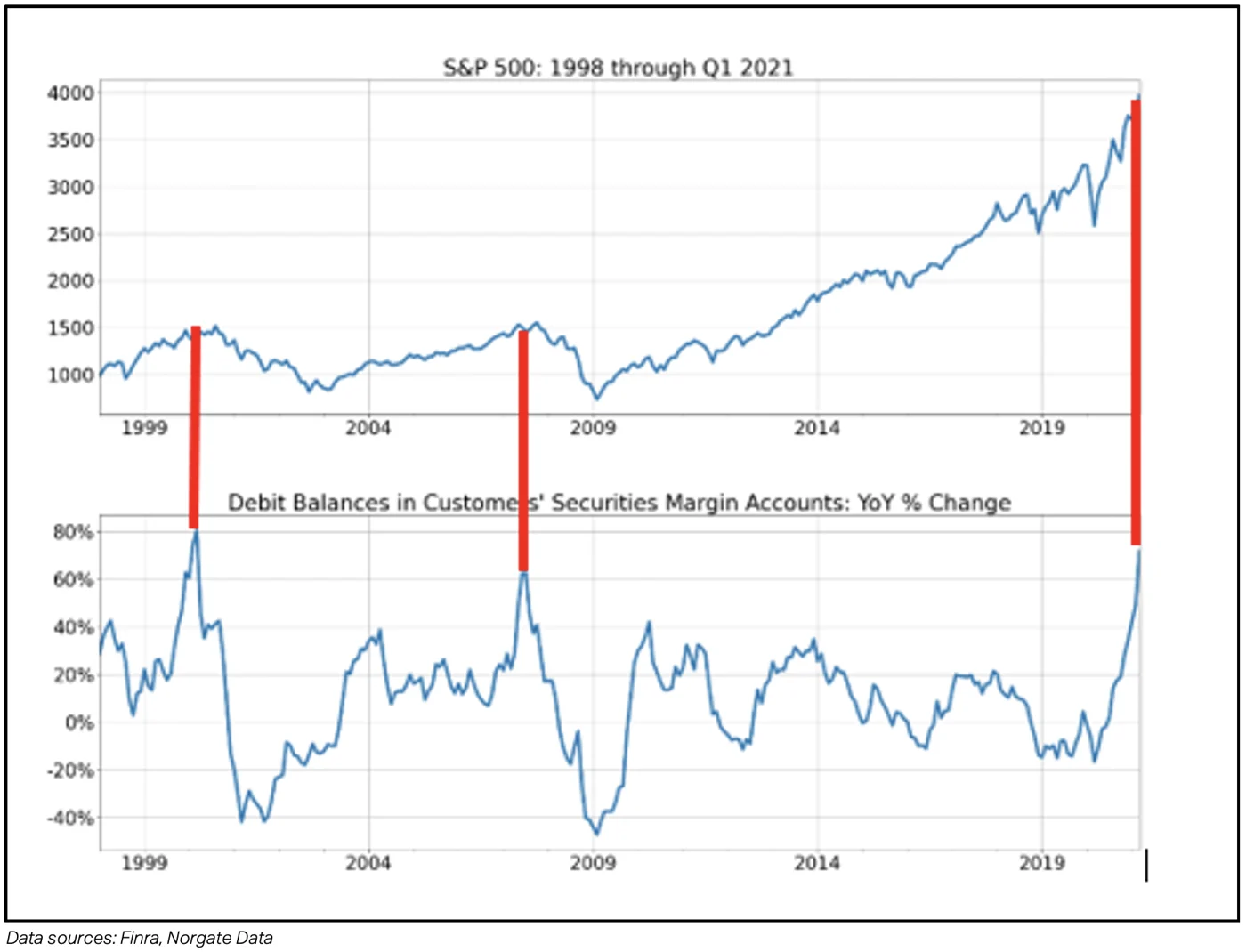

In last month’s commentary, we highlighted the seasonal adage, “Sell in May and go away.” Adding to our concern this month is a bearish signal from an important measure of investor sentiment: the recent surge in the growth of margin debit balances. Debit balances are the total amount of money owed by the customer to a broker or other lender for funds borrowed to purchase securities. Broad investor willingness to borrow money to buy securities is a sure sign of over optimism and a warning markets may be setting up for a correction.

Historically, an extreme (60%+) year-over-year change in margin debt is a rare occurrence, as illustrated by the chart below. Notice the red lines connecting the points in time when the year-over-year increase exceeded the 60% threshold. The prior two incidences preceded the last two major bear markets. The most current reading suggests it may again be time for a more defensive stance going forward.

The concern that investor sentiment may be reaching a bullish extreme is also supported by other anecdotal evidence: the growing trend of retail fondness for so-called “meme” stocks, cryptocurrencies, call options and other higher-risk offerings. Together with more fundamental reasons for caution in the form of rising interest rates and the possibility of major tax increases ahead suggests the need for a more tactical investment approach such as Kensington’s model-driven process, which has always sought to mitigate losses during significant market downturns.

Best regards,

Bruce P. DeLaurentis

Kensington Asset Management, LLC.

Related Perspectives

View All-

Strategy Review – May 2025

February saw heightened volatility as investors reassessed the economic impact of newly imposed trade tariffs. While the market had initially assumed tariffs were a bargaining tactic, the confirmation of their implementation triggered a swift correction.

-

Kensington Monthly Commentary – May 2025

The stock market endured one of its most volatile months in years. The S&P 500 fell 21.35% from its February 19 peak of 6,147.43 before bottoming on April 7 at 4,835.04, shortly before the Administration announced a 90-day pause on new tariffs (excluding China). Markets quickly rebounded on the news, with the S&P 500 soaring 9.52% on April 9, its largest single-day gain since October 2008. The Nasdaq Composite jumped 12.16% the same day, marking its biggest one-day percentage gain since January 3, 2001, and the second-largest on record.