Monthly Market Commentary – March 2026

(As of 03/31/2026)

Monthly Strategy Commentary

By Kensington Asset Management Team

Stock Market

US equities moved lower in March as the conflict involving Iran, the US, and Israel pushed energy prices sharply higher and added another layer of uncertainty to an already fragile market backdrop. After an initially muted reaction, equities weakened as investors began to price in a more prolonged disruption and the potential economic consequences of higher oil prices. By month-end, the S&P 500 had declined 5.09%, while the Nasdaq 100 fell 4.89% and the Russell 2000 lost 5.17%.

International markets generally fared worse, particularly in regions more exposed to imported energy costs. Japan and India were among the hardest hit, with the Nikkei 225 down 12.7% and the BSE Sensex down more than 11% during the month. Those moves illustrate how an oil shock can pressure growth expectations, especially in economies that rely heavily on imported energy.

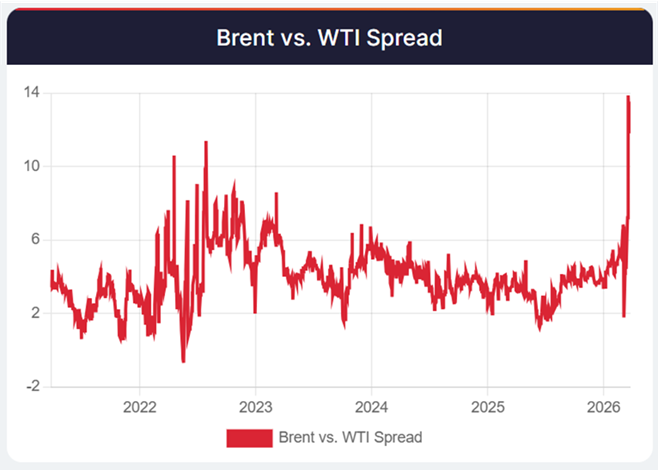

Oil was central to the market narrative. While both Brent and WTI moved sharply higher, Brent was the more important signal because it better reflected the supply disruption facing global markets. As the month progressed, the widening Brent-WTI spread highlighted the difference between global and domestic energy pricing pressure. At the peak of the move on March 31, that spread widened to $25 per barrel, highlighting the potential inflationary and economic considerations associated with higher global oil prices.

Source: RBN Energy LLC as of March 31, 2026

One of the more notable developments in March was that traditional safe havens did not provide as much support as investors might have expected. Gold and longer-duration Treasuries both came under pressure, suggesting that liquidity considerations and inflation concerns may have outweighed typical flight-to-safety dynamic. That is consistent with the broader view that global liquidity conditions have become less supportive, with tighter financial conditions, firmer oil prices, a stronger US dollar, and elevated bond volatility all acting as headwinds for risk assets.

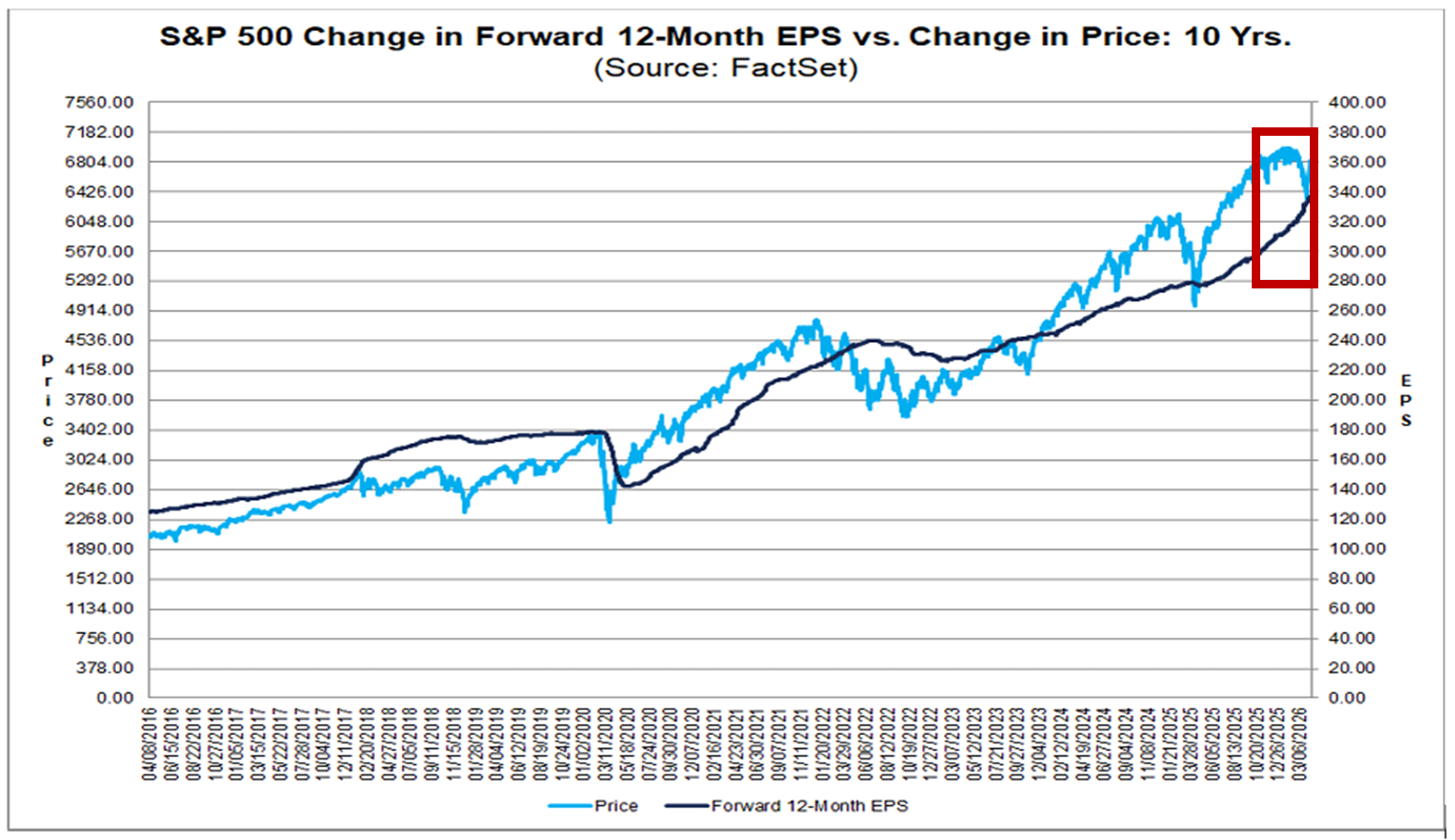

At the same time, the underlying earnings backdrop remained constructive. FactSet notes that first quarter earnings growth for the S&P 500 was tracking at 12.6%, which would mark a sixth consecutive quarter of double-digit year-over-year growth (4/10/26). Given the historical tendency for companies to outperform initial estimates, that figure could ultimately move higher. In our view, this earnings backdrop may help explain why equities showed sensitivity to late-month headlines suggesting a possible path to de-escalation. Even in a more volatile macro environment, earnings fundamentals for large-cap US companies have remained relatively resilient.

Source: FactSet as of April 10, 2026

Fixed Income

Fixed income markets also struggled in March as the rise in oil prices pushed inflation concerns back to the forefront. Treasuries posted negative returns across the curve, with the 10-Year down 2.49% and the 30-Year down 3.87%. Bloomberg US Corp Investment Grade Index declined 1.98%, mortgage-backed securities fell 1.65%, and High Yield Index lost 1.18%.

The weakness in longer-duration Treasuries was especially notable. In a typical geopolitical shock, Treasuries often benefit from safe-haven demand. This time, however, the inflationary implications of higher energy prices appear to have dominated. If oil prices remain elevated, investors may require higher yields to compensate for the possibility of stickier inflation and a longer period of restrictive policy. In that environment, duration becomes more difficult to own even when growth risks are rising.

The key question for bond markets is whether the energy shock proves temporary or more structural. Early April reports suggested meaningful damage to energy infrastructure with some facilities potentially taking extended periods to restore. If that assessment proves correct, markets may need to adjust to a world in which the oil shock is not simply cyclical, but a more persistent drag on global growth and inflation trends.

Federal Reserve and Monetary Policy

The Federal Reserve remains in a wait-and-see posture, with the near-term focus shifting toward the inflationary consequences of the conflict rather than the immediate market volatility. One important signal in March was the move in the 5-Year Breakeven Inflation Rate, which rose 11 basis points to 2.56%. That increase indicates that market-based inflation expectations rose during the month.

At the same time, recent research from Goldman Sachs suggests AI-related displacement is already affecting entry-level and administrative roles, particularly in certain segments of the labor market. While there is still considerable debate around the ultimate labor market impact of AI, the broader point is relevant for policy: the economy may be entering a period where productivity improves even as hiring becomes more restrained.

That leaves the Fed facing a more complicated policy backdrop. Higher oil prices argue for caution on inflation, while slower labor demand could eventually argue for easier policy. For now, the Fed has signaled a cautious approach. The path forward will depend not just on headline inflation, but on whether the current energy shock fades quickly or begins to feed more persistently into inflation expectations and economic activity.

Disclaimers:

Investing involves risk, including possible loss of principal. Past performance does not guarantee future results. No strategy, including diversification, ensures a profit or prevents loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746. Xtollo Investment Partners, LLC (“XIP”) promotes KAM strategies and funds and receives compensation for these activities, which creates a conflict of interest. XIP is not a registered investment adviser or broker-dealer.

Please refer to Important Disclosures | Glossary

KAM20260415

Related Perspectives

View All-

Strategy Review – May 2026

March was shaped by a sharp escalation in US-Iran tensions, a surge in energy prices, and renewed concern that inflation could stay stickier than expected. The Federal Reserve again held rates steady, while higher oil prices and rising yields pressured traditional risk assets.

-

Monthly Market Commentary – May 2026

US equities moved lower in March as the conflict involving Iran, the US, and Israel pushed energy prices sharply higher and added another layer of uncertainty to an already fragile market backdrop. After