Politics Prevail

Monthly Market Commentary

By Kensington Asset Management Team

Geopolitics

In February, Goldman Sachs wrote a report calling 2024 the “Year of Elections”, noting that over half the world’s population was expected to head to polls to vote this year. As part of their analysis, they asked a number of political experts to weigh in on whether the global trend of “democratic backsliding” would continue, and set the stage for less liberal challengers/populists to succeed. Former Council of Foreign Relations President Richard Haase had this to say: “…it’s a particularly tough environment for democracy today. Many countries have run into difficult economic times, especially during and after Covid. And when governments have a harder time delivering resources and services to their people, alternatives—essentially, populists— tend to gain momentum. The pressure on societies from globalization and technological shifts has also made it harder for many individuals to succeed, and social media’s rise has both fueled individuals’ discontent and provided a larger platform for alternatives to democracy and democratic norms to gain traction.” (9/6/2022)

While political scientists can debate the future of democracy, incumbents around the globe unquestionably faced a hostile electorate. In fact, as John Burn-Murdoch of the Financial Times wrote, the incumbents in every single one of the 10 major countries that held national elections in 2024 were voted out of office. This is the first time this has ever happened in almost 120 years of records. Although pundits have pointed to inflation and immigration as the central causes for the upheaval, the unprecedented results strongly suggest historical forces at work. Cem Karsan, CEO of Kai Volatility, has frequently pointed out we have entered a period of political and economic populism and change, not unlike the 1960s. Over that decade and the one to follow, not one President remained in office for two consecutive terms.

Stock Market

Equities experienced a mild decline in October, with the cap-weighted S&P 500 Index down less than a percent, the equal weighted S&P 500 Index declining -1.72%, the Nasdaq 100 Index down -0.85% and the Russell 2000 Small Cap Index off -1.49%. Foreign indices were down as well, with the MSCI EAFE Index losing -1.59% and the MSCI Emerging Market Index lower by -2.87%.

Earnings results for the third quarter reported during the month were, on the whole, positive: with just over 93% of S&P 500 companies reporting, roughly 75% surpassing consensus EPS expectations. In aggregate, earnings growth is tracking at 5.4% year-over-year, marking the fifth straight quarter of earnings growth, per FactSet data.

The positive results took a back seat, though, to the upcoming Presidential and Congressional elections and markets vacillated for the most part buffeted by poll results indicating a very narrow outcome. (It turned out to be anything but of course, and markets raced to all-time highs in the new month on news of a Republican sweep.)

With the forthcoming change in Administrations, investors are understandably focused on what policy changes are on the horizon and how they will affect the economy, corporate profitability and taxes. Already, strategists are ramping up their earnings estimates and price targets as a result. In one of the more bullish forecasts (so far), Ed Yardeni believes the S&P 500 Index will reach 10,000 by the end of the decade. He bases his prediction on a trifecta of positives: 1) President-elect Trump will quickly lower the corporate tax rate from 21% to 15%; 2) the Administration will institute a series of measures that roll back industry regulation, reducing costs; and 3) faster productivity growth as a result of increased corporate investment and realized benefits from the artificial intelligence revolution. Yardeni believes profit margins on the S&P 500 will reach record highs of 13.9% and 14.9% as a result, spurring a bull market not unlike the Roarin’ Twenties. On top of that, Yardeni doesn’t expect another bear market through the end of the decade.

Will this uber-bullish forecast come to pass? Valuations aren’t as high as they were during the internet mania – at least outside of AI companies – but they certainly are nowhere near cheap, historically speaking. In addition, the reduction in tax rates will substantially increase the federal deficit unless the Administration can somehow find enough budget cuts to offset the revenue shortfall. In a budget where only 6.4% of federal spending is discretionary, that stands to be a tall order.

Even if found, those cuts will likely negatively affect someone’s income and spending, in turn reducing overall economic growth. As Peter Berezin of BCA Research stated “tax cuts may help growth and corporate earnings but they may be counteracted by cuts to spending, with many Republicans keen to trim the cost to government of Medicaid, food stamps, housing assistance and other programs that target the poor. Although most of these programs are not huge in absolute terms, they generate sizable [economic] multiplier effects because their recipients generally spend whatever income or transfer payments they receive” (11/8/2024).

Fixed Income

Bond markets struggled in October as investors grappled with the fact that no matter which party gained power, government deficits were set to widen in the years ahead. The benchmark US Treasury 10-year fell -3.55% over the course of the month, the Bloomberg US Aggregate declined -2.48% and the Bloomberg US MBS Index was off -2.83%. Low duration sensitive indices fell less, with the US 2-Year Treasury down fractionally, off -0.64% and the US Corporate High Yield Index lowered by -0.54%.

The upset in the bond market over the past few years has been almost entirely rate driven, with credit being extremely well bid even during times of market volatility. This isn’t surprising given the strength of the fiscal impulse dating back to the pandemic and it may well be in this fixed income cycle, any fireworks seen will be in the sovereign debt sector rather than privates.

Since the Great Financial Crisis, politicians, in tandem with monetary authorities, have made it their mission to smooth out business cycles by injecting liquidity into the economy at any hint of significant distress. While this has succeeded in repairing the private sector’s balance sheet, it has come at the cost of an immense expansion of the publics. And by most economists’ calculations, the new Administration will be adding to that total.

When investors might begin objecting to the size of the deficits is anyone’s guess, but in 2023, the U.K. experienced a trial run of what a Treasury-failed auction might look like as the Gilt market came close to collapse. The impact to global markets, should it happen here, would be an order of magnitude larger.

Federal Reserve and Monetary Policy

The Federal Reserve continues to meet with success in its mission to bring down the growth rate of inflation while remaining supportive of economic growth. The Core Personal Consumption Expenditures Index, the Fed’s favorite inflation measure, showed a year-over-year increase of 2.7% in September, while the annual core consumer price inflation rate registered a 3.3% increase. We hasten to caution that inflation measures have flatlined over the past few months and as Powell himself has suggested, the ultimate path to a 2% inflation rate will be bumpy (if achievable at all).

Both housing and energy prices should help in the months ahead. In regard to energy, the IEA recently trimmed its forecast for demand growth in 2025 to 990,000 barrels a day and said that even if OPEC+ were to keep all cuts in place, it expected crude supply to exceed demand by 1 mbd in 2025. That is a stunning shortfall driven by slower growth out of China in the main, a slowdown likely to continue with the broad imposition of tariffs under the Trump Administration.

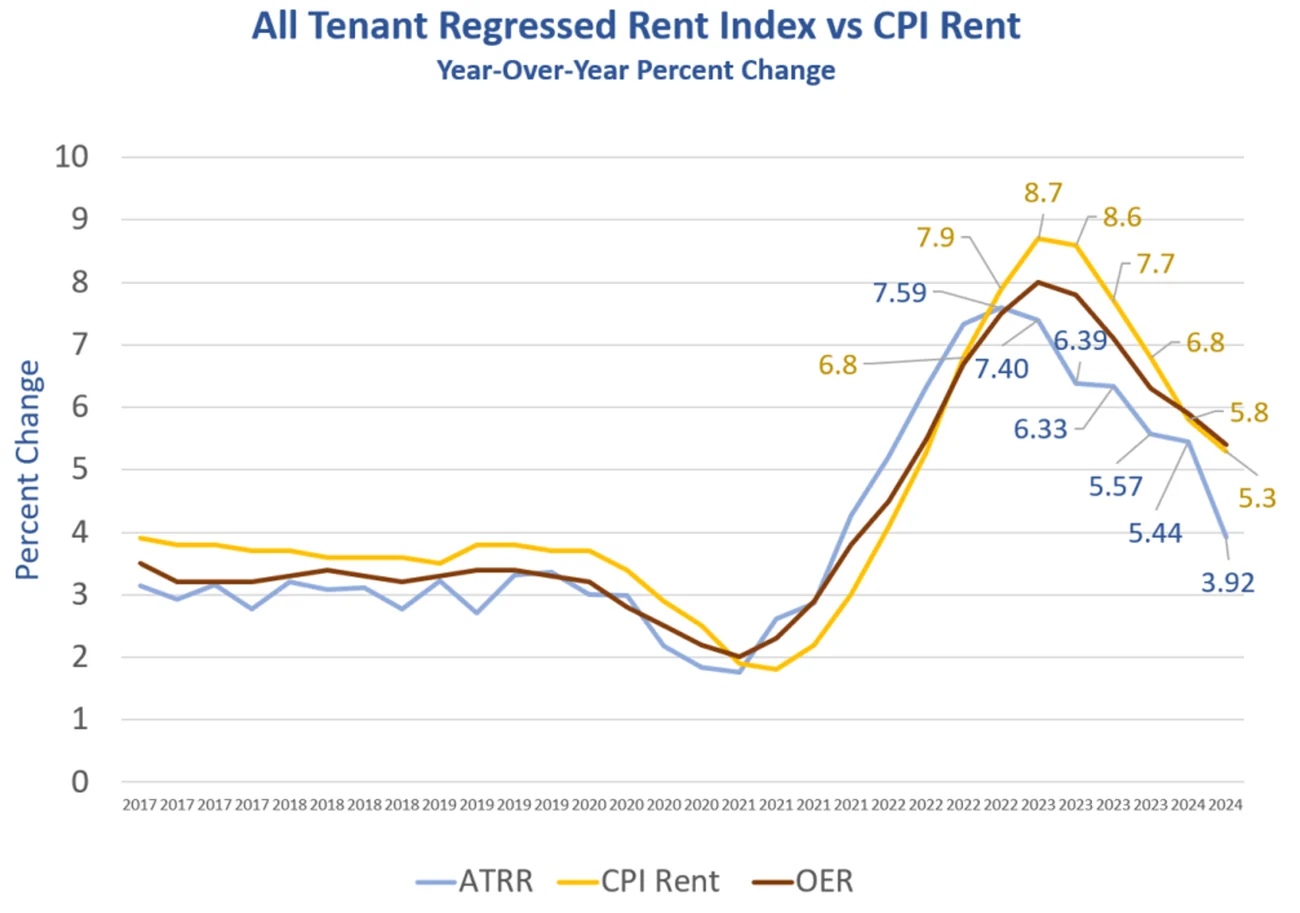

Turning to housing, the rate of increase in housing prices, as measured by the BLS All Tenant Rental Rate (“ATTR”), has been falling steadily over the past several quarters. As it’s a lagging indicator due to smoothing effects, the ATRR’s full impact on the CPI has yet to be felt.

Investors are increasingly bifurcated into two camps on future monetary policy, with one imploring the Federal Open Market Committee (FOMC) to continue on their path of reducing rates in light of slowing growth; while the other is warning financial conditions continue to be quite loose and Powell risks reigniting inflation by lowering rates further and particularly so since the new Administration appears intent on putting in place large scale tariffs and highly stimulative fiscal policy.

Clearly, interest rate markets are growing concerned. The aforementioned Mr. Yardeni famously coined the phrase “bond vigilantes” when characterizing the impact bond investors hold over the economy, and it seems more than likely they will play an outsized role in the months ahead. The press is riveted by the specter of a clash between Chairman Powell and President-elect Trump, but the real battle will be seen in the longer end of the bond market where most corporate financing is done.

Managed Income Strategy – Manager Commentary

As we mentioned last month, September brought market participants the much-anticipated initial rate cut from the Federal Reserve. However, following this announcement, bond yields rose during October. The 10-Year Treasury rate soared from 3.74% to 4.36% during the month. Economic data, such as demand for goods and services, wage growth, and consumer spending, all came in hotter than expected, contributing to the increase in bond yields. Meanwhile, expectations continue to remain high for the Federal Reserve to reduce rates by half a percentage point (or 50 basis points) before the end of 2024.

As yields rose during the month, most segments of the bond market turned into negative performance for the month. However, the senior loan and floating rate segments produced a positive return. High yield was slightly negative for the month. The Managed Income Model remains Risk-On and the current portfolio remains high yield centric, with satellite positions in floating rate and senior loan investments. We anticipate high yield to remain strong at this point, and do not anticipate any changes to the portfolio composition in the short term.

Dynamic Growth Strategy – Manager Commentary

US stocks were mixed during the month of October, holding onto modest gains until month-end, when big tech earnings sparked a sharp selloff. This resulted in a slight loss across all major indices for the month. This broke a five-month winning streak for the S&P and Dow indices. The so-called “Magnificent Seven” stocks experienced a rough end to the month, with Microsoft shares plunging over 6% on Halloween. Meta closed down over 4% on the last day of the month. Nvidia ended the last trading session of October, down approximately 4.7%.

The Dynamic Growth Model was in a Risk-On state for the entirety of the month. Like the major indices, October was generally a positive month, until the October 31 selloff wiped out the monthly gains. The Dynamic Growth Strategy is currently positioned approximately 50% in S&P 500 exposure, with the remaining half of the portfolio in growth stocks. Generally, seasonality favors the months of November and December, particularly in an election year. However, should equities experience increased volatility following this brief selloff, we would expect the Dynamic Growth Model to move back to a Risk-Off state in response. As we noted last month, if future data points toward a continued slowing of the economy, or if inflation fails to continue falling, equities could be under pressure in the months ahead.

Active Advantage Strategy – Manager Commentary

The Active Advantage model remains positioned in a fully Risk-On state, with a balanced posture across fixed income and equities. During the month of October, the portfolio management team significantly reduced its duration-sensitive elements of fixed income, shifting toward high yield and floating rate segments. Given continued pressure on bond yields, the portfolio management team is electing to keep the fixed income side of the portfolio low in duration. On the equity side, Active Advantage remains predominantly invested in core S&P 500 exposure.

As noted above, we believe risks remain elevated for markets in general, as bond yields continue to rise after the rate cut announcement. Further pressure on fixed income could occur if inflation data begins to increase once again in Q4 2024. On the equity side, we remain positioned primarily in core equities to guard against volatility as the major indices reach for all-time highs once again.

Defender Strategy – Manager Commentary

October 2024 was marked by heightened market volatility driven by a mix of geopolitical tensions, fluctuating bond yields, and concerns over a potential economic slowdown. The Federal Reserve’s mixed signals on interest rate policy added uncertainty, with investors remaining cautious amid inflation concerns and signs of a tightening labor market. Equities, particularly in growth and tech sectors, saw modest returns, while hard asset sectors like gold and real estate showed continued gains.

The Kensington Defender Strategy demonstrated resilience in October, showing a moderate decline relative to broader indices. The strategy’s defensive positioning, focused on capital preservation and risk management, helped mitigate the impact of market turbulence.

Looking ahead, the Kensington Defender Strategy remains committed to its strategy of defensive growth. The current macroeconomic environment suggests continued volatility, especially as the market awaits further clarity on the Federal Reserve’s monetary policy path and the broader economic outlook. The Strategy will continue to focus on the disciplined approach and fixed income securities that are better positioned to withstand a potential economic slowdown, while being prepared to capitalize on market dislocations as they arise.

Hedged Premium Income Strategy – Manager Commentary

September and October tend to be notorious for equity volatility. After living up to this reputation in September, where the S&P 500 Index traded in a 6.75% range, October was relatively quiet, with the market only trading in a sub-4% range. Despite it being a relatively quiet month, option prices (as measured by implied volatility) exploded higher in front of three consecutive “known market events:” 1) the November jobs report, 2) the Election, and 3) the FOMC decision and press conference. The 9-day implied volatility index for the S&P 500 (CBOE S&P 500 9-Day Volatility Index) catapulted from under 13 to just over 27. It is very unusual to see this happen when the market is quiet, but in this case, it is very understandable as traders and investors bought both puts and calls to express directional views relating to the pending events.

For the second consecutive month in the Hedged Premium Income Strategy, the S&P 500 Index finished the expiration cycle near the upper end of our short call spreads. This is unfortunate, as it did not allow our investors to participate in any market appreciation. Rather, the return was limited to the net option premium realized during the cycle.

On October 18th, the income-generating call spreads were reset to the new higher levels, resulting in the cap moving higher. The option premium collected for the month was above the long-term average, keeping the current income pace near the high end of the range of our expectations. With the potential for a volatile end to the year, the Strategy continues to be well positioned to benefit from a flat, sharply lower or sharply higher market.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular strategy such as the types of securities being substantially different.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Managed Income Strategy

Risks specific to the Managed Income Strategy include Management Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Non-Diversification Risk, Turnover Risk, US Government Securities Risk, LIBOR Risk, Models and Data Risk.

Dynamic Growth Strategy

Risks specific to the Dynamic Growth Strategy include Management Risk, Equity Securities Risk, Market Risk, Underlying Funds Risk, Non- Diversification Risk, Small and Mid-Capitalization Companies Risk, Turnover Risk, US Government Securities Risk, Models and Data Risk.

Active Advantage Strategy

Risks specific to the Active Advantage Strategy include Management Risk, Equity Securities Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Limited History of Operations Risk, Non-Diversification Risk, Small and Mid-Capitalization Companies Risk, Turnover Risk, US Government Securities Risk, LIBOR Risk, Models and Data Risk.

Defender Strategy

Risks specific to the Defender Strategy are detailed in the prospectus and include general market risk, credit risk, interest rate risk, management risk, equity securities risk, fixed-income securities risk, high-yield bond risk, foreign investment risk, emerging markets risk, real estate and REITs risk, commodities risk, currency risk, subsidiary risk, market risk, underlying funds risk, derivatives risk, limited history of operations risk, turnover risk, models and data risk, momentum risk or risk of the portfolio not performing as expected.

Hedged Premium Income Strategy

The Strategy invests in options that derive their performance from the performance of the S&P 500 Index. Selling (writing) and buying options are speculative activities and entail greater than ordinary investment risks. The Strategy’s use of put options can lead to losses because of adverse movements in the price or value of the underlying asset, which may be magnified by certain features of the options. When selling a put option, the Strategy will receive a premium; however, this premium may not be enough to offset a loss incurred by the Strategy if the price of the underlying asset is below the strike price by an amount equal to or greater than the premium. Purchased put options may expire worthless and the Strategy would lose the premium it paid for the option. The Strategy may lose significantly more than the premiums it receives in highly volatile market conditions.

The Strategy will invest in short term put options which are financial derivatives that give buyers the right, but not the obligation, to sell (put) an underlying asset at an agreed-upon price and date. The Strategy’s use of options may reduce the Strategy’s ability to profit from increases in the value of the underlying asset. The Strategy could experience a loss or increased volatility if its derivatives do not perform as anticipated or are not correlated with the performance of their underlying asset or if the Strategy is unable to purchase or liquidate a position.

Definitions:

Bloomberg US Aggregate Bond Index: An unmanaged index comprised of US Investment grade fixed rate bond market securities, including government agency, corporate and mortgage-backed securities. Investors cannot invest directly in an index. It is also known as US Aggregate Bond Index.

Bloomberg US Corporate Investment Grade Bond Index: An unmanaged index comprised of US investment grade fixed rate, taxable corporate bond market.

Bloomberg US Corporate High Yield Index: An unmanaged market value-weighted index that covers the universe of fixed-rate, non-investment grade debt in the US. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

Bloomberg US Mortgage-Backed Securities (MBS) Index: An unmanaged index that tracks fixed-rate agency mortgage-backed pass-through securities guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The index is constructed by grouping individual TBA-deliverable MBS pools into aggregates or generics based on program, coupon, and vintage.

BLS All Tenant Rental Rate (“ATTR”): Published by the US Bureau of Labor Statistics, this index measures the rent paid by all renters, both new and continuing, and incorporates data from the Consumer Price Index (CPI) Housing Survey.

Call Spread: An options trading strategy where the Strategy buys and sells call options on the same asset with different strike prices or expiration dates. The strategy helps manage risk and profit from small price changes.

Covered Call: An options strategy where a long asset position is held while a call option is sold. This generates income from the premiums received for selling the call option, but limits potential upside gains if the asset price rises above the strike price.

NASDAQ 100 Index: A market index that comprises of the one hundred largest, most actively traded companies listed on the Nasdaq stock exchange.

Russell 2000 Small Cap Index: A market index that consists of 2,000 small-cap US companies that are part of the larger Russell 3000 Index.

S&P 500: A capitalization weighted index of 500 stocks representing all major domestic industry groups. The S&P 500 TR Index assumes the reinvestment of dividends and capital gains.

MSCI EAFE Index: An international equities market index that consists of large and mid-cap stocks across developed markets in Europe, Australasia, and Far East Asia. Excludes US and Canadian equities.

MSCI Emerging Markets Index: An international equities market index that consists of large and mid-cap stocks across 24 emerging market countries that include but not limited to Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, South Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and United Arab Emirates.

KAM20241118A

Related Perspectives

View All-

Strategy Review – May 2025

February saw heightened volatility as investors reassessed the economic impact of newly imposed trade tariffs. While the market had initially assumed tariffs were a bargaining tactic, the confirmation of their implementation triggered a swift correction.

-

Kensington Monthly Commentary – May 2025

The stock market endured one of its most volatile months in years. The S&P 500 fell 21.35% from its February 19 peak of 6,147.43 before bottoming on April 7 at 4,835.04, shortly before the Administration announced a 90-day pause on new tariffs (excluding China). Markets quickly rebounded on the news, with the S&P 500 soaring 9.52% on April 9, its largest single-day gain since October 2008. The Nasdaq Composite jumped 12.16% the same day, marking its biggest one-day percentage gain since January 3, 2001, and the second-largest on record.