The Age of Global Populism

Monthly Market Commentary

By Kensington Asset Management Team

Geopolitics

The period of global populism we are living through promises to be one of wrenching change, not all of it peaceful. The recent assassination of a senior health care executive, while morally repugnant, is but one sign of socio-economic conflict intermixed with a generational transition not unlike what took place in the 1960s.

Part and parcel is a world in chaos. The French government lost a no-confidence vote early this month, as Macron’s popularity level fell to the lowest level since becoming President in 2017. In lock step, Germany’s ruling coalition collapsed, paving the way for early elections in 2025 (its economy, the world’s third largest, is expected to shrink in 2024 for the second year in a row). South Korea’s government recently declared martial law before reversing field, leaving its future in grave doubt. Russia’s prospects have been severely diminished by a catastrophic three-year war (inflation is 8.9% and rising, interest rates are now over 20% and economic growth is forecast to plunge to a meager 0.5% in 2025). Iran, whose economy is struggling, pinched by Western sanctions and a war with Israel, is dealing with the fallout from a Middle East policy in shambles after the overthrow of the Alawite regime in Syria. China’s growth remains stubbornly weak, its bond yields hitting historical lows as it faces a US (and quite possibly European) intent on forcing a rebalancing of trade policy.

All this has left the US in an advantageous negotiating position just as a new Administration takes office, resolved to rewriting the terms of global engagement. Part of that negotiating strategy is willful unpredictability, leaving both long-time partners and enemies searching for clues on President-elect Trump’s intentions. One thing seems certain – it will be commercial, ad-hoc in many cases, and have an “America First” imprint.

fixed income

Bond markets rebounded smartly in November, recouping some of the large losses incurred in the prior month. The benchmark S&P US Treasury Bond Current 10-Year Index gained 1.01%, the S&P US Treasury 30-Year Index gained 2.0%, while the Bloomberg US Corporate Investment Grade Index returned 1.34%, Bloomberg US Corporate High Yield Index returned 1.15% and Bloomberg US MBS Index finished the month up 1.33%.

The positive performance emanated from both fundamental and technical factors. In line, inflation numbers were supportive and coincided with a substantial drop in price volatility. The Merrill Lynch Option Volatility Estimate (MOVE) Index – which measures expectations of future price volatility based on the implied volatility of one-month Treasury options – dropped nearly 25%, as investors who had hedged against the possibility of a contested Presidential election quickly closed their positions. This volatility crush translated into an immediate liquidity boost (lenders being more willing to finance risk assets), driving both stock and bond markets higher.

Tellingly, during the entire run up to the election credit spreads simply chose to ignore the doomsters, actually tightening to multi-year lows.

Looking forward, rates are sending a contradictory message. Futures are pricing in Fed cuts of 100 basis points over the next year while the 2-year Treasury rate currently sits at 4.25%, an unusually wide gap in short term rate expectations. The performance of the long end may be an important tell and, as of this writing, the 10-year Treasury has backed up 80 bps in yield since the Fed began cutting in September. Looking back at the last seven Fed easing cycles dating to 1989, this just happens to be its worst performance over a comparable time frame.

stock market

Equities enjoyed a “Trump Bump” in November, with small-cap equities being a particular standout. The Russell 2000 Index gained an eye-opening 10.84%, while the S&P 500 Index returned 5.73% and the Nasdaq 100 Index 5.23%. Unsurprisingly, foreign exchanges lagged with the Euro Stoxx 50 Index finding itself in the red, down -0.48%, the MSCI EAFE Index up a slight 0.58%, and the MSCI Emerging Market Index down -2.74%. The combination of a stronger US dollar and the specter of a more nationalist America served to drag down overseas markets and ignite large foreign inflows into the US.

The significant disparity in stock market performance between the US and foreign markets has been a key feature of this bull market, reaching historical extremes as can be seen in the graph below:

From a longer-term perspective, there are multiple fundamental reasons for this divergence: the US relies to a far greater extent on fixed interest rate financing, both in the corporate and mortgage markets and is consequently much more immune to the global central bank tightening that started in the first quarter of 2022. By contrast, mortgage financing in Europe is predominantly done using floating rate instruments, which means consumer demand is much more sensitive to the level of short term rates. This structural distinction accounts for much of the differential in growth rates between the two continents.

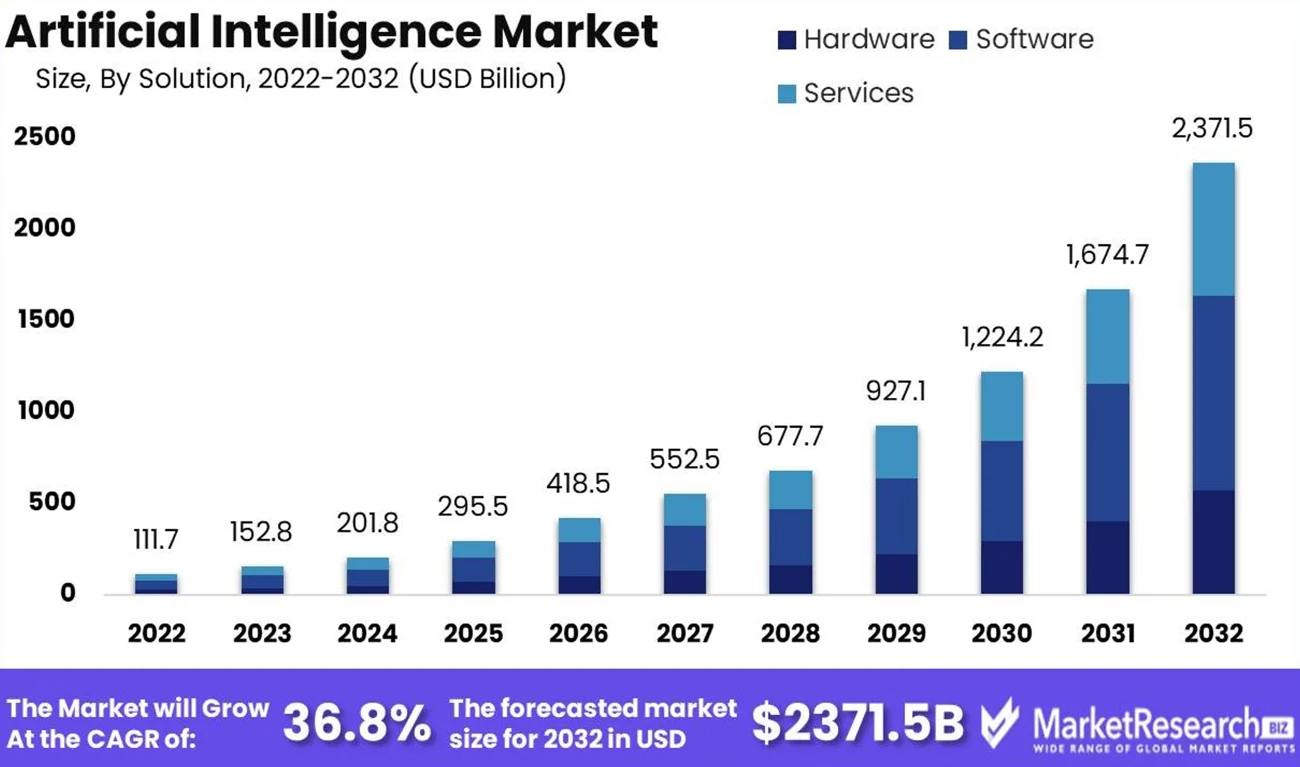

In addition, the US is amid a capital investment boom, driven by demand for artificial intelligence tools and the energy transition. Goldman Sachs estimates the AI infrastructure build-out will cost over $1 Trillion in the next several years alone, which includes spending on data centers, utilities, and applications. When including software, the number grows to over $2 Trillion by 2032:

Federal Reserve and Monetary Policy

Monetary policy remains on a steady trajectory toward lower short-term rates (the Fed will likely have lowered Fed Funds rate by 25 bps by the time we go to press) but the more pressing issue will be the market’s reaction to such a decrease. As has been crystal clear for many months, overall financial conditions are loose and investor behavior is exhibiting signs of euphoria. On top of this, core PCE prices rose 0.3% month over month in October, in line with expectations but showing little progress in achieving the Fed’s 2% goal.

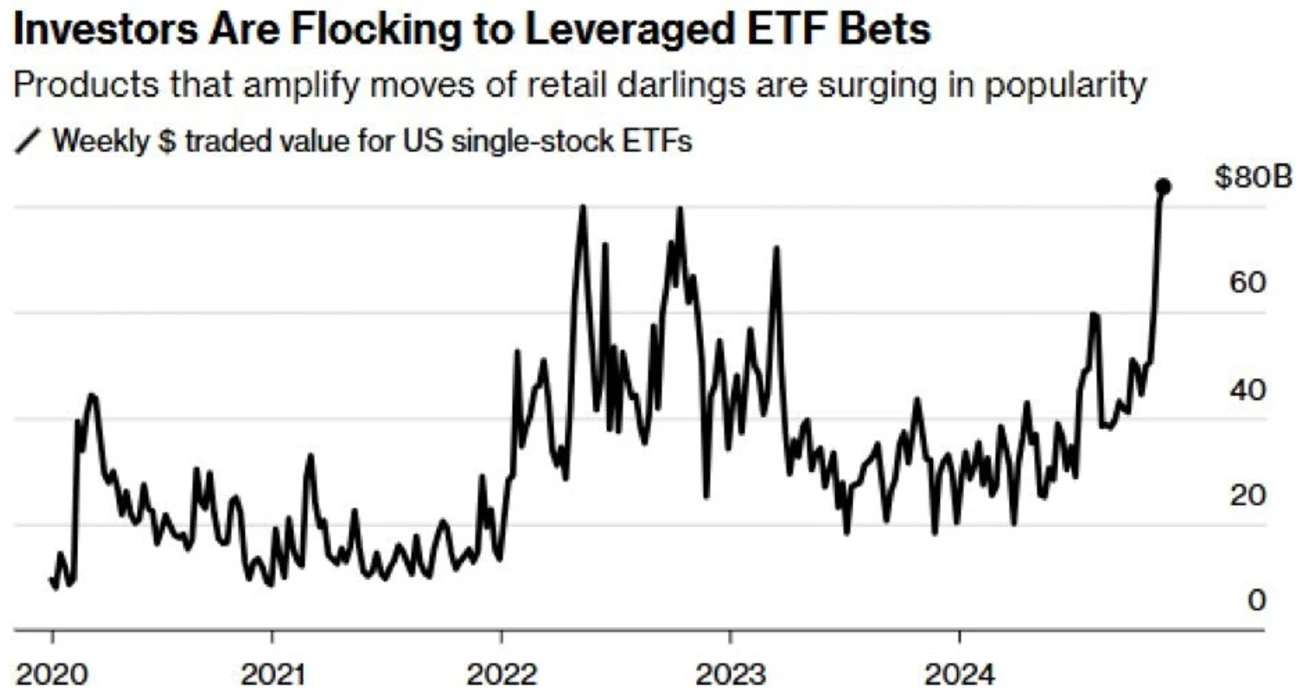

Because the economy is much less sensitive now to short-term rates for reasons explained above, the Fed will want to pay attention to other drivers of economic expansion, in particular the direction of equity markets and long-term rates and their effect on demand and production. With the public now fully engaged in and enthusiastically embracing leverage (chart below), it’s not difficult to imagine a market correction of some magnitude directly impacting consumer purchasing habits and overall economic activity.

Managed Income Strategy – Manager Commentary

After yields increased dramatically during the month of October, the bond markets saw some mean reversion in November. The 10-Year Treasury yield finished the month at 4.18%, down slightly from its starting point of 4.36%. Thanks to this relief rally, all flavors of fixed income experienced gains during the month.

On November 7, the Federal Open Market Committee announced a reduction in the federal funds rate by a quarter percentage point, or 25 basis points. At the accompanying press conference, Federal Reserve Chair Jerome Powell noted sentiment around the broader remains very strong. However, Powell noted overall US fiscal policy, particularly the level of debt to GDP, is on “an unsustainable path,” and must be dealt with. Looking ahead, market participants continue to price in one more 25 basis point cut to close out the year in December.

Heading into the close of the year, the Managed Income Model remains Risk-On and there have been no sizable changes to the portfolio. We remain high yield centric, with satellite positions in floating rate and senior loan investments. The current high yield spread, or the difference between high yield rates and the risk-free rate, is the lowest since 2007. In our view, this signals the relative “expensiveness” of the asset class, as investors search for meaningful yield. We continue to hold positions yielding a higher level than short-term Treasuries.

At this time, we do not anticipate any major changes to the portfolio. Because of tight spreads in the high yield market, we continue to hold floating rate/senior loan positions, which can potentially buffer against losses should the high yield market pull back in the short term.

Dynamic Growth Strategy – Manager Commentary

Market participants piled into equities during November, particularly after the US elections. This follows traditional seasonal patterns for election years, with risk assets posting gains across the board in what is already a typically strong month for equities. After snapping a five-month winning streak in October, the S&P 500 and Nasdaq Composite Index roared back, posting gains of 5.7% and 6.2%, respectively, and finished November at fresh all-time highs.

Dynamic Growth benefited from November’s strong gains, posting its best month since July 2022. Dynamic Growth is still positioned approximately 50% in S&P 500 exposure, with the remaining half of the portfolio in growth stocks. Looking ahead, December often exhibits strong seasonality as well. However, despite the strong post-election runup in stocks, we believe that if future data points toward a continued slowing of the economy, or if inflation fails to continue falling, equities could be under pressure in the months ahead. In November, the forward 12-month Price/Earnings ratio for the S&P 500 posted its highest reading since April 2021, suggesting equities are looking relatively expensive. A wave of “profit taking” could also act as a headwind for equities as we close out the year. However, for now, equities continue to mark new all-time highs.

Active Advantage Strategy – Manager commentary

In November, Active Advantage benefitted from rising risk assets across the board, during the month. The Active Advantage Model remains positioned in a fully Risk-On state, with a balanced posture across fixed income and equities. On the fixed income side, we continue to lean into high yield and floating rate/senior loan holdings. While yields did decline somewhat during October, we remain cautious given the possibility of inflation to tick up as we move into 2025. For equities, Active Advantage is positioned predominantly in core S&P 500 exposure, with satellite holdings in growth stocks and low volatility sectors.

For this reason, we believe Active Advantage is well-positioned should markets end the year on a high note; however, on both the fixed income and equity sides of the portfolio, we have placed in satellite holdings designed to mitigate downside, should yields push higher, or if equities falter down the stretch.

Defender Strategy – Manager commentary

November was marked by significant market activity as investors continued to navigate a challenging macroeconomic environment and a contentious US election that created uncertainty. Inflationary pressures showed signs of easing, prompting central banks to adopt a more measured tone regarding future rate hikes. Equity markets rallied during the month, with major indices posting strong gains, while bond yields experienced modest declines. Geopolitical tensions, particularly in Europe, contributed to market volatility, but overall investor sentiment improved as economic data showed resilience.

The Kensington Defender Strategy delivered a positive result in November. The Strategy’s robust performance was driven by disciplined asset allocation of the top 6 asset classes with the most momentum. The asset class that attributed the most to the return on the month was US Small Cap Equities, followed by US Large Cap Equites and Real Estate, as well as the option overlay strategy. The asset classes that detracted from performance in the month were Gold and Emerging Markets. The fund maintained its commitment to downside protection by actively managing exposure assets based on momentum. Tactical adjustments away from emerging markets and into high yield around the middle of the month in addition to the options overlay, helped reduce some drawdown and outperform the benchmark.

As the year concludes, the Kensington Defender Strategy remains focused on delivering consistent, risk-adjusted returns. While headwinds such as global economic slowdown and geopolitical risks persist, the easing of monetary policy pressures and resilient corporate earnings provide a constructive backdrop. The Strategy will continue leveraging its disciplined investment process to identify opportunities that align with its long-term objectives.

Hedged Premium Income Strategy – Manager Commentary

The expectations of many market participants was that multiple “known market events” (the November jobs report, the election, and the FOMC decision and press conference) would likely spark a wave of equity volatility in November. As it turned out, a decisive and drama-free election along with a continued dovish stance by the Fed drove equity markets higher, with the S&P 500 gapping up almost 6% for the month and equity volatility (as measured by the CBOE Volatility Index (“the VIX”) dropping over 35%. The VIX finished the month at 13.51, which is well below the long-term average of close to 20 as traders anticipated a quiet December that tends to benefit from strong seasonality.

The Hedged Premium Income Strategy benefited from two key factors during the month. First, the S&P 500 Index had a brief pullback during the month that brought the Index down to the short call strikes in the strategy on the day they expired. This resulted in the options that were written expiring nearly worthless, allowing the Strategy to maximize the value of writing those options. Second, after resetting the call strikes, the market resumed rallying and finished the month near the top end of the call spread range. This is important in that the Strategy is well positioned to participate in any continued market appreciation in December, while also having a meaningful amount of protection in place.

When the income-generating call spreads were reset to new levels on November 15th, the option premium collected for the month was above the long-term average, keeping the current income pace near the high end of the range of our expectations. Overall, the Strategy continues to be well positioned to benefit from a flat, sharply lower or sharply higher market.

Disclaimers:

Investing involves risk, including loss of principal. Past performance does not guarantee future results. There is no guarantee any investment strategy will generate a profit or prevent a loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Kensington Asset Management, LLC (“KAM”) relies on third party sources for some of its information that we believe is reliable. However, we make no representation, warranty, endorse or affirm as to its accuracy or completeness. The information provided is current as of the date of publication and may be subject to change. We are not responsible for updating this information to reflect any subsequent developments or events.

Any indices and other financial benchmarks shown are provided for illustrative purposes only, are unmanaged, reflect reinvestment of income and dividends and do not reflect the impact of advisory fees. Investors cannot invest directly in an index. Comparisons to indexes have limitations because indexes have volatility and other material characteristics that may differ from a particular strategy such as the types of securities being substantially different.

Certain information contained herein constitutes “forward-looking statements,” which can be identified using forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results, or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance, or a representation as to the future.

Advisory services offered through Kensington Asset Management, LLC, Barton Oaks Plaza, Bldg II, 901 S Mopac Expy – Ste 225, Austin, TX 78746.

Managed Income Strategy

Risks specific to the Managed Income Strategy include Management Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Non-Diversification Risk, Turnover Risk, US Government Securities Risk, LIBOR Risk, Models and Data Risk.

Dynamic Growth Strategy

Risks specific to the Dynamic Growth Strategy include Management Risk, Equity Securities Risk, Market Risk, Underlying Funds Risk, Non- Diversification Risk, Small and Mid-Capitalization Companies Risk, Turnover Risk, US Government Securities Risk, Models and Data Risk.

Active Advantage Strategy

Risks specific to the Active Advantage Strategy include Management Risk, Equity Securities Risk, High-Yield Risk, Fixed-Income Security Risk, Foreign Investment Risk, Loans Risk, Market Risk, Underlying Funds Risk, Limited History of Operations Risk, Non-Diversification Risk, Small and Mid-Capitalization Companies Risk, Turnover Risk, US Government Securities Risk, LIBOR Risk, Models and Data Risk.

Defender Strategy

Risks specific to the Defender Strategy are detailed in the prospectus and include general market risk, credit risk, interest rate risk, management risk, equity securities risk, fixed-income securities risk, high-yield bond risk, foreign investment risk, emerging markets risk, real estate and REITs risk, commodities risk, currency risk, subsidiary risk, market risk, underlying funds risk, derivatives risk, limited history of operations risk, turnover risk, models and data risk, momentum risk or risk of the portfolio not performing as expected.

Hedged Premium Income Strategy

The Strategy invests in options that derive their performance from the performance of the S&P 500 Index. Selling (writing) and buying options are speculative activities and entail greater than ordinary investment risks. The Strategy’s use of put options can lead to losses because of adverse movements in the price or value of the underlying asset, which may be magnified by certain features of the options. When selling a put option, the Strategy will receive a premium; however, this premium may not be enough to offset a loss incurred by the Strategy if the price of the underlying asset is below the strike price by an amount equal to or greater than the premium. Purchased put options may expire worthless and the Strategy would lose the premium it paid for the option. The Strategy may lose significantly more than the premiums it receives in highly volatile market conditions.

The Strategy will invest in short term put options which are financial derivatives that give buyers the right, but not the obligation, to sell (put) an underlying asset at an agreed-upon price and date. The Strategy’s use of options may reduce the Strategy’s ability to profit from increases in the value of the underlying asset. The Strategy could experience a loss or increased volatility if its derivatives do not perform as anticipated or are not correlated with the performance of their underlying asset or if the Strategy is unable to purchase or liquidate a position.

Definitions:

Bloomberg US Corporate Investment Grade Bond Index: An unmanaged index comprised of US investment grade fixed rate, taxable corporate bond market.

Bloomberg US Corporate High Yield Index: An unmanaged market value-weighted index that covers the universe of fixed-rate, non-investment grade debt in the US. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below. Bonds from issuers with an emerging markets country of risk, based on the indices’ EM country definition, are excluded.

Bloomberg US Mortgage-Backed Securities (MBS) Index: An unmanaged index that tracks fixed-rate agency mortgage-backed pass-through securities guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The index is constructed by grouping individual TBA-deliverable MBS pools into aggregates or generics based on program, coupon, and vintage.

Call Spread: An options trading strategy where the Strategy buys and sells call options on the same asset with different strike prices or expiration dates. The strategy helps manage risk and profit from small price changes.

CBOE Volatility Index (VIX): Often called the “fear index,” measures the market’s expectations for volatility over the next 30 days based on S&P 500 index options. It is a key indicator of market sentiment, with higher values indicating greater expected volatility.

Covered Call: An options strategy where a long asset position is held while a call option is sold. This generates income from the premiums received for selling the call option, but limits potential upside gains if the asset price rises above the strike price.

Euro Stoxx 50 Index: A market capitalization-weighted stock index that represents the 50 largest blue-chip European companies operating within the eurozone nations.

NASDAQ 100 Index: A market index that comprises of the one hundred largest, most actively traded companies listed on the Nasdaq stock exchange.

NASDAQ Composite: A market capitalization-weighted index that includes over 2,500 stocks listed on the NASDAQ stock exchange. It is heavily weighted towards the technology sector, making it a key indicator of tech industry performance.

Russell 2000 Small Cap Index: A market index that consists of 2,000 small-cap US companies that are part of the larger Russell 3000 Index.

S&P 500: A capitalization weighted index of 500 stocks representing all major domestic industry groups. The S&P 500 TR Index assumes the reinvestment of dividends and capital gains.

S&P US 30Y Treasury Index: Tracks the performance of U.S. Treasury bonds with maturities of 30 years. It reflects the long-term interest rate environment and is used by investors to gauge the performance of long-term government debt.

S&P US Treasury Bond Current 10 – Year Index: The S&P U.S. Treasury Bond Current 10-Year Index is a one-security index comprising the most recently issued 10-year U.S. Treasury note or bond.

MSCI EAFE Index: An international equities market index that consists of large and mid-cap stocks across developed markets in Europe, Australasia, and Far East Asia. Excludes US and Canadian equities.

MSCI Emerging Markets Index: An international equities market index that consists of large and mid-cap stocks across 24 emerging market countries that include but not limited to Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, South Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and United Arab Emirates.

KAM20241219A

Related Perspectives

View All-

Strategy Review – May 2025

February saw heightened volatility as investors reassessed the economic impact of newly imposed trade tariffs. While the market had initially assumed tariffs were a bargaining tactic, the confirmation of their implementation triggered a swift correction.

-

Kensington Monthly Commentary – May 2025

The stock market endured one of its most volatile months in years. The S&P 500 fell 21.35% from its February 19 peak of 6,147.43 before bottoming on April 7 at 4,835.04, shortly before the Administration announced a 90-day pause on new tariffs (excluding China). Markets quickly rebounded on the news, with the S&P 500 soaring 9.52% on April 9, its largest single-day gain since October 2008. The Nasdaq Composite jumped 12.16% the same day, marking its biggest one-day percentage gain since January 3, 2001, and the second-largest on record.