2025 Year-End Market Review

Monthly Strategy Commentary

By Kensington Asset Management Team

Equities

A flat December did little to tarnish what was another exceptional year for US equities. The S&P 500 finished the month essentially unchanged (-0.05%) but still managed a rare three-peat, delivering returns in excess of 15% for the third consecutive year and ending 2025 up 16.39%. The Nasdaq 100 and Russell 2000 both declined modestly in December (-0.73% and -0.74%, respectively), yet posted strong full-year gains of 20.17% and 11.29%. The equal-weighted S&P 500 stood out, rising 0.25% in December and finishing the year up 9.34%.

International markets also ended the year on a strong note. The MSCI EAFE Index gained 2.07% in December and 20.60% for the year, while the MSCI Emerging Markets Index advanced 2.61% in December and an impressive 31.28% in 2025.

Outside of equities, precious metals delivered one of their strongest years in decades, with the GSCI Gold Total Return Index up 62.47%. The US dollar moved sharply in the opposite direction, with the Bloomberg US Dollar Spot Index declining 8.10%.

The Year of the Retail Investor

If 2025 had a defining market narrative, it was the growing influence of the retail investor. Long viewed skeptically, individual investors consistently added exposure during periods of market weakness, demonstrating a willingness to lean into volatility rather than retreat from it. In contrast, many professional investors remained cautious amid concerns around artificial intelligence valuations, persistent inflation, and the Federal Reserve’s ability to engineer a soft landing. Despite several bouts of volatility, particularly around tariff-related developments, maintaining equity exposure ultimately proved to be the correct posture for the year.

Retail participation was evident not only through steady equity inflows but also through increased engagement with more tactical market instruments. Combined with the growing prevalence of systematic and momentum-oriented strategies, this behavior contributed to market dynamics that favored upside persistence once rallies became established. The result was a market environment that, for much of the year, displayed a notable resilience to pullbacks and a tendency for strength to build upon itself.

Earnings and the Path Forward

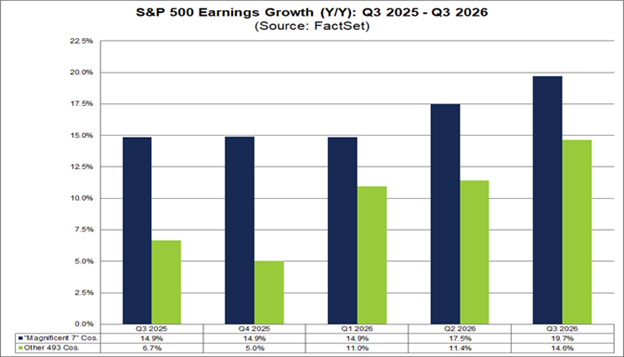

Importantly, equity gains were not driven solely by flows and sentiment. At the start of the year, analysts expected S&P 500 earnings to grow roughly 15% year over year. As is typical, those estimates drifted lower as the year progressed, driven by guidance changes and conservative analyst revisions. However, that pattern was not uniform. While the broader, non-megacap portion of the index followed the traditional downward revision path, the large technology and AI-oriented companies were notable exceptions, with earnings expectations rising over the course of the year.

Looking ahead, consensus expectations once again call for approximately 15% earnings growth. While the so-called “Magnificent Seven” are projected to grow earnings at a robust 22.7% pace, a central theme for 2026 is expected to be broadening participation. The remaining 493 companies in the S&P 500 are forecast to grow earnings by 12.5%, a meaningful acceleration from 2025. Net profit margins are projected to reach 13.9%, which would be the highest level recorded since FactSet began tracking the data in 2008.

Earnings Growth Is Expected to Broaden Beyond the Magnificent 7

Source: FactSet as of October 20, 2025

Earnings growth should continue to benefit from supportive tax policy and ongoing AI adoption. With an election year underway, the Administration has emphasized policies aimed at improving affordability and economic participation. Running the economic engine “hot” may support corporate profits, but it also implies a greater draw of liquidity into the real economy.

High nominal growth, however, reduces the urgency for aggressive interest rate cuts. That dynamic likely caps valuation multiples, suggesting that in 2026 equity returns will rely more heavily on earnings growth than on falling discount rates.

Fixed Income

December was a mixed month for fixed income, shaped largely by a steepening yield curve. The 2-year Treasury gained 0.32%, while longer-dated Treasuries declined, with the 5-year down 0.22%, the 10-year down 0.81%, and the 30-year falling 2.28%. Credit markets were relatively resilient. The Bloomberg US Corporate Investment Grade Index declined 0.20%, the Bloomberg Mortgage-Backed Securities Index rose 0.21%, and the Bloomberg High Yield Index gained 0.57%.

For the full year, US fixed income delivered solid, if unspectacular, returns, with most domestic bond indices gaining between 7% and 8%. Long-duration Treasuries once again lagged, with the 30-year returning just 3.60%, barely preserving purchasing power. Currency effects, however, drove significant dispersion across global portfolios. With the Bloomberg US Dollar Spot Index down more than 8%, foreign investors in US bonds saw muted returns, while US investors in unhedged foreign bonds benefited materially.

Inflation, Rates, and Credit Risks

Inflation was the dominant macro uncertainty entering 2025. Many investors anticipated a renewed surge in prices driven by tariff policy and expanding fiscal deficits. Inflation data, however, remained relatively contained, hovering near 3% for much of the year. At the same time, consumer inflation expectations rose meaningfully, with the University of Michigan’s one-year inflation expectation reaching 4.3% early in the year. This divergence led the Federal Reserve to emphasize patience, dampening expectations for rapid rate cuts.

Institutional investors responded by shifting exposure toward the middle of the yield curve, seeking to balance inflation and rate risks. In hindsight, risks materialized at both ends of the curve. Inflation proved more benign than feared, allowing the Fed to ease later in the year and limiting short-end returns. Meanwhile, large fiscal deficits and geopolitical uncertainty weighed on long-duration bonds as investors reduced exposure.

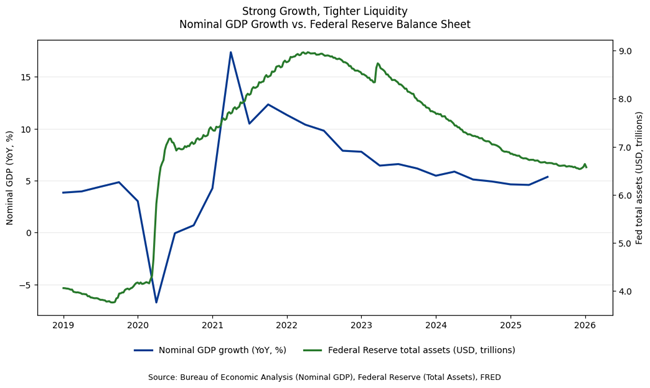

Looking ahead, most analysts advocate for maintaining neutral duration, with returns likely driven primarily by coupon income rather than price appreciation. That outlook comes with important caveats. A re-accelerating economy, fueled by fiscal stimulus and favorable tax policy, could reduce financial market liquidity even as growth remains strong, increasing volatility across risk assets. The chart below highlights this divergence between resilient economic growth and a tightening liquidity backdrop.

Credit markets also warrant close monitoring. While broad high yield indices appear healthy, the lowest-rated segment faces a meaningful refinancing challenge. CCC-rated debt maturities are expected to reach $62.1 billion in 2026, more than double the amount maturing in 2025. Slower refinancing in this tier raises the risk of a localized increase in defaults. Similar dynamics bear watching in private credit markets, where valuation marks can mask underlying risk until a sudden credit event forces a sharp repricing.

The Federal Reserve and the Shift Toward Fiscal Policy

Chair Jerome Powell’s term as Federal Reserve Chair is nearing its conclusion, and the final stretch has been marked by unusual political tension. The Administration has initiated a Department of Justice investigation related to cost overruns at the Federal Reserve’s headquarters renovation, a move Powell has publicly characterized as a pretext tied to policy disagreements. To date, the episode has had little direct impact on monetary policy decisions.

More broadly, the controversy may obscure a more consequential shift underway: a move away from monetary policy as the primary economic lever and toward more direct fiscal intervention. Treasury Secretary Bessent has articulated a clear preference for policies that channel support directly to households rather than through financial markets. Programs focused on tax relief, household affordability, and family support signal an increased reliance on fiscal policy to drive economic outcomes.

If sustained, this approach could reduce the Federal Reserve’s centrality in economic management, positioning it more as a supporting institution than the primary engine of stimulus. For investors, this evolution underscores the importance of monitoring not just interest rate policy, but also the scale, structure, and financing of fiscal initiatives in the years ahead.

Disclaimers:

Investing involves risk, including possible loss of principal. Past performance does not guarantee future results. No strategy, including diversification, ensures a profit or prevents loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Please refer to Important Disclosures | Glossary

KAM20260115

Related Perspectives

View All-

Strategy Review – May 2026

March was shaped by a sharp escalation in US-Iran tensions, a surge in energy prices, and renewed concern that inflation could stay stickier than expected. The Federal Reserve again held rates steady, while higher oil prices and rising yields pressured traditional risk assets.

-

Monthly Market Commentary – May 2026

US equities moved lower in March as the conflict involving Iran, the US, and Israel pushed energy prices sharply higher and added another layer of uncertainty to an already fragile market backdrop. After