Kensington Monthly Commentary – November 2025

Monthly Market Commentary

By Kensington Asset Management Team

Equity Markets: Leadership Beneath the Surface

A late-month rally was just enough to push most major equity indices into positive territory for November. The cap-weighted S&P 500 gained 0.13%, while the equal-weighted version rose a more robust 1.73%, highlighting improving breadth. The Russell 2000 advanced 0.85%. In contrast, the Nasdaq 100 declined 1.64%, making it the weakest performer among major U.S. indices. International markets delivered mixed results. The Euro Stoxx 50 gained 0.11%, MSCI EAFE rose 0.55%, and MSCI Emerging Markets fell 1.60%.

The late-month rebound followed a sharp Risk-Off episode driven by a collapse in speculative assets. Bitcoin, which peaked in early October near $126,200, experienced a severe 36% peak-to-trough correction. That drawdown forced leveraged investors to liquidate positions across crypto and broader risk assets, contributing to heightened volatility. Selling pressure was compounded by losses tied to the unwinding of the yen carry trade, where investors borrow at low Japanese interest rates to fund investments in higher-yielding global assets.

Markets stabilized only after economic data pointed to a slowing, but still resilient, US economy. That “weaker but not weak” narrative helped restore confidence that the Federal Reserve could ease policy without tipping the economy into recession.

As the calendar turns toward year-end, investors increasingly look ahead to emerging themes for the coming year. Historically, these shifts often begin to surface in December as asset managers reposition portfolios ahead of consensus views.

Fed Easing and the Case for Small-Caps

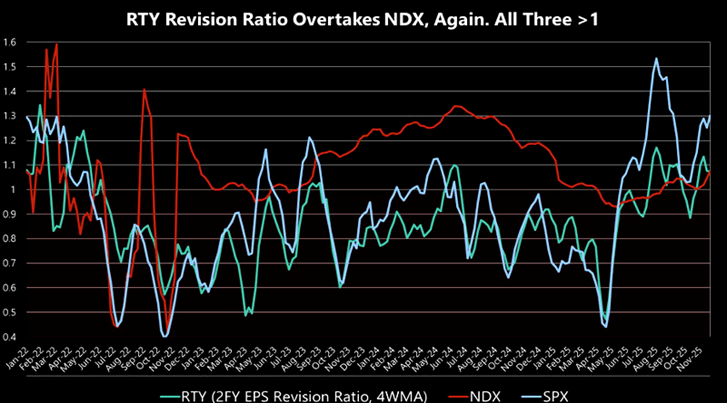

History suggests that the performance of equities during Fed easing cycles depends heavily on the surrounding economic environment. When rate cuts occur during economic expansions rather than recessions, leadership often rotates toward smaller-capitalization stocks.

With 2026 shaping up as a midterm election year and recession risk still muted, history points to a familiar pattern: sustained outperformance of Small-Caps. Notably, earnings revisions for the Small-Cap universe have turned positive, signaling a potential end to the earnings recession that plagued the segment over the past year.

Source: S&P Global as of November 30, 2025

[RTY – Russell 200o Index, NDX – NASDAQ 100 Index, SPX – S&P 500 Index]

Small-Cap earnings appear poised to accelerate through the fourth quarter and into next year, potentially outpacing Large-Cap Growth. Within the asset class, Small-Cap Value has historically outperformed Small-Cap Growth in the year following the onset of a sustained easing cycle, reinforcing the leadership shift now beginning to take shape.

Fixed Income: Liquidity Matters Again

Fixed income markets also delivered solid results in November. The 10-year Treasury returned 1.05%, the Bloomberg US Corporate Investment Grade Index gained 0.65%, Bloomberg US Mortgage-backed Securities Index rose 0.62%, and Bloomberg US Corporate High Yield Index advanced 0.58%. The 30-year Treasury gained 0.30%.

Returns were supported by three primary factors: growing confidence in a December Fed rate cut, a flight to safety during the mid-month deleveraging episode, and inflation data that remained above target but showed signs of moderation.

Looking ahead, fixed income markets face several important cross-currents. Global fiscal stimulus remains substantial. The US is running annual deficits exceeding $2 trillion, while Japan, Germany, and the US continue to implement new stimulus initiatives.

At the same time, US monetary policy has shifted from restrictive toward neutral. The Federal Reserve has slowed the pace of balance sheet runoff and adopted an “ample reserves” framework that will increase reserves by roughly $40 billion per month, injecting additional liquidity into the system.

Japan: A Structural Shift with Global Implications

These dynamics are unfolding against a backdrop of persistent inflation across developed markets, particularly in Japan. Core CPI in Japan rose 3.0% year over year in October, well above the Bank of Japan’s (“BOJ”) 2% target, increasing pressure on policymakers to respond.

For years, the BOJ’s policy of Yield Curve Control capped domestic yields and suppressed volatility. That framework was formally abandoned in March 2024, marking a historic shift toward quantitative tightening and reduced bond purchases.

As a result, Japanese bond yields are finally beginning to reflect underlying inflation pressures. The market is also adjusting to increased government issuance at a time when the BOJ, previously the dominant buyer, is stepping back. Given Japan’s role in global capital flows, these changes have meaningful implications for global fixed income markets, particularly as central banks worldwide retreat from quantitative easing and rely more heavily on private capital to absorb supply.

Source: StockCharts.com as of December 8, 2025

The Fed: Neutral Rates, More Liquidity

At its latest meeting, the Federal Open Market Committee lowered rates by 25 basis points, as expected. Chairman Powell described policy as having reached a neutral level and emphasized that the Fed is well positioned to pause and assess incoming data.

The Fed also announced reserve-management purchases of short-term Treasuries, totaling $40 billion in the first month, to ensure ample liquidity in money markets. While Powell stressed these actions were separate from monetary policy, their effect is nevertheless to increase system liquidity.

By signaling neutrality on rates while simultaneously adding liquidity, the Fed has attempted to balance competing risks: avoiding an overly dovish stance that could push long-term rates higher, while preventing a liquidity shortfall. For now, markets appear comfortable with that balance.

Looking ahead, the composition of the FOMC will shift in 2026, with several more dovish regional Fed presidents rotating into voting positions. This evolving policy backdrop helps explain the strong performance of precious metals in 2025 and renewed interest in inflation-sensitive assets such as commodities.

At the same time, the growing influence of alternative policy voices, including Kevin Warsh, introduces additional uncertainty. A more aggressive balance-sheet reduction approach would likely increase near-term volatility but could reset longer-term inflation expectations. While untested, such policy shifts underscore the importance of flexibility as markets navigate the next phase of the cycle.

Disclosures:

Investing involves risk, including possible loss of principal. Past performance does not guarantee future results. No strategy, including diversification, ensures a profit or prevents loss.

This is for informational purposes only and is not a recommendation nor solicitation to buy, sell or invest in any investment product or strategy. Our materials may contain information deemed to be correct and appropriate at a given time but may not reflect our current views or opinions due to changing market conditions. No information provided should be viewed as or used as a substitute for individualized investment advice. An investor should consider the investment objectives, risks, charges, and expenses of the investment and the strategy carefully before investing.

Please refer to Important Disclosures | Glossary

KAM20251218

Related Perspectives

View All-

2025 Investment Strategies Review

Risk assets delivered mixed but generally positive results in November as investors weighed softer labor data, the ongoing government shutdown, and the prospect of another Federal Reserve rate cut in December.

-

2025 Year-End Market Review

Risk assets delivered mixed but generally positive results in November as investors weighed softer labor data, the ongoing government shutdown, and the prospect of another Federal Reserve rate cut in December.